What the 50/30/20 Rule Really Is And Why It Still Matters

Most people don’t struggle with money because they’re bad at math. They struggle because real life is messy. Rent goes up. Kids need braces. Cars break down at the worst possible moment. Somewhere between bills, groceries, and trying to enjoy life, budgeting starts to feel less like a plan and more like a guilt trip.

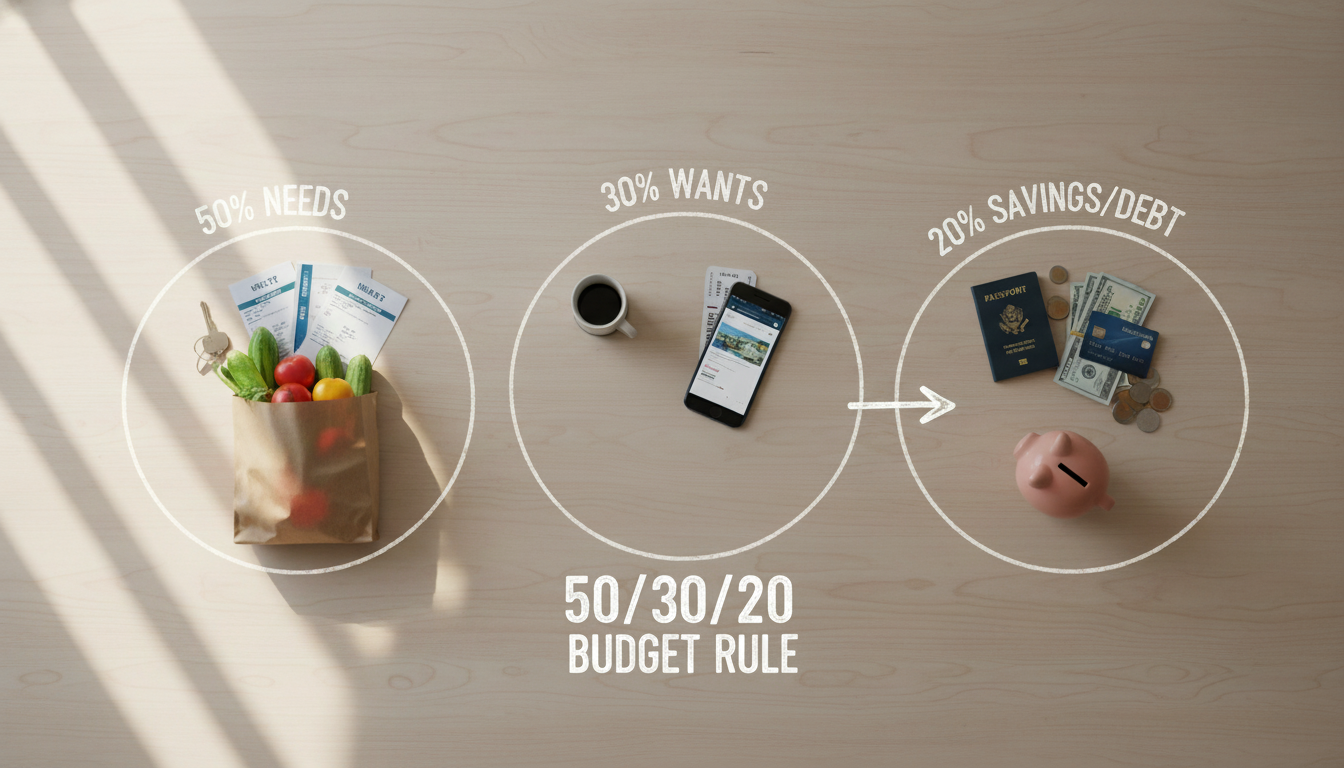

That’s where the 50/30/20 budget rule comes in. At its core, the rule is simple: 50% of your after-tax income goes to needs, 30% goes to wants, and 20% goes to savings. Without spreadsheets with 42 categories or tracking every coffee down to the cent, you only need three buckets to make clearer decisions.

But here’s the important note: the rule only works when you adapt it to your real life. Used rigidly, it can feel unrealistic. Used thoughtfully, it can be a powerful starting point that actually sticks.

The 50% Bucket: Needs

What Counts as a “Need”?

