Being behind on debt can feel crushing when paying the minimum barely reduces your balance. High interest rates keep rising, and the constant phone calls are ones you wish you could ignore. When managing bills starts to seem impossible, turning to a Debt Management Program (DMP) can offer a clear and structured way to move forward. This approach doesn’t require taking out another loan or harming your credit like more extreme options could.

This guide explains all the key points you need to understand. It covers how these programs function, who gains the most from them, what they charge, how they affect your credit, and how to figure out if they’re the right choice for you.

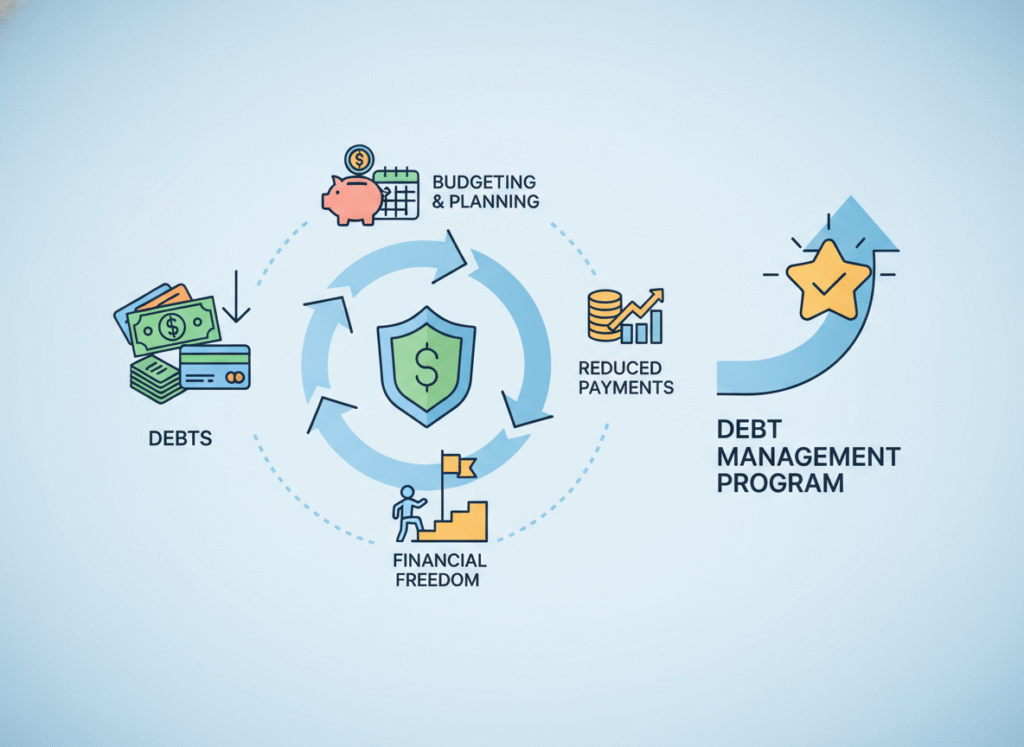

What Is a Debt Management Program?

A Debt Management Program offers a repayment plan created and handled by a nonprofit credit counseling agency. Unlike debt settlement that aims to cut down the amount you owe or consolidation loans that involve taking on new credit, a DMP helps you pay back your debt. The difference is that it makes payments much simpler to manage.

