Buying a home is thrilling, but it can also feel overwhelming. For many buyers, the toughest decision isn’t picking the perfect house. It’s figuring out which mortgage makes the most sense.

It’s normal if you’re comparing FHA vs. conventional mortgages. These two loan options account for most home purchases in the U.S., and each one is built for different financial needs and situations.

Here’s the thing: there’s no single “best” mortgage for everyone. Plus, the right choice depends on your credit profile, your down payment, and how long you expect to own the home.

This guide explains everything in clear, straightforward terms, with practical, real-life insight, so you can choose a mortgage that works for you.

FHA vs. Conventional Loans: The Big Picture

Before diving into numbers, it helps to understand the core difference:

- FHA loans are backed by the federal government, which allows lenders to accept more risk.

- Conventional loans are not government-backed, so lenders rely more heavily on your credit and financial strength.

That single difference affects approval requirements, monthly payments, and long-term costs.

What Is an FHA Loan?

An FHA loan is backed by the Federal Housing Administration, which means the government helps protect lenders if a borrower can’t repay the loan. Because that risk is reduced for lenders, FHA loans typically come with more flexible approval standards, making them easier to qualify for than many other mortgage options.

Homebuyers often choose FHA loans because they allow lower credit scores, smaller down payments, and more lenient debt-to-income limits. Gift funds and down payment assistance programs are also permitted, which can be a big help if you haven’t saved much yet. These features make FHA loans especially appealing to first-time buyers, those working to rebuild their credit, or buyers with limited savings.

What Is a Conventional Mortgage?

A conventional loan isn’t backed by a government agency, which means the lender assumes the full risk of the loan. Because of that, qualification standards are typically tighter. However, borrowers with strong financial profiles are often rewarded with lower overall costs and more favorable terms over the life of the loan.

Many buyers choose conventional loans for their flexibility and long-term savings potential. These loans can be used for primary residences, vacation homes, or investment properties, and private mortgage insurance can be removed once enough equity is built. Conventional loans also tend to offer higher loan limits in many areas. They’re usually a good fit for buyers with solid credit, steady income, and the ability to make a larger down payment.

Key Differences Between FHA and Conventional Mortgages (Quick Comparison)

FHA | Conventional Mortgages | Suggestion | |

|---|---|---|---|

Down payment requirements |

|

| FHA is still more forgiving if your credit is lower, even though conventional loans now allow small down payments |

Credit score requirements | Minimum 500 (approval is more common at 580+) | Typically 620+, with better pricing above 700 | Higher credit scores help with both loan types, especially interest rates |

Debt-to-income ratio (DTI) | Often allow DTIs up to around 50% | Prefer under 36%, sometimes allow up to around 45–50% | If your student loans or car payment push your DTI higher, FHA may be more forgiving |

