Ratio Explained: How It’s Calculated, Why It Matters, and Ideal Limits")

You can do almost everything “right” with your money, such as pay on time, save steadily, keep your credit score healthy, and still get tripped up by one quiet number: your debt-to-income (DTI) ratio. Until a lender suddenly shows up, you don’t think about it because it doesn’t appear on your credit report.

If you’re planning to apply for a mortgage, refinance, take out a personal loan, or even just want a clearer picture of your financial health, understanding DTI can save you time, stress, and disappointment. Let’s break it down in a way that actually makes sense and is easy-to-understand.

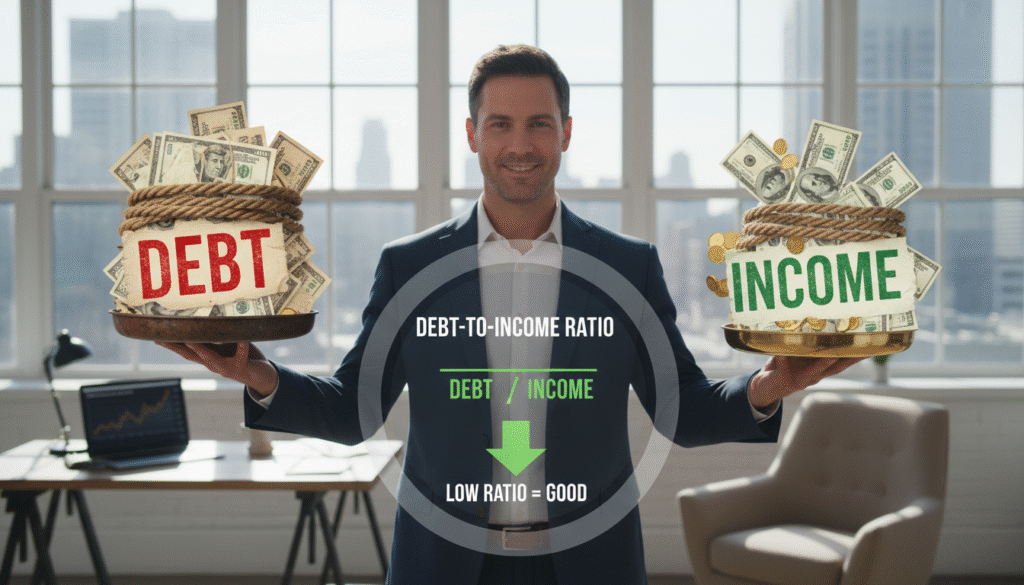

What Is a Debt-to-Income (DTI) Ratio?

Your debt-to-income ratio compares how much of your gross monthly income goes toward monthly debt payments. It’s expressed as a percentage.

In plain terms, DTI answers one question lenders care deeply about: “How stretched is your income already?” The higher the percentage, the more of your income is committed to debt, and also the riskier you look on paper. Lenders use DTI when reviewing mortgage applications, auto loans, personal loans, and some credit card approvals.

Why Lenders Care So Much About DTI

Credit scores show how you’ve handled debt in the past, while debt-to-income (DTI) ratio reflects whether you can realistically handle more debt right now. Even borrowers with excellent credit can be denied if their DTI is too high, because lenders focus on current cash flow, not just past behavior.

A lower DTI signals to lenders that you have breathing room in your budget, are less likely to miss payments, and can better absorb unexpected expenses, making you a lower-risk borrower overall.

What Counts (and Doesn’t) in Your DTI

| Debts that usually count | Expenses that don’t count |

|---|---|

|

|

How to Calculate Your DTI (Step by Step)

DTI Formula

Total monthly debt payments ÷ gross monthly income × 100

Example

If your gross monthly income is $5,000 and your monthly debts include a $400 car loan, $300 in student loans, $200 in credit card minimums, and a $1,100 future mortgage, your total monthly debt comes to $2,000. Dividing $2,000 by $5,000 gives you a DTI of 40%, meaning 40% of your pre-tax income is already committed to debt payments.

