When it comes to purchasing a car, understanding interest rates is one of the most crucial aspects of financing. Your interest rate can significantly impact your monthly payments and the overall cost of the vehicle. The APR (Annual Percentage Rate) reflects the true cost of borrowing money, including both the interest and any additional fees. For those who are new to the concept or looking to secure the best deal, it’s essential to understand how car loan interest rates work, what factors affect them, and how you can lower them.

What Is a Car Loan Interest Rate?

A car loan interest rate is the percentage of the loan amount that a lender charges as a fee for borrowing money. This interest is paid over the life of the loan and is a key factor in determining how much you’ll pay each month. The interest rate can vary depending on several factors, including your credit score, loan term, and the type of car you’re purchasing.

The car loan interest rate is often expressed as an APR (Annual Percentage Rate), which includes not only the interest on the loan but also any fees or additional charges that come with the loan agreement. While you may see nominal interest rates advertised by dealerships or banks, the APR gives you a more accurate idea of the total cost you’ll pay over the course of the loan.

How Do Car Loan Interest Rates Work?

The way car loan interest rates work can significantly affect your monthly payments and the overall amount you pay for the car. When you take out a loan, the lender charges interest on the principal amount plus any fees associated with the loan.

If your loan has a fixed interest rate, the rate remains the same throughout the loan term, and your monthly payments will stay consistent. In contrast, with a variable interest rate, the rate can change over time, which could cause fluctuations in your monthly payments.

The way interest is applied to the loan depends on whether it’s a simple interest loan or compound interest loan. Most car loans use simple interest, meaning the interest is calculated only on the principal balance of the loan. As you make payments, the interest is gradually reduced as the loan balance decreases.

Key Factors That Affect Your Car Loan Interest Rate

Several factors can influence the interest rate you’ll be offered when taking out a car loan. These factors include your credit score, the term of the loan, the amount of the loan, and the type of car you’re buying. Understanding these factors can help you secure a lower interest rate and reduce the overall cost of your loan.

Credit Score

Your credit score is one of the most important factors affecting your car loan interest rate. A higher credit score indicates to lenders that you’re a lower risk, and as a result, you’re likely to qualify for a lower interest rate. On the other hand, if your credit score is poor, lenders may charge you a higher interest rate to compensate for the perceived risk.

Loan Term

The length of the loan (how long you have to repay it) can also impact the interest rate. Shorter loan terms (such as 36 months) typically come with lower interest rates, while longer terms (such as 72 months) often have higher interest rates. This is because longer loan terms pose more risk for lenders since there’s more time for interest rate changes or the possibility that you’ll default.

Down Payment

A larger down payment can help lower your car loan interest rate. When you pay more upfront, the lender is taking on less risk, which may result in a better interest rate for you. A down payment of at least 20% is often recommended to reduce both your loan balance and your interest costs.

New vs. Used Cars

The type of car you’re purchasing also impacts your interest rate. New cars generally come with lower interest rates because they’re considered less risky for lenders due to their higher resale value. On the other hand, used cars might come with higher interest rates because their value can depreciate more quickly.

Lender Type

Different lenders, whether it’s a bank, credit union, or dealership, offer different interest rates. Credit unions often offer the best interest rates because they’re non-profit organizations focused on benefiting their members. However, dealership financing may offer promotional rates, but they tend to have stricter terms or higher overall costs, so it’s important to shop around.