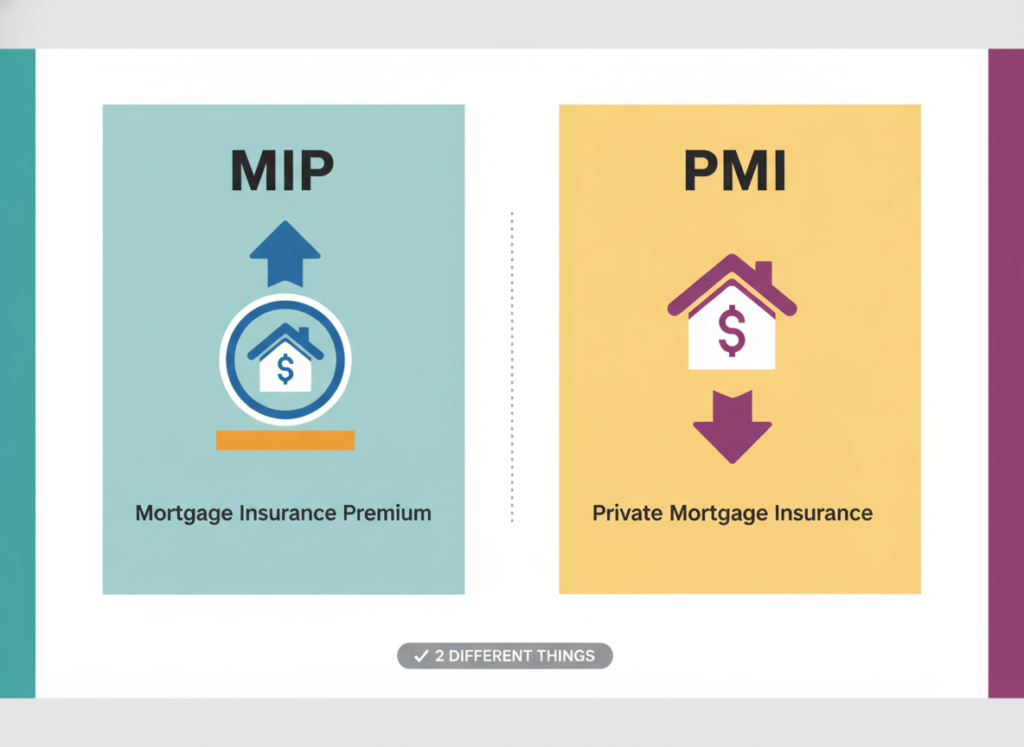

Mortgage Insurance: The Real Cost Difference

This is often the part of the mortgage decision that catches buyers off guard. FHA mortgage insurance, known as Mortgage Insurance Premium (MIP), is required on every FHA loan. It includes an upfront fee that’s usually rolled into the loan balance, plus a monthly insurance payment added to your mortgage. If you put down 10% or more, MIP typically lasts for 11 years. With a smaller down payment, you’ll pay it for the entire life of the loan unless you refinance.

With a conventional loan, mortgage insurance, called Private Mortgage Insurance (PMI), is only required if your down payment is under 20%. Unlike FHA insurance, PMI can usually be removed once you reach about 20% equity in your home, and its cost depends largely on your credit score. This is why FHA loans may appear more affordable at first, but conventional loans often become cheaper over time. As a result, many homeowners start with an FHA loan and later refinance into a conventional mortgage once their credit and equity improve.

Interest Rates: Which Is Lower?

You’ll often hear that FHA loans come with lower interest rates, and in some cases, that’s true. But focusing on the rate alone can be misleading. The interest rate is only one piece of the puzzle, and it doesn’t always reflect the true cost of the loan over time.

What really determines how much you’ll pay is the combination of the interest rate, the cost of mortgage insurance, and how long you plan to keep the loan. A conventional mortgage with a slightly higher rate may actually cost less overall if the mortgage insurance can be removed after you build equity. In contrast, an FHA loan with a lower rate can become more expensive in the long run if you’re required to pay mortgage insurance for many years, or even for the life of the loan.

Loan Limits (2024–2025 Snapshot)

Loan limits are updated each year and vary depending on where the property is located.

FHA Loans

The baseline borrowing limits are generally lower, though higher limits are available in more expensive housing markets to reflect higher home prices. Even so, FHA limits can restrict how much you’re able to borrow, especially in competitive or high-cost areas.

Conventional Loans

They typically offer higher baseline limits, giving buyers more room to work with when purchasing higher-priced homes. For borrowers who exceed those limits and have strong credit and financial profiles, jumbo loans are also an option. If you’re shopping in a high-cost market or planning to buy a larger or more expensive home, a conventional loan often provides greater flexibility.

Property Rules and Appraisals

FHA Property Requirements

Homes purchased with an FHA loan must meet stricter appraisal standards. The appraisal not only confirms the home’s value but also evaluates basic safety, livability, and overall condition. The property has to meet the FHA’s minimum guidelines before the loan can be approved, and it must be used as your primary residence, meaning you’re required to live in the home.

Conventional Property Rules

Conventional loan appraisals focus primarily on the home’s market value, with far fewer condition-based requirements. Because of this flexibility, conventional loans can be used for a wider range of properties, including primary residences, vacation homes, and investment properties. As a result, fixer-uppers or homes needing repairs are often easier to purchase with a conventional loan, since they may have trouble passing FHA appraisal standards.

Refinancing Options

FHA loans offer a Streamline Refinance option that’s designed to be quicker and less expensive than most refinancing programs. In many cases, it requires minimal paperwork and may not require a new appraisal, making it easier to lower your rate or monthly payment. Conventional loans also offer refinancing options, including rate-and-term refinances and cash-out refinances, but these usually involve more documentation and a full underwriting process.

Because of this, a common strategy is to begin with an FHA loan and refinance into a conventional mortgage once your credit score improves and you’ve built enough equity to eliminate mortgage insurance.

