When you sell an asset, such as stocks, real estate, or bonds, you may have to pay capital gains tax on the profit you make from that sale. How much you pay depends largely on the duration of time you held the asset before selling it.

Understanding the difference between short-term and long-term capital gains is essential for managing your tax liability and making informed investment decisions. This article will explain the key differences between short-term and long-term capital gains, outline the tax rates for each, and provide practical strategies to help you save money on capital gains tax.

What Are Capital Gains?

Capital gains are the profits made from the sale of an asset, such as stocks, real estate, or bonds. The gain is calculated by subtracting the purchase price of the asset, known as the cost basis, from the sale price. For example, if you bought shares of stock for $5,000 and sold them for $7,000, your capital gain would be $2,000.

However, the amount of tax you owe on that gain depends on whether the asset was held for the short term (one year or less) or the long term (more than one year). The tax rates for short-term and long-term capital gains differ significantly.

Short-Term vs Long-Term Capital Gains: Key Differences

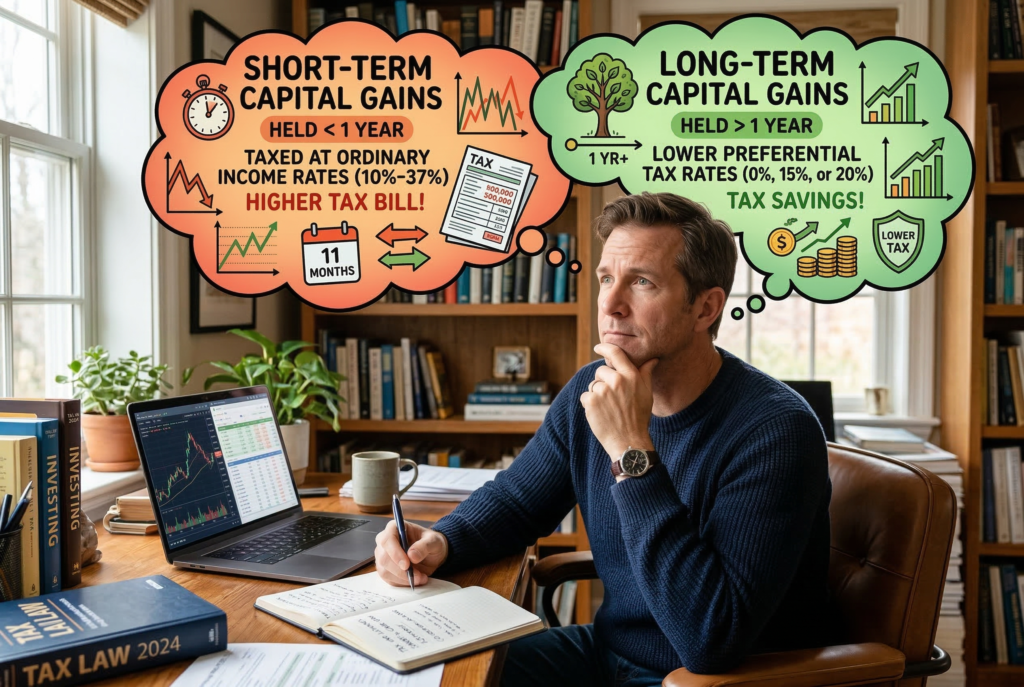

The primary difference between short-term and long-term capital gains is the holding period of the asset. If you sell an asset that you have held for one year or less, the gain is considered short-term. If you’ve held the asset for more than a year, the gain is considered long-term. This distinction is important because short-term capital gains are taxed at your ordinary income tax rate, which could be as high as 37%, depending on your income level. Long-term capital gains, on the other hand, are typically taxed at a lower rate.

Short-Term Capital Gains

When you sell an asset that you’ve held for one year or less, the gain is classified as a short-term capital gain. This gain is taxed at your ordinary income tax rate, which ranges from 10% to 37% based on your income bracket. Because short-term gains are taxed as ordinary income, they’re usually subject to a higher tax rate than long-term capital gains, which can lead to a larger tax liability.

For example, if you’re in the 24% tax bracket, and you sell an asset for a $5,000 profit, you would owe $1,200 in taxes on that short-term capital gain. This is significantly higher than the taxes you would pay on the same gain if it were considered a long-term capital gain.

Long-Term Capital Gains

Long-term capital gains are gains on assets held for more than one year. The tax rates for long-term gains are generally lower than for short-term gains, encouraging long-term investment. For the tax year 2026, the long-term capital gains tax rates are:

- 0% for individuals with taxable income up to $44,625 for single filers or $89,250 for married couples filing jointly.

- 15% for taxable income between $44,626 and $492,300 for single filers, or between $89,251 and $553,850 for married couples filing jointly.

- 20% for taxable income over $492,300 for single filers or $553,850 for married couples filing jointly.

For example, if you’re in the 15% long-term capital gains bracket, and you sell an asset for a $5,000 profit, you would only owe $750 in taxes on that gain. This is a much lower tax rate compared to short-term capital gains.

Key Differences in Tax Rates

The most significant difference between short-term and long-term capital gains is the tax rate applied. While short-term gains are taxed as ordinary income, long-term gains are taxed at preferential rates: 0%, 15%, or 20%, depending on your income. This makes long-term investments more tax-efficient, as they’re subject to lower taxes than short-term investments.

