A brokerage account is one of the most common tools for investing outside of retirement plans. It gives you access to assets like stocks, ETFs, mutual funds, bonds, and sometimes more advanced investments, all through one account. For people in the United States who want flexibility, fewer withdrawal restrictions, and more control over how they invest, understanding how a brokerage account works is an important part of building a smart financial plan.

What Is a Brokerage Account?

A brokerage account is an investment account that lets you buy, sell, and hold financial assets through a brokerage firm. Unlike retirement accounts such as a 401(k) or IRA, a standard taxable brokerage account doesn’t usually come with special tax advantages, but it offers much more flexibility in how and when you use your money.

Once the account is funded, you can use it to invest in a variety of securities. Common choices include individual stocks, exchange-traded funds (ETFs), mutual funds, bonds, and cash equivalents. Some brokerage platforms also offer options trading, margin accounts, and access to more specialized investments, though those features aren’t necessary for every investor.

A brokerage account can be opened by an individual, jointly with another person, or in certain custodial arrangements for minors. The structure depends on who owns the assets and how the money is meant to be used.

How a Brokerage Account Works

A brokerage account works by acting as the holding place for your investments. After opening the account with a brokerage firm, you deposit money into it from a linked bank account. From there, you can place trades and choose how to invest the cash.

If you decide to buy shares of a stock or ETF, the brokerage executes that transaction on your behalf. Once purchased, the investment stays in your account until you sell it. The value of the account rises or falls based on market performance, any income generated from dividends or interest, and your ongoing contributions or withdrawals.

One major difference between a brokerage account and a retirement account is access. In most cases, you can withdraw money from a taxable brokerage account whenever you want. There’s no age-based penalty for taking funds out. That flexibility makes it useful for goals that aren’t strictly tied to retirement. Still, flexibility doesn’t mean there are no tax consequences. Selling investments for a profit may create capital gains taxes, and dividends or interest earned in the account may also be taxable.

What You Can Hold in a Brokerage Account

A brokerage account can hold a wide range of assets, which is one reason it appeals to many investors. The exact menu depends on the brokerage, but the most common holdings include:

- Stocks give investors ownership in publicly traded companies and the potential for long-term growth.

- ETFs are baskets of investments that trade like stocks and are often used for diversification and lower-cost investing.

- Mutual funds pool money from many investors and may be actively managed or passively track an index.

- Bonds can provide income and may reduce portfolio volatility compared with stocks alone.

Some brokerage accounts also allow you to hold money market funds, certificates of deposit through brokered products, or other short-term instruments.

Because of this flexibility, a brokerage account can support many investing styles, from simple passive investing to more active trading. For most long-term investors, broad diversification and low-cost funds are often more practical than trying to trade frequently.

Key Benefits of a Brokerage Account

No Early Withdrawal Penalty

One of the biggest advantages is access to your money. Unlike many retirement accounts, a brokerage account doesn’t usually impose an age-based penalty for withdrawals. That makes it useful for medium-term goals, major purchases, or general wealth building outside of retirement-only planning.

Broad Investment Flexibility

A brokerage account gives you the freedom to invest in a wide range of assets. Whether you want to build a portfolio of ETFs, buy individual stocks, invest in bonds, or keep part of the balance in cash-like holdings, the account can usually support that mix.

No Annual Contribution Limits

Another important benefit is that taxable brokerage accounts generally don’t have the same annual contribution caps found in accounts like IRAs. If you’ve already maxed out retirement contributions or simply want to invest more, a brokerage account can give you additional room.

Useful for Multiple Financial Goals

A brokerage account can serve many purposes. Some people use it for long-term investing. Others use it for a future home purchase, supplemental retirement savings, or building wealth that stays accessible along the way.

Easy to Manage Alongside Other Accounts

For many households, a brokerage account works well as a complement to retirement accounts, emergency savings, and other parts of a broader financial strategy. It fills the gap between short-term cash and tax-advantaged retirement savings.

Brokerage Account vs. Retirement Account

A brokerage account and a retirement account can both be used for investing, but they serve different roles.

A retirement account like a 401(k) or IRA is built for long-term retirement saving and usually comes with tax advantages. In exchange, there may be contribution limits, eligibility rules, and penalties for early withdrawals.

A taxable brokerage account doesn’t provide those same upfront tax benefits, but it offers more freedom. You can contribute as much as you want in most cases, invest broadly, and withdraw funds without the retirement-account penalty structure.

This doesn’t mean one is always better than the other. For many people, the smartest approach is using both. Retirement accounts may come first because of the tax advantages, while a brokerage account can add flexibility once those accounts are in place or when money may be needed before retirement age.

Potential Drawbacks to Understand

A brokerage account offers flexibility, but it also comes with tradeoffs.

The biggest one is taxes. Because it’s a taxable account, investment income and realized gains may create annual tax obligations. If you sell an investment at a profit, you may owe capital gains tax. Dividends and interest may also be taxable, even if you don’t withdraw the money.

Another drawback is behavioral risk. Since the account is easy to access, some investors are more tempted to sell during market declines or use the money for nonessential spending. That can interrupt long-term compounding.

Fees can also vary. Many brokerages now offer commission-free stock and ETF trading, but that doesn’t mean the account is cost-free. Expense ratios on mutual funds or ETFs, advisory fees, account fees, and other charges can still affect long-term returns.

