You can’t avoid taxes, but you can avoid paying more than necessary.

If you’ve ever looked at your tax bill and wondered “Why is this so high?” or “Did I miss something?”, you aren’t the only one dealing with this problem. Millions of Americans leave money on the table every year simply because they don’t fully understand tax credits or how to use them strategically.

This guide breaks tax credits down in an easy-to-understand way, and shows you how to use them to lower your tax bill quickly and legally, whether you file on your own or work with a professional.

What Is a Tax Credit (and Why It Matters So Much)?

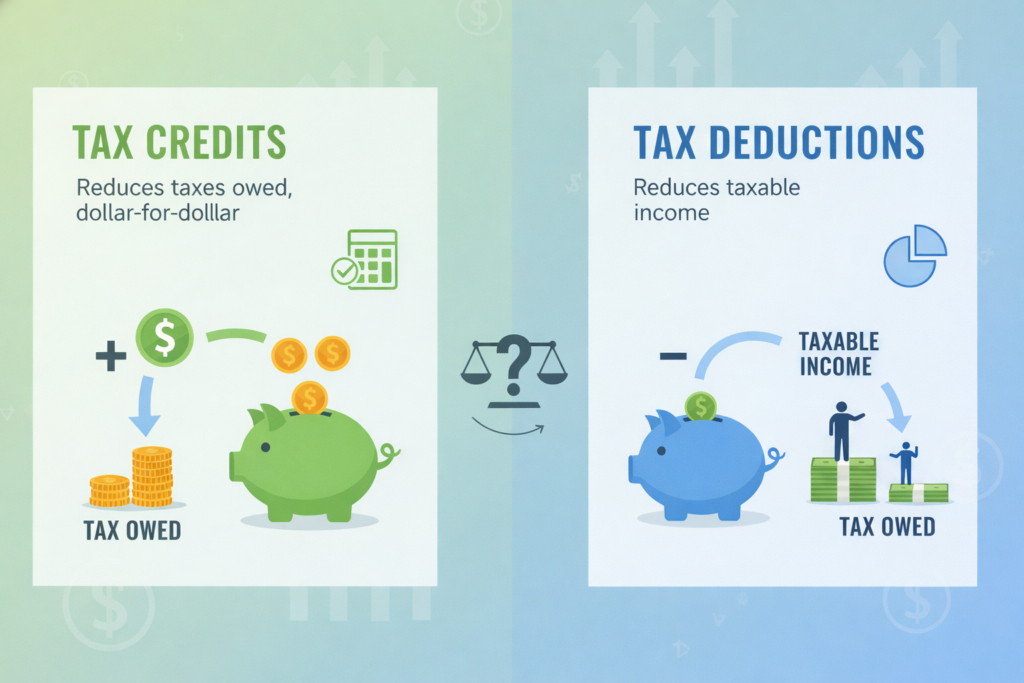

A tax credit is a dollar-for-dollar reduction of the taxes you owe, making it one of the most powerful tools for lowering your tax bill. For example, if you owe $4,000 in taxes and qualify for a $1,000 tax credit, your bill simply drops to $3,000 without complicated calculations required. This is a big difference from a tax deduction, which only reduces the income that’s taxed, not the amount you owe. Tax credits almost always provide bigger, faster savings because they directly cut your tax bill.

Why tax credits exist: The government uses tax credits to encourage behaviors it wants to support, like raising children, saving for retirement, going to school, buying health insurance, or improving energy efficiency.

Tax Credits vs. Tax Deductions: The Key Difference

Tax credits | Tax deductions | Quick example |

|---|---|---|

|

|

|

The smart tax planning usually focuses on maximizing credits first, then stacking deductions where possible.

How Tax Credits Work (Step by Step)

1. You qualify

Each tax credit comes with its own set of rules. Eligibility may depend on your income level, family situation, job status, or specific expenses you paid during the year. Meeting all the requirements matters, because even small details can affect whether the credit applies.

2. You claim the credit when you file

Tax credits aren’t applied automatically. You must enter the correct information on your tax return, and some credits require additional forms or schedules. If the paperwork isn’t completed properly, the credit won’t be counted.

3. The credit reduces your tax bill

Once claimed, the credit lowers the amount of tax you owe. Depending on whether the credit is refundable, nonrefundable, or partially refundable, it may also increase your refund.

Here’s the thing: the most common and expensive mistake taxpayers make is assuming the IRS will notice and apply credits for them. It won’t. If you don’t claim a credit accurately and on time, you simply lose the benefit.