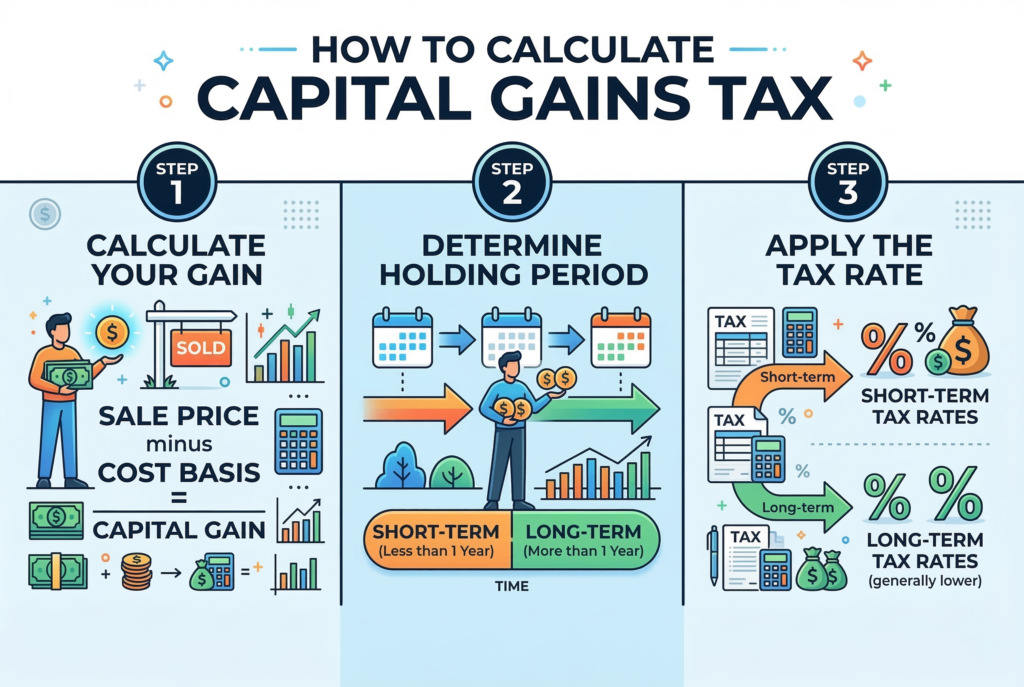

How to Calculate Capital Gains Tax

To calculate your capital gains tax, you’ll need to determine your capital gain (the difference between the purchase price and the sale price) and then apply the correct tax rate based on the holding period.

- Calculate your gain: Subtract the purchase price (cost basis) of the asset from the sale price. This gives you your capital gain.

- Determine holding period: Check how long you’ve held the asset. If it’s more than one year, it qualifies as long-term. If it’s one year or less, it’s a short-term gain.

- Apply the tax rate: Use the appropriate tax rate based on whether your gain is short-term or long-term.

For example, if you sold a stock for $10,000 that you purchased for $6,000, your capital gain is $4,000. If you held the stock for more than a year, it would be subject to long-term capital gains tax, and you would apply the relevant tax rate based on your income bracket.

Strategies to Reduce Capital Gains Tax

1. Hold Assets for the Long Term

One of the easiest ways to reduce your capital gains tax burden is by holding onto your investments for more than one year. Long-term capital gains are taxed at a much lower rate than short-term gains, so this strategy allows you to keep more of your profits.

2. Use Tax-Advantaged Accounts

Investing through tax-advantaged accounts like IRAs or 401(k)s can help you avoid capital gains taxes. In particular, Roth IRAs allow for tax-free growth and tax-free withdrawals of long-term capital gains. Contributions to traditional retirement accounts, such as a 401(k), also allow you to defer taxes on capital gains until you retire, which can be advantageous if you are in a lower tax bracket when you withdraw the funds.

3. Offset Gains with Losses

Tax-loss harvesting is a strategy where you sell investments that have decreased in value to offset gains from other investments. If you have more losses than gains, you can use the excess losses to offset up to $3,000 of ordinary income ($1,500 if married filing separately), and carry forward any remaining losses to future years.

4. Invest in Opportunity Zones

Opportunity Zones are designated areas that encourage investment by offering tax incentives, including deferring and possibly eliminating capital gains taxes. By investing in qualified Opportunity Zones and holding the investment for at least 10 years, you may be able to avoid paying taxes on any capital gains from those investments.

5. Donate Appreciated Assets to Charity

Donating appreciated assets, such as stocks or real estate, to a qualified charity can allow you to avoid paying capital gains tax. You can also claim a charitable deduction for the fair market value of the donated asset, further reducing your overall tax liability.

How State Taxes Impact Capital Gains

While the IRS sets federal capital gains tax rates, each state has its own rules regarding capital gains taxation. Some states, such as California and New York, tax capital gains as ordinary income, while others, like Florida and Texas, don’t impose any state-level capital gains tax.

Before making an investment, especially if you live in a state with high capital gains tax rates, it’s important to understand how your state taxes capital gains and plan accordingly.

Conclusion: Plan Ahead to Save on Capital Gains Tax

Understanding capital gains tax is an essential part of managing your investments and minimizing your tax burden. By holding investments for longer than a year, utilizing tax-advantaged accounts, and employing strategies like tax-loss harvesting, you can significantly reduce the amount you owe in capital gains taxes.

Planning ahead and considering your tax situation when making investment decisions can save you money in the long run, ensuring that your hard-earned gains don’t get swallowed up by taxes. With the right strategies in place, you can optimize your investment returns and build wealth efficiently while keeping your tax liabilities in check.