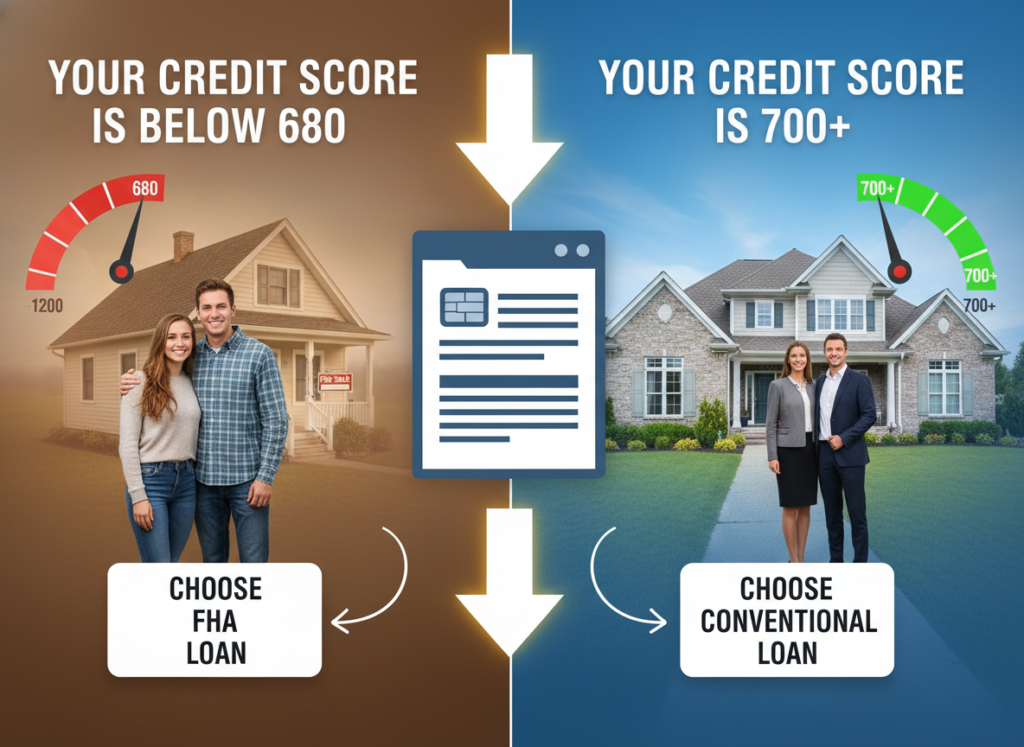

FHA vs. Conventional: Which One Fits You Best?

FHA may be better if:

- Your credit score is below around 680

- You have limited savings for a down payment

- Your DTI is on the higher side

- You’re buying a primary residence

- You plan to refinance later

Conventional may be better if:

- Your credit score is 700+

- You can put down 10–20%

- You want to avoid long-term mortgage insurance

- You’re buying a second home or investment property

- You plan to stay long-term

Common Buyer Mindset Mistakes to Avoid

1. Choosing a loan based on the interest rate alone

A low rate can look appealing, but it doesn’t show the full cost of the loan. Mortgage insurance, loan duration, and how long you keep the loan all play a major role in what you’ll actually pay over time.

2. Assuming FHA loans are “only for beginners”

FHA loans aren’t limited to first-time buyers. They’re a strategic option for buyers with specific financial profiles, including those rebuilding credit or prioritizing cash flow early on.

3. Ignoring long-term mortgage insurance costs

Ongoing insurance payments can add up significantly over the years. Failing to factor in how long you’ll pay PMI or MIP can lead to higher total costs than expected.

4. Not planning for refinancing from the start

Many buyers benefit from refinancing later, but skipping this strategy upfront can limit your options. Knowing when refinancing might make sense helps you choose the right loan now. That’s why the most financially savvy buyers think beyond the closing table. They plan five to ten years ahead, choosing a mortgage that supports both their current needs and future goals.

Final Thoughts: Make the Loan Work for You

Choosing between an FHA and a conventional mortgage is about finding the option that truly fits your financial situation. The right loan should work for where you are today, give you room to grow as your finances improve, and help keep long-term costs manageable. If you’re unsure which path makes the most sense, you should get pre-approved for both options and compare the numbers side by side. It can provide you with real clarity.