Investing isn’t only about finding the highest return. It’s also about choosing a strategy you can actually stick with when markets become unpredictable. That’s where risk tolerance matters. If your investments don’t match your comfort level, even a well-designed portfolio can feel stressful enough to abandon at the wrong time. A smart investment plan should reflect both your financial goals and your ability to stay steady through market ups and downs.

Understanding your risk tolerance can help you make better decisions, avoid emotional mistakes, and build a portfolio that feels sustainable over the long term.

What Risk Tolerance Really Means

Risk tolerance is your ability and willingness to handle fluctuations in the value of your investments. In simple terms, it reflects how much uncertainty you can accept in pursuit of higher potential returns.

Every investment involves some level of risk. Stocks can rise and fall sharply. Bonds are often steadier, but they still carry risks tied to interest rates, credit quality, and inflation. Cash and cash-like holdings may feel safer in the short term, but they can lose purchasing power over time if returns don’t keep up with rising costs. Risk tolerance helps answer an important question: how much volatility can you accept without panicking, losing sleep, or making impulsive decisions?

Why Risk Tolerance Matters in Investing

A portfolio that looks good on paper isn’t always the right one in real life. If it causes too much anxiety, you may sell during a downturn, stop contributing, or constantly change your strategy. Those reactions can do more damage than a temporary market decline.

This is why matching investments to your comfort level is so important. Rather than choosing the most aggressive approach, focus on an investment strategy that balances long-term growth with your personality, time horizon, and financial situation. When your portfolio aligns with your risk tolerance, you’re more likely to stay invested, keep contributing, and make decisions calmly instead of emotionally.

Risk Tolerance Isn’t the Same as Risk Capacity

People often use these terms interchangeably, but they aren’t identical. Risk tolerance is emotional and behavioral. It reflects how comfortable you feel with investment uncertainty. Risk capacity is more practical. It reflects how much financial risk you can afford to take.

For example, a younger investor with stable income, little debt, and decades before retirement may have high risk capacity because they have time to recover from market declines. But if that same investor becomes extremely anxious during volatility, their actual risk tolerance may be lower.

On the other hand, someone close to retirement may feel comfortable with market swings but have lower risk capacity because they may need access to their money sooner. A strong investment plan considers both. You need a portfolio that fits your emotions and your financial reality.

The Main Factors That Shape Your Risk Tolerance

Several things influence how much investment risk feels manageable. One of the most important is your time horizon. If you won’t need the money for many years, short-term volatility may matter less. Longer time horizons often allow investors to take more growth-oriented positions because there’s more time to recover from downturns.

Your income stability also matters. Someone with consistent earnings, strong savings, and low debt may feel more able to handle market fluctuations. A person with unstable income or limited emergency savings may feel more pressure when investments decline.

Life stage matters too. A person saving for retirement in their thirties may invest differently than someone nearing retirement or planning to use the funds within a few years. Personal experience also plays a role. Investors who have lived through major market declines may either become more cautious or more confident, depending on how they responded at the time.

Conservative, Moderate, and Aggressive Risk Profiles

Investment risk tolerance is often described in three broad categories: conservative, moderate, and aggressive.

A conservative investor usually prioritizes stability over higher growth potential. They may prefer investments with lower volatility, even if long-term returns are likely to be lower. This type of investor often values peace of mind and capital preservation.

A moderate investor typically wants a balance between growth and stability. They understand that some market volatility is normal but don’t want extreme swings in portfolio value. This is often a middle-ground approach for people with long-term goals who still want manageable risk.

An aggressive investor is usually more comfortable with short-term market drops in exchange for greater long-term growth potential. They may hold a larger percentage of stocks or other higher-volatility assets because they can tolerate bigger fluctuations. These labels are useful as a starting point, but real-life portfolios often fall somewhere between them.

How Your Time Horizon Changes the Risk Conversation

One of the clearest ways to evaluate investment risk is by asking when you’ll need the money. A long time horizon generally allows for more growth-oriented investing because short-term losses may have time to recover. Someone investing for retirement 25 years away may tolerate more stock exposure than someone saving for a house down payment in two years.

This matters because investment choices should match the purpose of the money. Funds needed soon usually shouldn’t be exposed to the same level of volatility as money invested for distant goals. A person may have a high tolerance for retirement account fluctuations but still keep short-term savings in safer, more stable accounts. Risk tolerance isn’t one fixed number across your entire financial life. It can vary depending on the goal.

Emotional Reactions Are a Useful Test

A lot of people think they can handle risk until markets actually fall. That’s why your emotional response to declines matters. Imagine your portfolio drops 10%, 20%, or more during a rough year. Would you stay calm and continue investing, or would you feel compelled to sell?

This question matters because behavior often shapes outcomes more than theory. An aggressive investment strategy only works if you can stay committed during stressful periods. If volatility makes you stop contributing or move everything to cash, the strategy may not fit you, even if it looks efficient on paper. A realistic assessment is far more valuable than an optimistic one. It’s better to build around the risk you can truly handle than the risk you wish you could handle.