Front-End vs. Back-End DTI (Mortgage-Specific)

Front-End DTI

The front-end DTI looks only at housing-related costs, including your mortgage principal and interest, property taxes, homeowners insurance, and any HOA fees. Lenders typically prefer to see this ratio land around 28% to 31%, though some flexibility exists depending on the loan type and overall financial profile.

Back-End DTI

It includes all monthly debts, housing plus everything else. This is what most people mean when they say “DTI.”

What Is a “Good” DTI Ratio?

There’s no single magic DTI number, but lenders generally view it in ranges: below 36% is considered strong and comfortable, 36%–43% is acceptable for many loans, 43%–50% signals higher risk and brings more scrutiny, and above 50% makes approval difficult. That said, higher income, a sizable down payment, healthy savings, or stable employment can sometimes offset a higher DTI and improve your chances of approval.

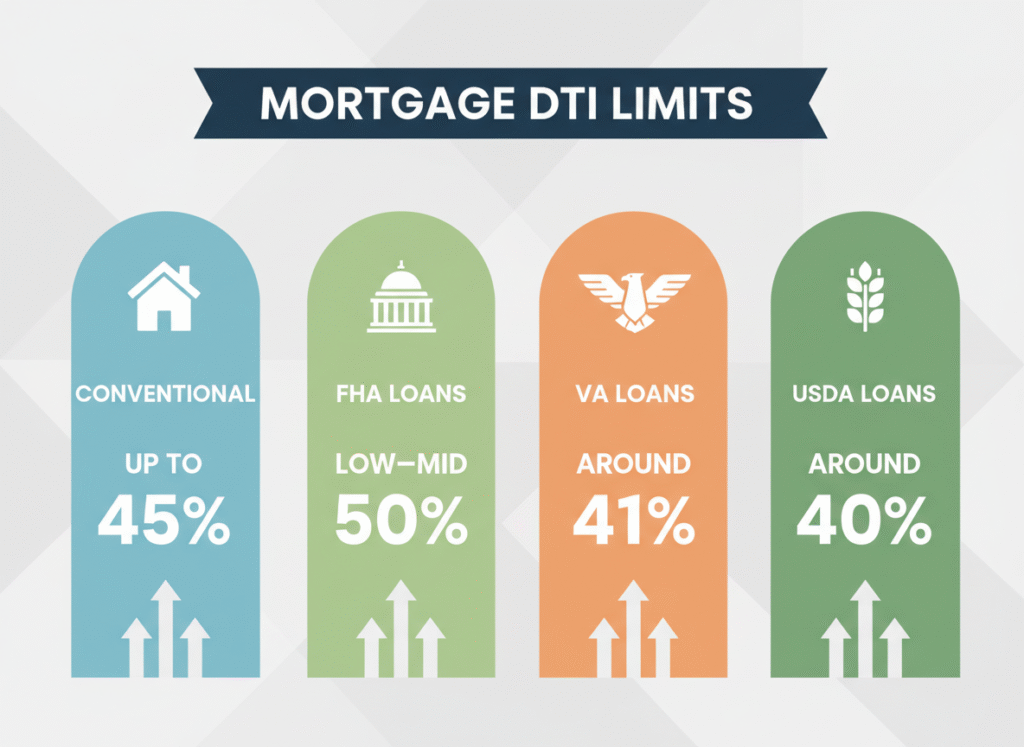

DTI Limits by Common Loan Types (General Guidelines)

DTI limits vary by loan type. Conventional mortgages often allow DTIs up to around 45%, and sometimes as high as 50% with strong compensating factors. FHA loans are more flexible and can permit higher DTIs, sometimes reaching the low-to-mid 50% range. VA loans don’t have a strict DTI cap, but around 41% is a common benchmark, while USDA loans tend to be tighter, often staying in the low 40% range.