Finally, the wide range of choices can overwhelm new investors. Too many options may lead to confusion, overtrading, or portfolios that are more complicated than necessary.

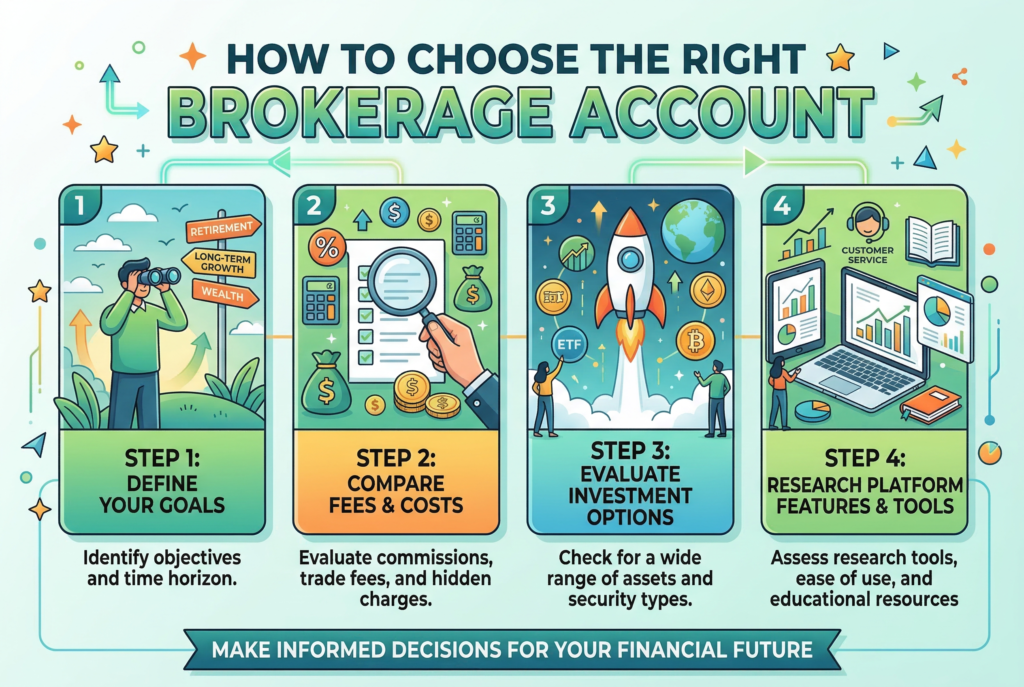

How to Choose the Right Brokerage Account

Choosing the right brokerage account starts with understanding your goals. The best account for active trading may not be the best one for long-term investing, beginner-friendly tools, or low-cost portfolio building.

Look at Fees and Costs

Start by reviewing account fees, trading commissions, fund expense ratios, and any maintenance charges. Even when trading is commission-free, underlying investment costs still matter. Lower fees can make a meaningful difference over time.

Review Investment Options

A good brokerage should offer the types of investments you actually plan to use. For many investors, that means easy access to ETFs, index funds, mutual funds, and bonds. If you want a simple long-term account, you may not need advanced trading features.

Check the Platform and User Experience

The platform should be easy to understand and use. Good research tools, a clear dashboard, strong mobile access, and reliable statements all help. Beginners often benefit from an interface that makes investing feel less intimidating.

Consider Customer Support and Education

Some brokerages do a better job than others with education, planning tools, and customer service. If you’re new to investing, strong support can make a real difference, especially when learning account features, tax documents, or trade basics.

Decide Whether You Want Self-Directed or Managed Investing

Some brokerage firms offer both self-directed accounts and automated investing options. A self-directed account gives you more control, while a managed or robo-advisor option may help if you prefer a hands-off approach.

When a Brokerage Account Makes Sense

A brokerage account often makes sense when you want to invest money that isn’t locked into retirement rules. It can be a strong choice for people saving for medium- or long-term goals, investors who’ve already contributed to retirement accounts, or anyone who wants more flexibility in accessing their funds.

It’s also useful for building wealth beyond employer-sponsored plans. If you want to keep investing after reaching your IRA or 401(k) contribution limits, a brokerage account is often the next step. For beginners, it can also be a practical entry point, as long as the account is used thoughtfully and the investments match the person’s time horizon and risk tolerance.

Smart Ways to Use a Brokerage Account

A brokerage account tends to work best when paired with a clear purpose. Some investors use it for long-term investing through diversified ETFs or index funds. Others use it for goals that are still years away but not as distant as retirement.

The key isn’t treating the account like random extra money. When it has a defined role in your financial plan, it becomes easier to decide how aggressively to invest, how much risk to take, and when to withdraw funds. For many investors, a simple strategy built around diversified, low-cost funds is enough. Complexity isn’t always better. Consistency usually matters more than trying to outguess the market.

Conclusion

A brokerage account is a flexible investment account that allows you to buy and hold assets like stocks, ETFs, mutual funds, and bonds without the withdrawal restrictions that come with many retirement plans. Its biggest strengths include broad investment choice, easy access to your money, and no standard annual contribution limits. Those features make it useful for a wide range of financial goals, from long-term wealth building to medium-term investing.

Still, flexibility comes with tradeoffs, especially around taxes and the need for disciplined investing. Choosing the right brokerage account means looking closely at fees, investment options, platform quality, and how the account fits into your overall financial strategy. When used carefully, it can be a powerful tool for growing money and expanding your investing options beyond retirement accounts.