Life moves fast. Bills show up whether you’re ready or not. Groceries cost more than they used to. And somewhere between work, family, and trying to have a life, managing money often becomes something you react to, not something you control.

Here’s the thing: You don’t need a perfect budget, a finance degree, or extreme discipline to feel better about your money. You need a few smart habits that actually fit real life.

Below are 10 personal money management tips designed for busy U.S. adults, including renters, homeowners, couples, families, and professionals, who want clarity, stability, and progress without turning money into a second job.

The Real Challenges of Money Management Today

Money management sounds simple on paper: spend less than you earn, save consistently, and plan ahead. But in real life, it rarely feels that clean.

Many people struggle not because they’re irresponsible, but because the system is noisy. Income doesn’t always rise as fast as expenses. Housing, food, insurance, and childcare costs keep climbing. Add irregular paychecks, student loans, family responsibilities, or just plain burnout, and it’s easy to feel like you’re doing everything “right” and still falling behind.

There’s also the emotional side. People usually deal with stress, guilt, comparison, and fear when making decisions. Plus, social media doesn’t help. Neither does advice that assumes unlimited time, perfect discipline, or a six-figure income.

Understanding these challenges matters because it reframes the goal. Personal money management will build systems that work even when life gets messy.

1. Get Clear on Where Your Money Is Going (Without Judging Yourself)

Most money stress comes from not knowing, so before you change anything, you need visibility.

What To Do This Week

Set aside 20 minutes to review your last month of bank and credit card statements. Notice what surprised you, like forgotten subscriptions, food delivery, or impulse buys, and pay attention to what spending actually felt worth it versus what felt draining afterward.

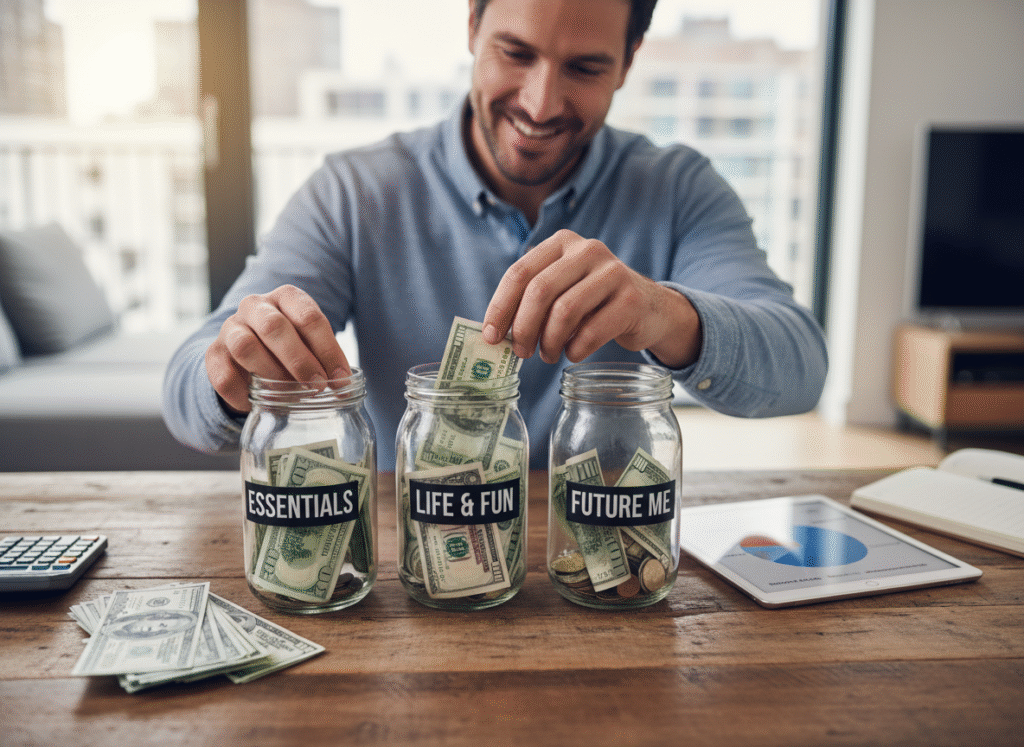

2. Build a Simple Spending Framework

A Flexible Approach That Works

Use a loose structure instead of micromanaging your money by grouping spending into a few clear buckets: essentials (housing, utilities, groceries, insurance), life & fun (eating out, hobbies, kids’ activities), and future you (savings, investing, debt payoff). This approach works better for real life because many traditional budgets fail by being too strict and unrealistic. If you want a simple starting framework, the 50/30/20 guideline can help you set rough boundaries without locking you into rigid rules.