Needs are the essential expenses required to keep your life running smoothly. These typically include rent or mortgage payments, utilities and basic internet, everyday groceries, transportation costs, insurance premiums, and minimum debt payments. If you were to skip any of these, it would likely lead to serious consequences such as missed bills, housing issues, or difficulty getting to work.

When Needs Take Up More Than 50%

This is a question most people ask. In high-cost cities or during early career years, housing alone can eat up 40% or more of income. So, adding insurance, groceries, and transportation makes the “50% rule” feel impossible.

It’s time to adjust your budget. Instead of forcing your life into a strict percentage, treat 50% as a benchmark, not a rulebook. If your needs sit closer to 55% or 60%, the goal becomes balance.

The 30% Bucket: Wants

Wants Aren’t the Enemy

Wants are the expenses that make life more enjoyable but aren’t essential for day-to-day survival. These include things like dining out or ordering takeout, streaming subscriptions, vacations and weekend trips, hobbies, gym memberships, entertainment, and optional upgrades.

The Real Trap: “Lifestyle Creep”

The sneaky part? Wants don’t always feel like wants. That daily coffee. The multiple streaming services you barely use. The impulse buys that feel small but add up fast. The 30% category works best when you ask one simple question: “Is this actually making my life better, or just more expensive?”

The 20% Bucket: Savings (Your Future Self’s Safety Net)

Why 20% Is the Heart of the Rule

This category covers building your future and includes things like emergency fund contributions, retirement savings through a 401(k) or IRA, long-term investing, and extra debt payments beyond the minimum. Savings are what transform budgeting from short-term survival into long-term stability, so if you prioritize nothing else, start here, even small, consistent contributions matter far more than perfect timing.

Can’t Save 20% Right Now?

If 20% feels unrealistic, you can start smaller by saving 5% or 10%, increasing your savings when income rises, or even automating contributions.

Why the 50/30/20 Rule Doesn’t Work the Same for Everyone

Income Level Changes the Math

Someone earning $45,000 a year faces different constraints than someone earning $150,000. Fixed costs hit harder at lower incomes, while higher earners often have more flexibility and more opportunity to save aggressively.

Life Stage Matters More Than People Admit

Your budget should change as your life changes. Early in your career, you may be managing higher debt, lower income, and building basic financial habits. As families grow, expenses like childcare and housing increase. During peak earning years, the focus often shifts to maximizing investments and retirement savings, while later in life, budgeting centers on protecting savings and managing fixed or retirement income.

Modern Costs Have Changed the Game

Housing, healthcare, and education have become far more expensive than wages in many places, making flexible budgeting a necessity rather than a nice-to-have.

How to Adjust the 50/30/20 Rule to Your Lifestyle

Many households adjust the traditional framework to better fit their reality. A 60/20/20 split often works well in high-cost areas or for lower incomes where essentials take up more room. A 50/20/30 approach suits aggressive savers who prioritize long-term goals, while a 55/25/20 balance is common for families managing both expenses and savings. High earners focused on wealth building may even use a 40/30/30 structure to accelerate investing and savings.

How to Start Using the Rule

Step 1: Look back before you plan ahead. Pull the last one or two months of bank statements. Categorize spending into needs, wants, and savings.

Step 2: Base everything on after-tax income. Your budget works with what actually hits your account, which means net salary. This keeps the math honest and usable.

Step 3: Automate the important stuff. Set savings transfers to happen on payday. When savings come first, the rest of the budget adjusts naturally.

Step 4: Review monthly. Budgets don’t need micromanaging. A monthly check-in is enough to spot issues and make adjustments without burnout.

A Real-Life Example

Imagine a household bringing home $5,000 per month after taxes.

A flexible 50/30/20-style budget might look like:

- Needs: $2,700 (rent, utilities, groceries, insurance)

- Wants: $1,300 (dining out, subscriptions, travel fund)

- Savings: $1,000 (emergency fund, retirement)

When the 50/30/20 Rule May Not Be the Best Fit

You may need a different budgeting approach if you’re aggressively paying down high-interest debt, dealing with income that changes from month to month, spending most of your income on housing, or trying to catch up on retirement savings. In situations like these, hybrid or goal-based budgeting often works better, where you prioritize saving first and then spend what remains.

The Bottom Line: Use the Rule as a Tool, Not a Test

The 50/30/20 budget rule creates awareness, balance, and breathing room in your finances. If your numbers aren’t exact, that’s okay. The important things are you know where your money is going, you’re covering today’s needs, and you’re protecting tomorrow’s goals.