Does DTI Affect Your Credit Score?

The short answer is no. Your DTI doesn’t appear on your credit report because credit bureaus don’t track income. That said, DTI and your credit score are still connected in indirect ways. Taking on more debt can raise your credit utilization, increase your monthly obligations, and push your DTI higher at the same time. For that reason, lenders almost always look at both your credit score and your DTI together when deciding whether to approve a loan, and on what terms.

Why a High DTI Can Hold You Back

When your DTI climbs too high, the effects tend to stack up. Loan approvals become harder to get, interest rates may rise, and lenders may cap how much you’re allowed to borrow. At the same time, your financial flexibility shrinks. Beyond lending decisions, a high DTI can spill into everyday life, too, making even small expenses feel heavier.

How to Lower Your DTI (Realistic Strategies)

First, you lower the debt side by paying down high-interest balances, eliminating small recurring debts first, and avoiding taking on new loans before applying.

Second, you increase the income side. You can earn side income from freelance work or a small second job. You also can raise or change jobs within the same field that improve pay stability. In some cases, adding a qualified co-borrower with reliable income can also strengthen an application and lower the overall DTI.

DTI and Modern Lending (2024–2025 Reality)

Today’s lenders look at debt-to-income ratios a little differently than they did even a few years ago. With higher interest rates pushing up monthly payments, lenders are more sensitive to how much of your income is already spoken for. Automated underwriting systems play a bigger role now, which means both numbers and context matter. Buy-now-pay-later plans are getting more scrutiny, even when they don’t feel like “real debt,” and lenders are paying closer attention to cash reserves, employment stability, and overall financial patterns alongside DTI.

Real-Life DTI Scenarios: How Lenders See Different Borrowers

DTI doesn’t exist in a vacuum. Two people can have the same ratio and get very different outcomes depending on income type, job stability, and overall financial picture.

Here’s how DTI plays out for real borrowers.

First-Time Homebuyer With Student Loans

Their profile is mid-20s to early 30s with a stable W-2 job, moderate income, and existing debts like student loans and a car payment. In these cases, a DTI range of about 38%–45% is typical and well within what many lenders are accustomed to reviewing.

Even with student loans, first-time buyers are often approved when payments are consistent and well documented, credit history is clean, and the projected mortgage payment is realistic for their income. Where many first-time buyers run into trouble is underestimating future housing costs can quietly push DTI higher than expected and affect affordability more than the loan payment alone.

High-Income Borrower With a High DTI

This profile typically falls in a 45%–50% DTI range and often includes borrowers with a six-figure income, multiple debts such as a mortgage, auto loans, and credit cards, and a strong credit score. Even at higher income levels, lenders still focus on percentages, so someone earning $180,000 with a 48% DTI may face tighter underwriting than a borrower earning $80,000 with a 32% DTI.

That said, high earners can sometimes offset a higher DTI with strong compensating factors, including large cash reserves, bigger down payments, low credit utilization, and stable, long-term employment, which help reduce perceived risk.

Self-Employed or Freelance Borrower

This profile typically includes a business owner, contractor, or freelancer with variable income and significant tax deductions. For self-employed borrowers, lenders usually calculate income using two years of tax returns, focusing on net income after deductions and averaging earnings over that period.

Because of this, DTI for self-employed borrowers can vary widely and often comes down to documentation rather than true affordability. Many improve their approval odds by reducing write-offs temporarily, maintaining larger cash reserves, and working with lenders experienced in non-W-2 income, who better understand how to evaluate variable earnings.

The Bottom Line

Your debt-to-income ratio reflects balance. A lower DTI gives you options, leverage, and peace of mind. In contrast, a higher one doesn’t mean failure, but it does mean planning matters more. If you’re preparing for a major financial move, knowing your DTI early and understanding how to improve it can put you back in control.