3. Automate the Boring Stuff

When saving and investing depend on remembering or feeling motivated, they tend to stall. Automation removes friction and makes progress happen quietly in the background. This might look like setting transfers to savings on payday, enrolling in automatic retirement contributions, or scheduling recurring bill payments. Once these are in place, your finances require less daily energy, and consistency becomes much easier to maintain.

4. Create an Emergency Fund That Actually Makes You Feel Safer

Instead of stressing over six months of expenses right away, start smaller and build momentum. For example, aim for a $1,000 starter buffer first, then work toward covering one month of essential expenses. From there, you can gradually grow your emergency fund to three to six months over time, then keep this money in a high-yield savings account so it stays safe, easy to access, and earns interest while it sits there.

5. Tackle Debt Strategically

Debt isn’t a moral failure, but it’s a math problem mixed with behavior. The key is choosing a payoff approach you’ll actually stick with. Some people prefer the snowball method, which focuses on paying off the smallest balance first to build momentum and motivation. Others choose the avalanche method, which targets the highest interest rate first to save more money over time. Both approaches work. The best plan is simply the one you can follow consistently without burning out.

6. Use Credit Cards as Tools, Not Traps

Credit cards can either support your finances or slowly work against you, it all comes down to how you use them. Healthy credit habits include paying your statement balance in full whenever possible, keeping utilization below about 30%, and avoiding carrying balances for everyday spending so interest doesn’t erode your financial progress.

7. Save for Retirement Earlier Than Feels Necessary

Instead of stressing about maxing everything out, you need to focus on steady progress. Start by contributing enough to get your employer match (it’s essentially free money), then increase your contributions as your income grows. If investing feels intimidating, simple, diversified options like target-date funds can take the pressure off decision-making. Over time, compound growth will do far more of the heavy lifting than motivation ever could.

8. Separate Your Money by Purpose

When everything sits in one account, it’s easy to overspend, or panic when balances dip. Creating simple “money buckets” adds instant clarity. For example, use your checking account for bills and daily spending, keep savings separate for emergencies and short-term goals, and reserve investing accounts for long-term growth. This small mental shift makes your money feel calmer, more intentional, and easier to manage almost right away.

9. Adjust for Real Life (Irregular Income, Kids, Curveballs)

Personal money management isn’t one-size-fits-all, especially in 2024–2025. Life changes fast, so building some breathing room into your finances, checking in every few months, and expecting things to shift is extremely important. Being flexible with money is a skill worth developing.

You can start planning for modern financial realities by accounting for side income or commission-based pay, preparing for rising insurance and housing costs, and factoring in major obligations like childcare, elder care, or student loan payments so your budget reflects real life, not ideal assumptions.

10. Stick With “Good Enough” Longer Than You Think

Most people struggle with money because they give up too early. Remember, real consistency is essential. It looks like messy months, small wins, and the occasional reset. Over time, those efforts add up, and progress compounds, just like interest.

Money Management Tips for Young Adults

If you’re early in your career, money management comes with a unique mix of pressure and opportunity. You’re making real money for the first time, but you’re also navigating rent, student loans, career uncertainty, and rising living costs.

Here are a few principles that matter most at this stage:

- Start before you feel “ready”: Waiting until you earn more or feel confident often delays progress for years. Even small habits, such as saving $50 a month or contributing a little to retirement, compound faster than you expect.

- Avoid lifestyle creep early: As income rises, expenses tend to follow. Being intentional about upgrades helps you build flexibility instead of financial pressure.

- Build credit carefully, not aggressively: One or two well-managed accounts are usually enough because the goal is consistency, not complexity.

- Focus on habits over hacks: Young adults benefit more from stable routines, like tracking spending, saving automatically, paying bills on time, than from chasing advanced strategies too early.

- Mistakes will happen: They’re part of learning. Honestly, the real risk isn’t making a wrong decision, it’s avoiding decisions altogether.

The Bottom Line

Personal money management is about reducing stress, creating options, and giving yourself room to breathe. When your systems are simple and realistic, money stops demanding constant attention, progress becomes quieter, confidence grows, and instead of reacting to every expense or headline, you start making decisions from a place of clarity.

Related Articles

- Money Management for Students: Simple Budgeting Tips to Save More and Stress Less

- How to Develop a Strong Money Mindset That Improves Your Finances and Builds Long-Term Wealth

- 7 Best Personal Budgeting Apps to Track Spending, Save Money, and Stay Organized

- 10 Best Money-Saving Apps to Help You Save More Automatically in 2025