Planning for retirement is one of the most crucial steps you can take to secure your financial future. A Traditional IRA (Individual Retirement Account) is a powerful tool that helps you save for retirement while offering tax advantages. In this guide, we’ll break down the essentials of a Traditional IRA, including its benefits, contribution rules, tax advantages, and how it works, all while making it clear and easy to understand for beginners.

What is a Traditional IRA?

A Traditional IRA is a retirement savings account with special tax benefits. When you contribute to a Traditional IRA, your contributions may be tax-deductible (depending on your income and whether you have access to a workplace retirement plan), which reduces your taxable income for the year. Additionally, the money in your IRA grows tax-deferred, meaning you won’t owe taxes on the interest, dividends, or capital gains until you withdraw the funds in retirement.

Example: If you contribute $6,000 to your IRA this year and have a taxable income of $50,000, you’ll only be taxed on $44,000 (after subtracting the IRA contribution), which could lower your tax bill for the year.

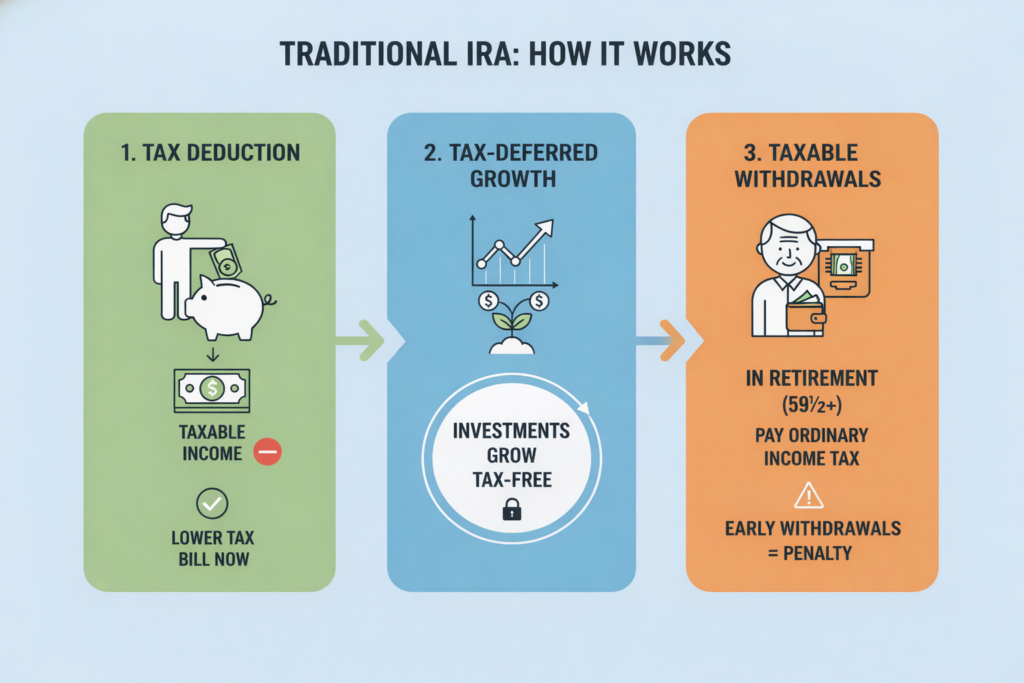

How Does a Traditional IRA Work?

Tax Deduction

When you contribute to a Traditional IRA, you may be able to deduct the contribution from your taxable income. However, the eligibility for this deduction depends on your income and whether you’re covered by an employer-sponsored retirement plan.

Tax-Deferred Growth

The real benefit of a Traditional IRA is the tax-deferred growth. This means that your investments will grow without being taxed until you withdraw the money. This can lead to faster wealth accumulation since you aren’t taxed every year on your earnings.

Taxable Withdrawals

When you retire and begin withdrawing funds from your IRA, those withdrawals will be taxed as ordinary income. The tax rate will depend on your total income during retirement.

Contribution Limits and Eligibility

The contribution limit for a Traditional IRA in 2026 is $6,500 for individuals under 50 years old, with a catch-up contribution of an additional $1,000 for those aged 50 and above, allowing them to contribute up to $7,500 annually.

Eligibility

If you have taxable income and aren’t covered by a workplace retirement plan, you can contribute the full amount and deduct it from your taxable income. However, if you participate in an employer-sponsored retirement plan, your ability to deduct your contributions may be reduced based on your income.

Example

If you work for a company that offers a 401(k) plan and have an income of $100,000, you may not be able to fully deduct your IRA contributions, depending on your income level.

When Can You Withdraw from a Traditional IRA?

Early Withdrawals

If you withdraw funds from your IRA before age 59½, you’ll face a 10% early withdrawal penalty, in addition to income tax. However, there are some exceptions, such as:

- First-time home purchase (up to $10,000)

- Qualified education expenses

- Medical expenses exceeding a certain percentage of your income

Required Minimum Distributions (RMDs)

Starting at age 73, you must begin taking Required Minimum Distributions (RMDs) from your IRA. If you fail to do so, you’ll face a penalty of 50% of the amount you were supposed to withdraw.

Tax Benefits and Withdrawals: What You Need to Know

Tax-Deductible Contributions

You can reduce your taxable income for the current year by contributing to your Traditional IRA. However, this only applies if you qualify based on your income and whether you participate in a workplace retirement plan.

Tax-Deferred Growth

Your money grows tax-free while it remains in the IRA. This allows your investments to grow faster compared to non-tax-advantaged accounts, where you might face yearly taxes on earnings.

Taxable Withdrawals

When you begin to withdraw money from your IRA in retirement, those withdrawals are taxed as ordinary income. If you withdraw before 59½, you’ll also face an additional 10% penalty unless you qualify for one of the exceptions.

How to Open a Traditional IRA

Opening an IRA is straightforward. You can open one at most banks, brokerages, or financial institutions. The key is choosing the provider that offers the investment options and fees that align with your financial goals. It’s important to understand the rules around contributions and withdrawals to ensure you’re taking full advantage of the tax benefits.

How to Decide if a Traditional IRA is Right for You

A Traditional IRA is a great option if you want to reduce your tax bill now and build wealth for retirement. However, if you anticipate being in a higher tax bracket when you retire or want more flexibility in how and when you withdraw funds tax-free, you might want to consider a Roth IRA instead.

Example: If you’re a high-income earner and believe your tax rate will be lower when you retire, a Traditional IRA may offer you the best tax benefits now. But if you expect to be in a higher tax bracket in the future, a Roth IRA might make more sense, as it offers tax-free withdrawals.

If you’re unsure whether a Traditional IRA is right for you, consider consulting a financial advisor to assess your retirement goals and income situation.

Final Thoughts: Taking Action for Your Future

Now that you have a better understanding of what a Traditional IRA is and how it can help you save for retirement, it’s time to take action. Start planning your contributions today and make sure you’re maximizing the tax benefits while staying within the contribution limits.

Investing in a Traditional IRA can be a smart move for securing your future financial freedom. By contributing now and deferring taxes until retirement, you’re setting yourself up for a more comfortable retirement. So, start today and take control of your retirement savings, there’s no better time than now to begin building your nest egg.

Related Articles

401(k) vs IRA vs Roth IRA: Key Differences Explained for Every Income Level