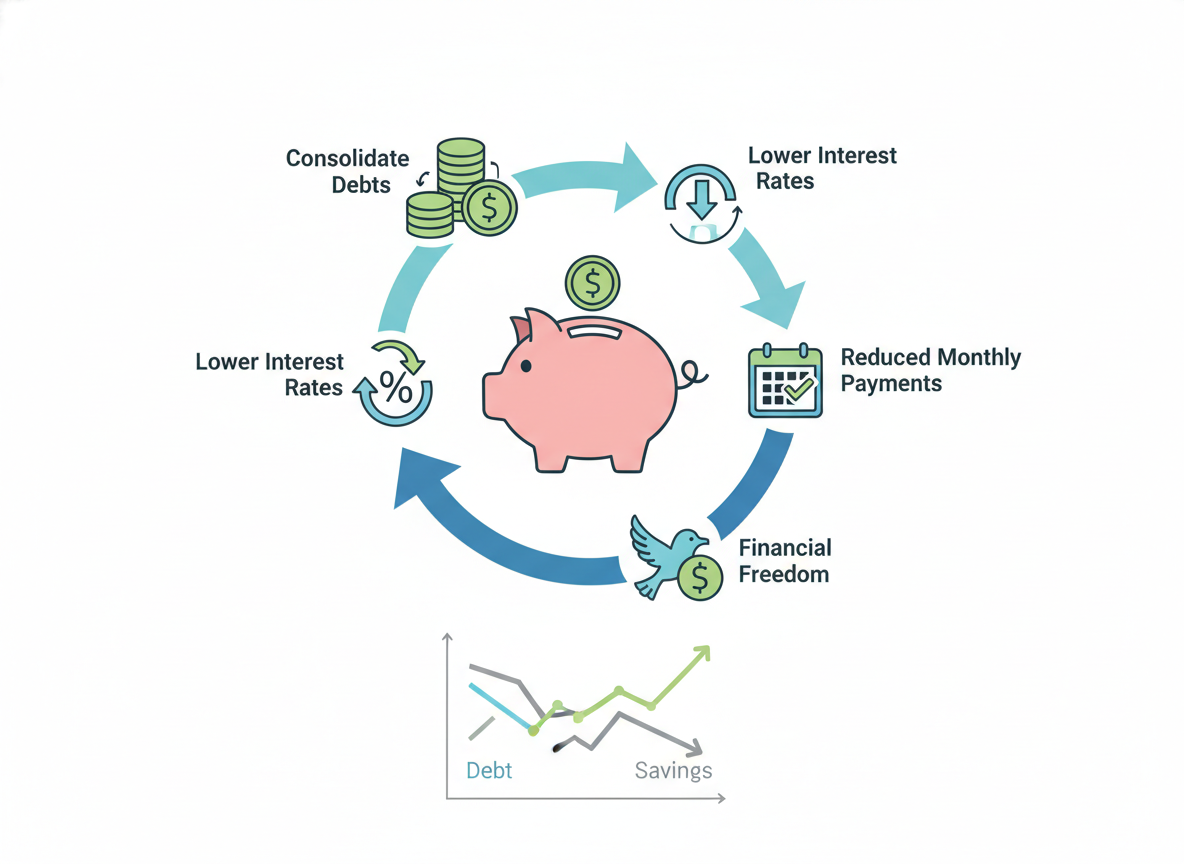

A debt management plan offers several key benefits, including lower interest rates on eligible debts like credit cards, reduced or waived fees, and a single monthly payment managed by the agency. It also provides a clear repayment timeline, along with a structured, manageable budget and relief from collection calls once creditors agree to the plan.

Debt Management Programs, known as DMPs, are made to help with credit card debt, medical bills, personal loans, and other unsecured debts. They don’t cover mortgages, car loans, or student loans.

Steps in Debt Management Programs

1. Meet With a Certified Credit Counselor

This can be done online or over the phone and is free. The counselor will examine your earnings, monthly costs, different kinds of debt, how much interest you’re paying, debt collection efforts, and your financial priorities.

2. The Counselor Designs a Custom Plan to Pay Off Your Debt

If a DMP is a good choice, the counselor will work out a monthly payment you can afford, identify which creditors may lower your interest rates, estimate how long it’ll take to pay everything off, and determine whether you need to close any of your current accounts.

3. Creditors Decide If They Accept Or Decline The Plan’s Terms

Most major credit card issuers participate in debt management programs, though they aren’t obligated to do so. In a DMP, your credit counselor negotiates on your behalf to reduce interest rates, often from 20–30% down to roughly 6–10%, bring overdue accounts current, and remove certain late fees or penalties.

4. You Send One Payment Each Month

Rather than paying many lenders, you pay the counseling agency. They handle dividing your payment among your creditors. This makes it easier to plan your budget and stick to it, which is super important for paying off your debt.

