When it comes to saving money or investing, understanding APY (Annual Percentage Yield) is essential. It helps you understand the real rate of return on your savings or investments by factoring in not just the interest rate but also the effects of compound interest. Whether you’re looking to invest in high-yield savings accounts, certificates of deposit (CDs), or other interest-bearing accounts, understanding APY can significantly impact how you approach your savings strategy.

This article will break down everything you need to know about APY, including its definition, how it works, why it’s important, and how you can use it to maximize your savings. Additionally, we’ll provide real-life examples to help you apply these concepts and get the best possible return on your money.

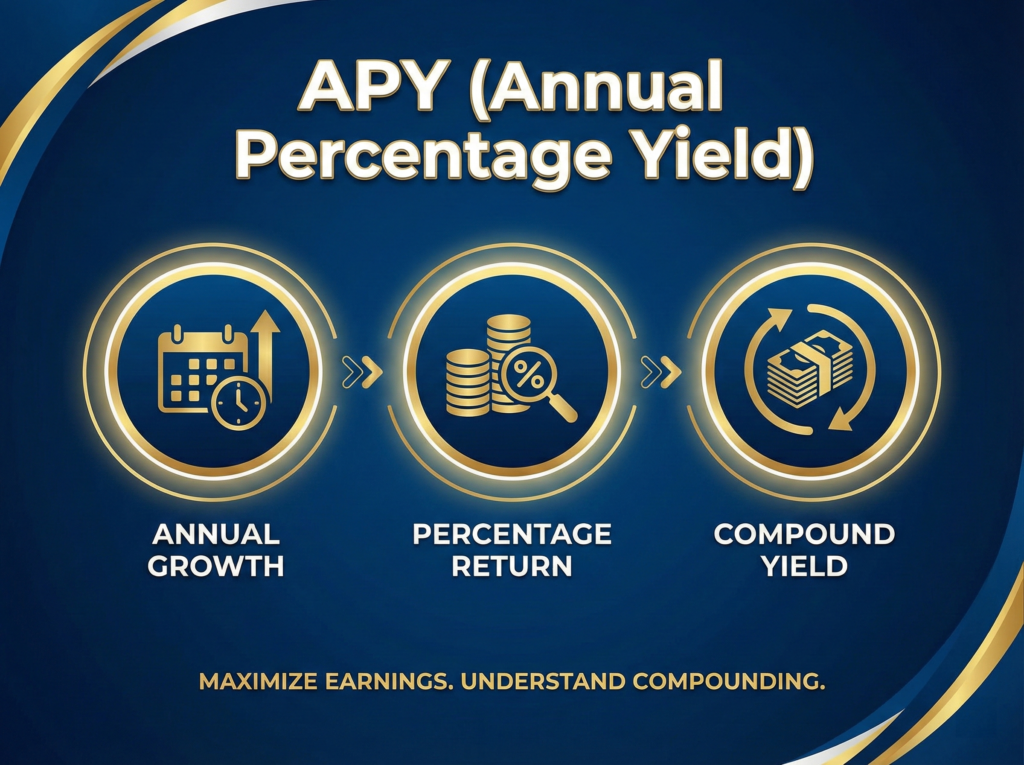

What Is APY?

APY (Annual Percentage Yield) is a metric that represents the actual annual return on an investment, taking into account compound interest. Unlike the nominal interest rate, which only reflects the interest charged or earned on the principal amount, APY provides a more accurate measure of how much you’ll earn in a year, factoring in the frequency with which interest is compounded.

For example, if you deposit $1,000 into a savings account offering a 5% interest rate compounded monthly, your APY will be slightly higher than the stated interest rate due to the monthly compounding. Over time, the interest you earn will be reinvested and begin earning interest itself, which increases your total return.

How Does APY Work?

Understanding APY is essential for choosing the right savings product. The way it works is based on two key concepts: interest rate and compounding frequency. Here’s how each one plays a role:

- Interest rate: This is the percentage of your balance that is paid as interest over a set period. For example, if the interest rate on a savings account is 5%, you would earn 5% of your balance in interest over the course of a year.

- Compounding frequency: This refers to how often interest is added to your account. The more frequent interest is compounded, the higher your APY will be. For example, interest compounded monthly will give a slightly higher return than interest compounded annually, even if both offer the same nominal interest rate.

Let’s use a real-life example to illustrate this. Imagine you deposit $5,000 in a savings account offering 5% interest, compounded monthly. After one year, you would earn $5,000 * (1 + 0.05/12) ^ 12 = $5,256.56. The additional $256.56 represents the interest earned, and your APY reflects this compounded amount, which is slightly higher than the nominal 5% rate.

Why Does APY Matter?

APY is critical because it provides a clearer understanding of how much you’re actually earning on your savings or investment over time. While the interest rate may look attractive, it doesn’t give you the full picture. APY factors in compounding, which makes a huge difference in your overall return.

When you’re choosing between different savings accounts, CDs, or investment products, APY is a key metric that helps you compare different options. It tells you how much interest you’ll earn after one year, allowing you to make an informed decision based on the effective return of each product.

For example, a high-yield savings account with a 3% APY will give you a higher return than an account offering 2% interest, even if both accounts advertise the same interest rate. The 3% APY accounts for compounding, which means you’re earning more money on your money.

How to Calculate APY

Calculating APY involves a formula that accounts for the nominal interest rate and the compounding frequency. The formula is:

APY = (1 + (r / n)) ^ n – 1

Where:

- r is the annual interest rate (expressed as a decimal, i.e., 5% = 0.05)

- n is the number of compounding periods per year (for example, 12 for monthly compounding)

So, if you have an account with an interest rate of 5% compounded monthly, the APY would be calculated as:

APY = (1 + (0.05 / 12)) ^ 12 – 1 = 0.0512 or 5.12%

This means that even though the nominal interest rate is 5%, the APY is slightly higher due to the compounding interest. This small increase makes a big difference when you’re looking to maximize your savings.

Why APY is Better Than Interest Rate

Many people make the mistake of comparing just the interest rate when evaluating savings accounts or other financial products. While interest rates are important, they don’t give you the full picture. APY, on the other hand, takes compounding into account, making it a more accurate reflection of the true returns.

For example, if two accounts offer the same interest rate (5%), but one compound interest monthly and the other annually, the account with monthly compounding will offer a higher APY and thus a better return. Always check the APY rather than just the interest rate when comparing different options.

Maximizing Your Savings with APY

Choose High-APY Accounts

Look for savings accounts, CDs, and other interest-bearing products with the highest APY. Online banks often offer higher APYs than traditional brick-and-mortar banks due to lower overhead costs.

Opt for Frequent Compounding

Choose accounts that compound interest monthly or even daily, as they typically provide higher APY compared to annual compounding.

Consider Long-Term Options

For higher APYs, consider locking your money in longer-term CDs or high-yield accounts. Though the access is limited, the higher returns can make it worth it.

Avoid Fees

Some accounts may offer a high APY, but they may come with fees that can diminish the returns. Make sure the account has low or no fees to truly benefit from the higher APY.

Conclusion: APY as a Key to Maximizing Your Savings

Understanding APY is crucial when choosing savings and investment products. By factoring in both the interest rate and the frequency of compounding, you can better evaluate which options will provide the highest returns on your savings. Whether you’re saving for a short-term goal or preparing for long-term financial growth, understanding how APY works will help you make smarter decisions and maximize your savings potential.

With the right savings strategy and an eye on APY, you can make your money work harder for you. Start applying these strategies today, and watch your savings grow over time with compound interest at the core of your financial success.

Related Articles

What Is APR? How It Works, Why It Matters, and How to Lower It