Understanding how your income tax is calculated can be intimidating, especially when faced with tax forms and unfamiliar terms. However, breaking down the process into simple steps can make it easier for you to estimate what you owe and maximize your tax refund. Whether you’re filing for the first time or want to make sure you’re getting the best tax return possible, understanding income tax calculations is essential for your financial well-being.

In this article, we’ll walk you through how income tax is calculated, including real examples to help you understand the process. By the end of this guide, you’ll be ready to estimate your tax liability with confidence and take control of your financial planning.

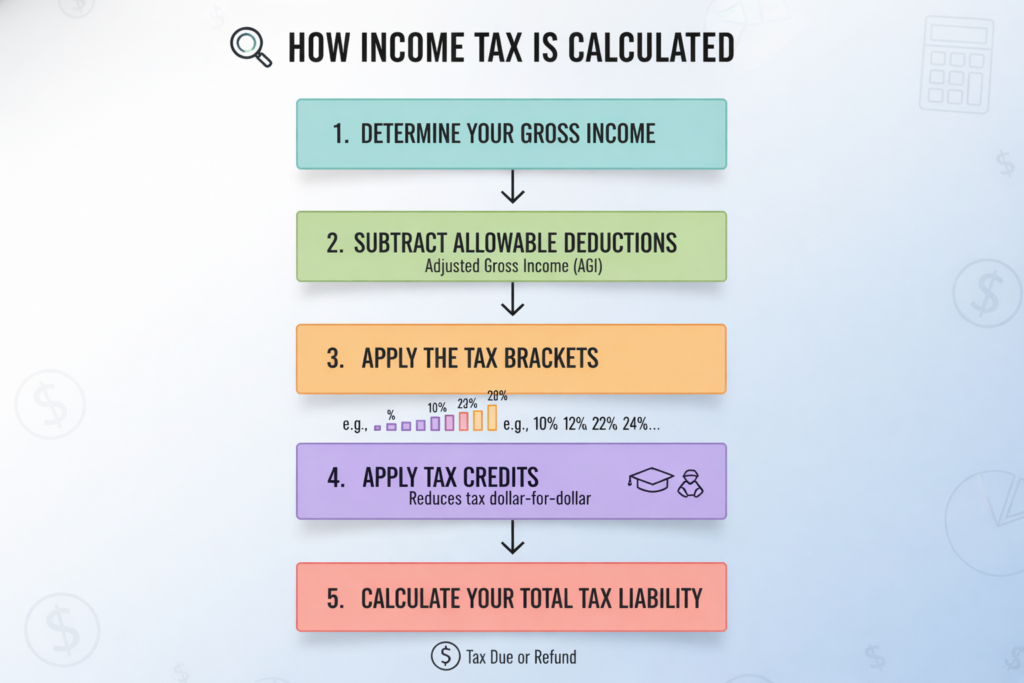

What Is Income Tax and How Is It Calculated?

Income tax is a tax levied by the federal government (and often state and local governments) on the money you earn. The U.S. operates under a progressive tax system, meaning the more you earn, the higher your income is taxed. However, your income isn’t taxed as a whole at a single rate. Instead, it’s taxed based on marginal tax brackets, income ranges taxed at different rates.

To calculate how much you owe, you follow these steps:

Step 1: Determine Your Gross Income

This is the total amount of money you earn before taxes. It includes wages, salaries, tips, dividends, and other forms of income, including investments.

Step 2: Subtract Allowable Deductions

Your taxable income is your gross income minus any deductions you’re eligible for. These deductions reduce your total taxable income and, in turn, the amount of tax you owe.

Step 3: Apply the Tax Brackets

Once your taxable income is calculated, apply the tax brackets based on your filing status such as single or married. Different portions of your income are taxed at different rates.

Step 4: Apply Tax Credits

After you calculate your tax based on the brackets, you can further reduce your liability using tax credits, such as the Child Tax Credit or Earned Income Tax Credit (EITC).

Step 5: Calculate Your Total Tax Liability

After applying deductions and credits, the result is the total amount of tax you owe.

Step-by-Step Breakdown of Income Tax Calculation

Let’s break this down with a real example: Imagine you’re a single filer with a gross income of $60,000. Your goal is to calculate how much federal income tax you’ll owe.