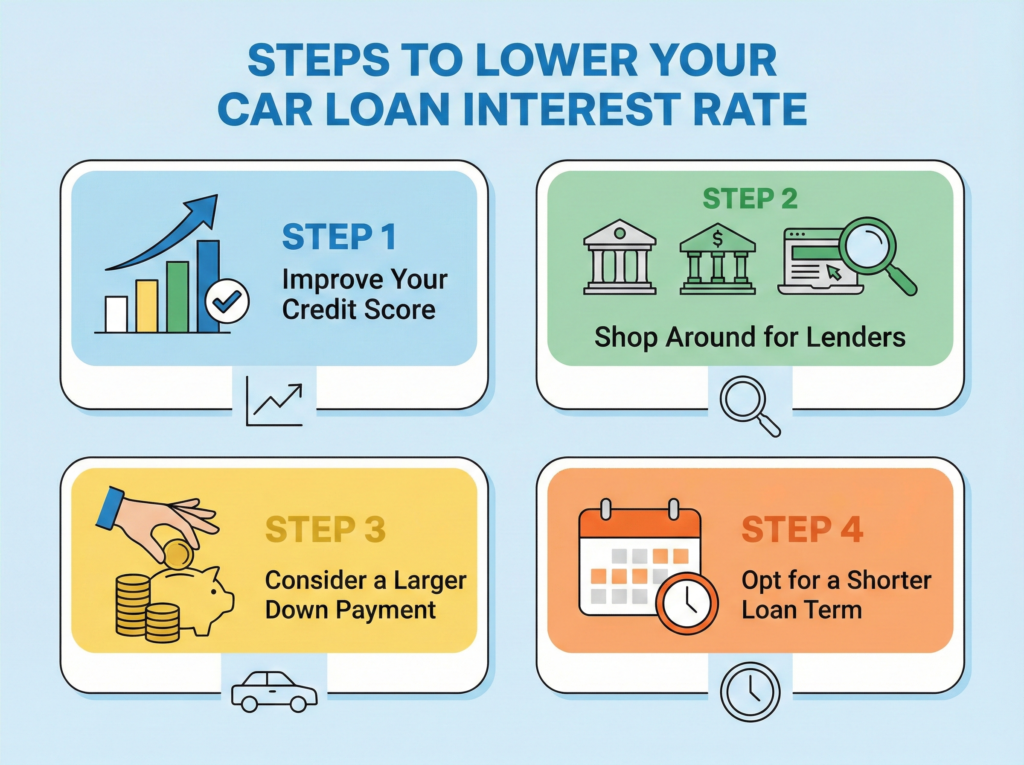

How to Lower Your Car Loan Interest Rate

Improve Your Credit Score

If your credit score is on the lower end, take some time to improve it before applying for a car loan. Pay off existing debt, ensure you’re making timely payments, and keep your credit utilization low. A higher credit score will directly lead to a lower interest rate.

Shop Around for Lenders

Don’t settle for the first loan offer you receive. Compare interest rates from banks, credit unions, online lenders, and dealerships to find the best deal. Be sure to check if the lender offers any special promotions or discounts that could lower your rate.

Consider a Larger Down Payment

If possible, consider making a larger down payment to reduce the amount you need to borrow. A larger down payment reduces the lender’s risk and could help you secure a lower interest rate.

Opt for a Shorter Loan Term

If you can afford it, choose a shorter loan term. While the monthly payments will be higher, you’ll generally be offered a lower interest rate, and you’ll pay less interest over the life of the loan.

How Car Loan Interest Rates Affect Your Monthly Payment

Car loan interest rates can significantly impact your monthly payments. A lower interest rate will result in lower monthly payments, making the loan more manageable. In contrast, a higher interest rate can lead to higher monthly payments and more money paid in interest over the life of the loan.

For example, if you borrow $20,000 at a 6% interest rate over 60 months, your monthly payment will be around $386. However, if your interest rate is 8%, the monthly payment will increase to around $406. Over the course of the loan, this can add up to thousands of dollars in additional interest payments.

Conclusion: How to Secure the Best Car Loan Interest Rate

Understanding car loan interest rates and how they work is essential for making an informed decision when purchasing a car. By knowing how factors such as your credit score, loan term, and down payment affect your interest rate, you can take steps to secure the best possible deal. Whether you’re buying a new car or a used one, the right car loan can save you money in the long run.

By following these tips to lower your interest rate and comparing offers from multiple lenders, you can reduce your monthly payment, save on interest, and make a financially sound decision when buying your next car.

Related Articles

Electric Vehicle Tax Credit 2025: Eligibility Rules, Income Limits, and Simple Steps to Claim