5. You Get Continuous Guidance And Help

Many agencies provide more than just debt help. They also offer budgeting support, financial education, guidance on managing your credit, and assistance if your income changes.

Debts You Can (and Can’t) Include in a DMP

| Debts that fit | Debts that don’t fit |

|---|---|

|

|

How DMPs Change Your Credit Score

Joining a debt management plan itself won’t lower your credit score, and a “credit counseling” note on your credit report is informational only and not used in scoring models. However, your score may dip temporarily if credit cards included in the plan are closed, since reduced available credit can increase utilization and closing older accounts may slightly shorten your credit history in the short term.

What Can Boost Your Score Over Time

Consistent on-time payments, lower balances, reduced credit utilization, and avoiding late or missed payments all help improve your credit over time. As balances come down and positive habits add up, many people see noticeable score improvements within one to two years.

Ups and Downs of Debt Management Programs

When a Debt Management Plan Works Best

A DMP can also make sense if you earn a steady income yet still feel financially tight. By lowering rates and consolidating payments, a DMP can make repayment more manageable.

For those who want to avoid bankruptcy or debt settlement, a DMP offers a more credit-friendly path. You still repay what you owe, but with structured support that protects your credit profile better than more extreme options.

Debt management can also provide relief if you’re feeling overwhelmed or unsure how to move forward. Having a clear plan, a defined timeline, and professional guidance often restores confidence and momentum. Most plans are designed to help people become debt-free within 36 to 60 months.

When a DMP Might Not Be Right for You

A debt management plan isn’t always the best solution in every situation. Other options may make more sense if your income is unstable, most of your debt is secured by assets, or you need immediate relief from legal actions like garnishments. You might also be better off managing repayment on your own if your total debt is relatively small or if you can effectively use strategies like the snowball or avalanche method. In some cases, alternatives such as debt consolidation, settlement, hardship programs, or even bankruptcy may provide a more appropriate path forward depending on your circumstances.

Comparing DMPs to Other Debt Options

Debt Consolidation Loan

It can work well if you have strong credit, since approval and interest rates depend heavily on your credit score. It allows you to combine multiple debts into one payment without closing your existing credit accounts, but it does require qualifying for a new loan.

Balance Transfer Credit Card

It’s often effective if you can secure a 0% introductory APR. This option typically requires good to excellent credit and works best as a short-term strategy.

Debt Settlement

It aims to reduce the total amount you owe, but it comes with significant downsides. It can seriously damage your credit, involve high fees, and carries the risk of creditor legal action. Rebuilding your credit afterward may take years.

Bankruptcy

It provides the most powerful form of debt relief by eliminating many types of debt, but it also leaves a long-lasting mark on your credit report, typically seven to ten years.

Real-World Example: How Much Can You Save?

Imagine you owe $20,000 in credit card debt, the interest rate averages 25%, and your monthly minimum payment is $500. If you pay the minimum each month, clearing the debt may take over 20 years and rack up a huge amount in interest.

When you switch to a debt management plan, interest rates are often reduced to around 7–10%, making payments more predictable and manageable. Most plans are completed within three to five years. For many people, this structure is why a DMP is seen as one of the simplest and most reliable ways to get a fresh start financially.

How to Tell If You Qualify

Each debt management program has its own guidelines, but many people qualify under common circumstances. If you carry unsecured debt, such as credit cards, medical bills, or personal loans, and can afford a consistent monthly payment, even one smaller than your current obligations, a DMP may be an option.

These programs are often designed for people experiencing financial pressure due to job changes, medical expenses, rising costs of living, or past-due bills. Another key requirement is being ready to stop using credit cards while enrolled, which helps ensure long-term progress and prevents new debt from undermining the plan.

The Bottom Line: A DMP Could Be Your Smartest Move for Debt Relief and Structure

If debt is keeping you up at night, payments feel endless, or you’re worried about making the wrong move, a Debt Management Program can offer something invaluable: clarity, stability, and a clear path forward.

With the right guidance, a DMP helps you address debt without the long-term damage associated with bankruptcy or the risks of debt settlement. It can be one of the most reliable and effective ways.