Step 1: Determine Gross Income

Your gross income is $60,000.

Step 2: Apply the Standard Deduction

For 2024, the standard deduction for a single filer is $13,850.

Your taxable income would therefore be:

60,000 – 13,850 = 46,150

So, your taxable income is $46,150.

Step 3: Apply Tax Brackets

The 2024 tax brackets for a single filer are as follows:

10% on income up to $11,000

12% on income between $11,001 and $44,725

22% on income between $44,726 and $95,375

Here’s how the calculation would look for $46,150 in taxable income:

10% on the first $11,000 = $1,100

12% on the next $33,725 (from $11,001 to $44,725) = $4,047

22% on the remaining $1,425 (from $44,726 to $46,150) = $313.50

Total tax before credits: 1,100 + 4,047 + 313.50 = 5,460.50

Step 4: Apply Tax Credits

Suppose you qualify for the Child Tax Credit (up to $2,000 per qualifying child under 17). If you have one child, you can apply this credit to reduce your tax liability.

Subtract the credit: 5,460.50 – 2,000 = 3,460.50

Your final tax liability is $3,460.50.

Tax Deductions: Standard vs. Itemized

You have two options when it comes to deductions: standard deduction or itemized deductions.

Standard Deduction

This is a fixed amount that reduces your taxable income. For a single filer in 2024, it’s $13,850.

Itemized Deductions

If your eligible expenses (e.g., mortgage interest, medical costs, state/local taxes, and charitable contributions) exceed the standard deduction, you can itemize your deductions instead.

Example

Let’s say you have $15,000 in itemized deductions. In this case, it would be more beneficial to itemize, since it’s greater than the standard deduction. This would further lower your taxable income, resulting in a smaller tax bill.

Tax Credits vs. Tax Deductions

It’s important to understand the difference between tax credits and tax deductions:

- Tax deductions reduce your taxable income, which lowers the overall amount of income that is subject to tax.

- Tax credits, on the other hand, directly reduce the amount of tax you owe. A tax credit is much more valuable than a deduction because it’s a dollar-for-dollar reduction of your tax bill.

For example, the Child Tax Credit directly subtracts $2,000 from what you owe, whereas a deduction might only reduce your taxable income by a certain amount.

State and Local Taxes: How They Affect Your Income Tax

In addition to federal taxes, many states and localities impose their own income taxes. While federal income tax rates are standard across the country, state income tax rates can vary widely, and some states, like Texas or Florida, have no state income tax at all.

When calculating your income tax, you should consider:

- State income taxes: These are typically withheld by your employer (if applicable) and vary by state.

- Local taxes: Some cities also have their own income tax rates, which can further affect your overall tax liability.

Remember, both state and local taxes can sometimes be deducted from your federal taxable income if you itemize deductions. This is known as state and local tax (SALT) deductions, but it’s subject to a $10,000 cap under recent tax laws.

Common Challenges in Income Tax Calculation

Many people face challenges when calculating their taxes, especially when it comes to understanding tax brackets, deductions, and credits. Here are a few common issues:

Misunderstanding Tax Brackets

It’s common to think that your entire income is taxed at the highest rate, but only the portion of your income that falls into each bracket is taxed at that rate.

Overlooking Deductions and Credits

Many taxpayers miss out on tax-saving opportunities because they don’t track eligible deductions and credits, such as medical expenses, education costs, and the Earned Income Tax Credit.

Complexity of Filing Status

The tax bracket and deductions available to you vary depending on your filing status (single, married, and head of household). Choosing the correct status is crucial for ensuring you’re taxed correctly.

Final Thoughts: Maximize Your Tax Efficiency

Tax season can be overwhelming, but by understanding how your income is taxed and applying the correct deductions and credits, you can reduce your tax liability and maximize your refund. Whether you’re a W-2 employee or a 1099 contractor, these steps will help you make sense of your taxes and guide you through the filing process.

Remember to track your deductions throughout the year, consider using tax software or consulting a tax professional, and stay updated on any tax changes to ensure you’re always prepared. By doing so, you’ll not only reduce stress during tax season but also set yourself up for long-term financial success.