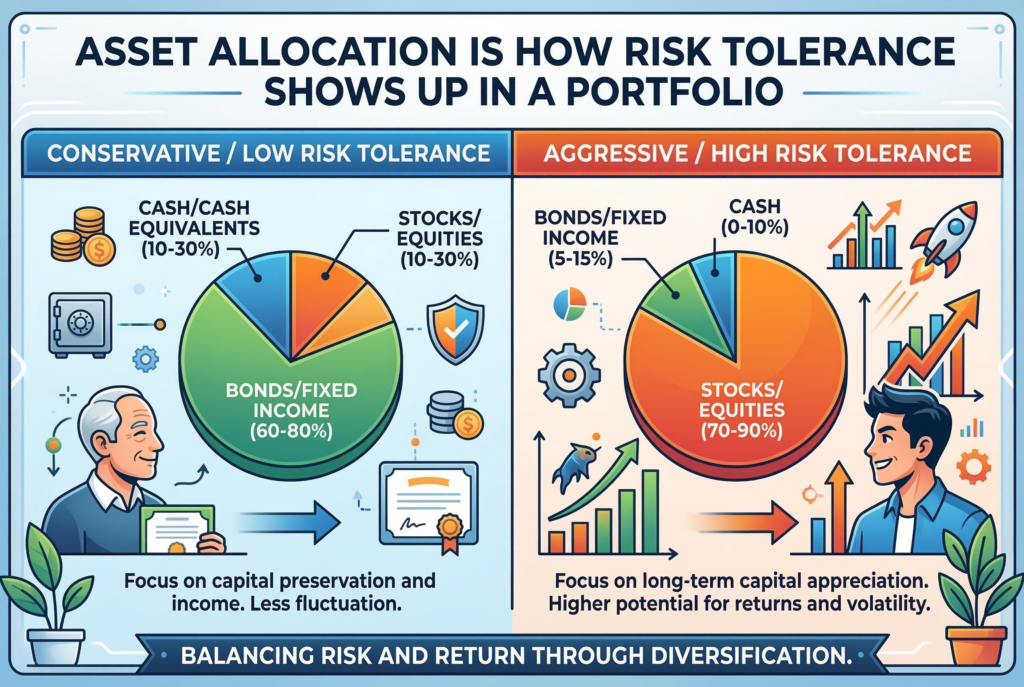

Asset Allocation Is How Risk Tolerance Shows Up in a Portfolio

Your asset allocation is one of the main ways risk tolerance gets translated into actual investments. Asset allocation refers to how your money is divided among stocks, bonds, cash, and possibly other asset categories.

In general, portfolios with more stocks tend to have higher growth potential and higher volatility. Portfolios with more bonds or cash equivalents tend to be steadier but may grow more slowly over time. A person with a higher risk tolerance may accept more stock exposure, while someone more cautious may prefer a more balanced or conservative mix. The goal involves taking a level of risk that supports your goals without pushing you into decisions driven by fear, rather than avoiding all risks.

How to Choose Investments That Match Your Comfort Level

A practical way to choose investments is to start with your goal, time horizon, and emotional response to volatility. Then consider whether your financial position supports taking more or less risk. Once those pieces are clear, you can build or choose investments that fit.

For many people, diversified mutual funds, index funds, or target-date funds can help simplify this process. These options often provide built-in diversification and a more structured risk approach than picking individual stocks without a broader plan.

The most important part is consistency. A portfolio that matches your comfort level should feel steady enough that you can continue contributing during both strong markets and weak ones.

Risk Tolerance Can Change Over Time

Your comfort with investment risk won’t necessarily stay the same forever. Income changes, family responsibilities, market experience, health concerns, and retirement timing can all affect how much risk feels appropriate.

That means it’s worth reviewing your investment mix periodically. A portfolio built for your twenties may not fit your forties or sixties in the same way. At the same time, changes shouldn’t be made impulsively. The goal is to adjust thoughtfully as your life changes, not react to every market headline. As your priorities evolve, your portfolio should evolve with them.

Avoid Common Mistakes When Assessing Risk Tolerance

One common mistake is assuming higher risk is always better because it may offer higher returns. In reality, too much risk can backfire if it leads to emotional investing mistakes. Another mistake is being too conservative for very long-term goals, which can limit growth and make it harder to keep pace with inflation.

It’s also easy to focus only on age and ignore behavior. Age matters, but it doesn’t tell the whole story. Two people of the same age may have very different risk tolerance because their income stability, family obligations, and emotional comfort levels differ. A thoughtful assessment is more useful than a generic one-size-fits-all rule.

Conclusion

Risk tolerance helps you choose investments that match both your financial goals and your emotional comfort level. When your portfolio reflects your ability to handle volatility, you’re more likely to stay invested, avoid impulsive decisions, and build long-term progress with more confidence. A strong investment plan takes into account your time horizon, risk capacity, life stage, and how you respond when markets become uncertain.

Risk can’t be eliminated from investing. The key is choosing a level of risk that aligns with your personal circumstances. When your investments align with your real comfort level, your strategy becomes easier to maintain, and that consistency is one of the most valuable advantages a long-term investor can have.