The 3 Types of Tax Credits (This Part Is Critical)

1. Nonrefundable Tax Credits

Nonrefundable tax credits can lower your tax bill, but only down to zero, and they don’t generate a refund. For example, if you owe $600 in taxes and qualify for a $1,000 nonrefundable credit, your tax bill is wiped out, but the remaining $400 can’t be refunded or carried forward. Common examples of nonrefundable tax credits include the Lifetime Learning Credit, the Saver’s Credit, the Foreign Tax Credit, and certain residential energy credits.

2. Refundable Tax Credits

Refundable tax credits go a step further than simply lowering what you owe. They can reduce your tax bill and still generate a refund, even if your tax balance drops to zero. For example, if you owe $300 in taxes and qualify for a $1,200 refundable credit, your tax bill is eliminated and you receive the remaining $900 as a refund. Some of the most well-known refundable tax credits include the Earned Income Tax Credit (EITC) and the Premium Tax Credit for health insurance, especially valuable for working families and lower-income households.

3. Partially Refundable Tax Credits

Partially refundable tax credits reduce your tax bill, and if the credit amount is larger than what you owe, a portion of the remaining amount may be refunded. A common example is the American Opportunity Tax Credit (AOTC), which offers up to $2,500 per eligible student, with up to $1,000 of that amount refundable. This hybrid structure is especially common among education-related tax credits.

Most Common Tax Credits Americans Miss

Many taxpayers miss out on meaningful savings simply because they don’t realize how many tax credits are available to them.

Some of the most commonly used, yet still frequently overlooked, credits fall into a few key categories. Family and income-related credits include the Child Tax Credit, the Earned Income Tax Credit (EITC), and the Child and Dependent Care Credit. Education-related relief may come from the American Opportunity Tax Credit or the Lifetime Learning Credit.

Health and insurance expenses can qualify for help through the Premium Tax Credit for marketplace health coverage. Retirement savers may benefit from the Saver’s Credit when contributing to retirement accounts.

Homeowners can reduce costs with residential energy tax credits, clean energy and solar incentives, and electric vehicle tax credits. In more specific situations, credits such as the Adoption Tax Credit and the Foreign Tax Credit may also apply.

Why Credits Change Every Year (and Why That Matters)

Tax credits aren’t fixed from year to year. They shift in response to inflation adjustments, expiring legislation, and new tax laws passed by Congress. Recent and upcoming changes have already affected Child Tax Credit amounts, Earned Income Tax Credit income limits, energy and electric vehicle incentives, and retirement savings credits. That’s why relying on last year’s rules can be costly. A credit that didn’t apply before may now be available to you, or one you claimed in the past may have changed or disappeared.

Credits vs. Deductions: When to Use Both

The smartest taxpayers use both credits and deductions. For example, contributing to a traditional IRA can lower your adjusted gross income (AGI). A lower AGI may then qualify you for the Saver’s Credit, which directly reduces your tax bill. The result is a powerful stacking effect: you receive a deduction that lowers taxable income and a credit that cuts your taxes dollar for dollar. This is one of the most effective and most underused tax strategies available to everyday taxpayers.

Common Tax Credit Mistakes to Avoid

These mistakes show up every filing season, and they often cost taxpayers hundreds or even thousands of dollars:

- Assuming you don’t qualify because of income: Many credits have phaseouts, not hard cutoffs. Even moderate- and higher-income households may still qualify for partial benefits.

- Confusing deductions with credits: Mixing the two can lead to missed savings. Credits reduce your tax bill dollar for dollar, while deductions only lower taxable income.

- Overlooking state-level credits: State tax credits often mirror federal ones, and missing them can mean leaving money on the table.

- Failing to plan before December 31: Once the year ends, many opportunities disappear. Timing matters for credits tied to income, contributions, or purchases.

- Not adjusting withholding after life changes: Marriage, children, job changes, or side income can all affect credit eligibility and withholding needs.

How to Reduce Your Tax Bill Faster (Practical Checklist)

Before you file, ask yourself:

- Did I contribute to retirement accounts that qualify for credits?

- Did I pay for education, childcare, or dependent care?

- Did my income change this year?

- Did I move, adopt, or buy a home?

- Did I make energy-efficient home upgrades?

If the answer is “yes” to any of these, you may qualify for multiple tax credits.

Final Takeaway: Tax Credits Are a Planning Tool, Not a Filing Trick

Tax credits are one of the most effective ways to reduce your tax bill, but only if you understand how they work and plan ahead. They lower your taxes directly, can increase your refund, and reward smart financial decisions. Whether you rely on tax software, work with a professional, or use a mix of both, knowing which credits apply to your situation is one of the fastest ways to stop overpaying the IRS. The goal is to keep more of your money.

Related Articles

How to File Your Taxes in the U.S.: Step-by-Step Beginner’s Guide for Easy Filing