Taxable income is a central concept that every taxpayer needs to understand in order to navigate the complexities of the tax system and minimize their tax liabilities. In essence, taxable income refers to the portion of your total income that is subject to taxation after applying various deductions and exemptions. Understanding what counts as taxable income, how it’s calculated, and what steps you can take to reduce it can lead to significant tax savings over time.

This article will help you grasp the details of taxable income, how it’s calculated, and effective strategies for lowering your taxable income, which can ultimately lead to paying fewer taxes.

What Is Taxable Income?

Taxable income is the portion of your total income that the IRS considers subject to taxation. It’s calculated by subtracting allowable deductions from your gross income (the total amount of income you receive). Once taxable income is determined, it’s used to figure out how much you owe based on your tax bracket and marginal tax rate.

Your taxable income isn’t limited to wages or salary; it includes all types of income, such as business earnings, investment income, and sometimes even government benefits. Understanding what constitutes taxable income versus nontaxable income is essential for accurately filing taxes and taking advantage of available deductions.

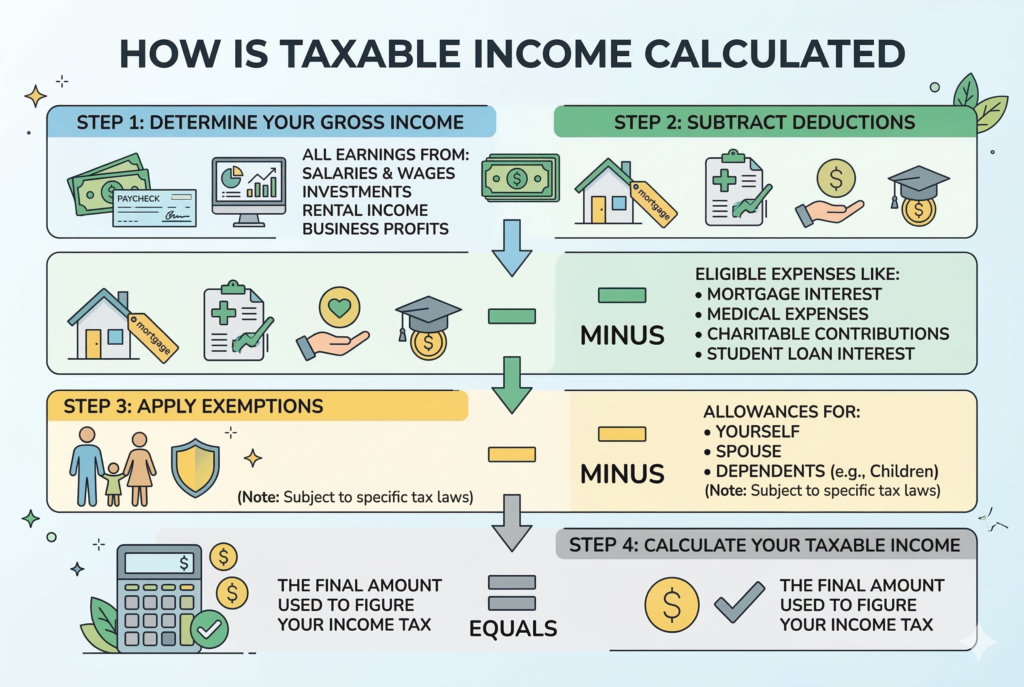

How Is Taxable Income Calculated?

Step 1: Determine Your Gross Income

Your gross income is the total of all money you earn from various sources. This includes wages from your job (reported on your W-2 form), self-employment income (from freelance work or business earnings), investment income (such as dividends or interest), rental income from property you own, and retirement distributions (from a 401(k) or IRA).

For example, if you earn $40,000 in salary, $5,000 from a side business, and $2,000 in dividends, your gross income for the year would be $47,000.

Step 2: Subtract Deductions

Once you have your gross income, you can reduce it by deductions. Deductions lower your taxable income and ultimately reduce the amount of tax you owe. There are two primary types of deductions:

Standard Deduction

This is a fixed amount that reduces your taxable income. The standard deduction varies depending on your filing status. For example, for a single filer, the standard deduction may be around $12,000 (this can change based on tax law updates).

Itemized Deductions

If your eligible expenses exceed the standard deduction, you can choose to itemize your deductions. Common itemized deductions include:

- Mortgage interest

- Charitable donations

- Medical expenses (above a certain threshold)

- State and local taxes (up to a limit)

For example, if you paid $3,000 in mortgage interest, donated $1,000 to charity, and had $2,500 in medical expenses that qualify, your total itemized deductions would be $6,500.

Step 3: Apply Exemptions

Exemptions have changed with recent tax reforms, but generally, they reduce taxable income for yourself and your dependents. In the past, you could claim an exemption for each dependent and for yourself. However, recent tax laws, like the Tax Cuts and Jobs Act, have temporarily suspended personal exemptions. While personal exemptions are no longer in play, understanding the concept can still be helpful when considering deductions for dependents and other family members.

Step 4: Calculate Your Taxable Income

Once you’ve subtracted deductions and exemptions, the remaining amount is your taxable income. This is the figure the IRS uses to determine the taxes you owe. For example, if your gross income is $47,000 and you claim a $12,000 standard deduction, your taxable income would be $35,000. At this point, you can determine your tax liability based on the tax brackets that apply to your taxable income.

What Counts as Taxable Income?

Several types of income are considered taxable, and it’s important to know which ones count toward your taxable income. Here are some common examples:

- Wages and salaries: The most common source of taxable income, which includes money you earn from working for an employer.

- Self-employment income: If you freelance, own a business, or are a contractor, the income you earn is taxable.

- Investment income: Earnings from interest, dividends, and capital gains from selling investments like stocks or bonds.

- Retirement distributions: Payments from retirement accounts such as 401(k)s and pensions are typically taxable when withdrawn.

- Rental income: Income from renting out property is taxable, though you can deduct certain expenses related to maintaining the property.

- Unemployment compensation: While unemployment benefits are meant to help when you lose your job, they’re still taxable.

- Gambling winnings: Money earned from gambling, whether at a casino, in the lottery, or through sports betting, is taxable.

- Bartering income: If you exchange goods or services (instead of using money), the fair market value of the goods or services you receive is taxable.

- Other miscellaneous income: This can include alimony payments, some types of insurance payouts, and rewards or prizes.

However, not all income is taxable. For example, child support payments and life insurance payouts are typically not subject to taxes.

How to Reduce Your Taxable Income

Contribute to Retirement Accounts

Contributing to tax-advantaged retirement accounts like a 401(k), Traditional IRA, or Health Savings Account (HSA) can reduce your taxable income. For example, contributions to a 401(k) are made with pre-tax dollars, meaning they reduce your taxable income in the year you contribute. This is particularly beneficial if you’re in a higher tax bracket.

For instance, if you contribute $5,000 to a 401(k) and your taxable income was $50,000, your new taxable income would be $45,000. This can lower your overall tax liability.

Use Tax-Advantaged Accounts for Healthcare and Education

Contributing to Health Savings Accounts (HSAs) or Flexible Spending Accounts (FSAs) can reduce taxable income. These accounts allow you to save money tax-free for medical expenses. Similarly, contributing to 529 Plans for education savings can provide tax-free growth and tax-free withdrawals when used for qualified education expenses.

Claim Deductions for Charitable Contributions

If you make charitable donations, you can deduct them from your taxable income if you itemize your deductions. This includes contributions to organizations like food banks, nonprofits, and even churches. Keep receipts or records of your donations to substantiate your claims.

Take Advantage of Tax Loss Harvesting

If you have investments that have lost value, you can sell them to offset capital gains from other investments. This strategy, known as tax loss harvesting, helps reduce taxable income by applying the losses against your gains. However, make sure to follow the wash-sale rule, which prevents you from buying back the same or substantially identical securities within 30 days of selling.

Consider Tax Credits

While tax deductions reduce your taxable income, tax credits directly reduce the amount of tax you owe. For example, the Child Tax Credit and the Earned Income Tax Credit (EITC) can significantly reduce the tax you owe, providing a larger refund or reducing your balance due.

Conclusion

Understanding taxable income is the first step in mastering your taxes. Knowing what counts as taxable income, how to calculate it, and how to reduce it allows you to make better financial decisions. Whether through retirement contributions, health savings, or strategic tax deductions, there are numerous ways to minimize your taxable income and reduce your tax liability.

By staying informed about available deductions and credits, and using smart tax strategies, you can keep more of your hard-earned money and ensure that you’re prepared for tax season. If you’re unsure about your situation, it’s always a good idea to consult with a tax professional to help you maximize your savings and avoid any costly mistakes.

Related Articles

- 2026 Income Tax Explained: Key Rules, Brackets, and Deductions You Need to Know

- Unexpected Tax Bills: Why They Happen and How to Prevent Them

- States With No Income Tax: Where You’ll Pay Less and How These States Offset Revenue

- 10 Common Tax Mistakes That Cost People Thousands Without Them Noticing

- How to Build a Tax Smart Financial Lifestyle for Long Term Financial Security

- 10 Best Tax Software of 2026 for Easy Filing, Accurate Returns, and Maximum Refunds