If you’ve ever looked at your savings account and thought, “There has to be a better way to earn something on this money,” this article is worth a closer look. For many Americans, such as renters saving for a move, homeowners planning a renovation, couples juggling shared goals, or busy professionals just trying to be smarter with cash, certificates of deposit, or CDs, often come up as a quiet but tempting option.

They aren’t flashy, and they won’t make headlines. But when used the right way, CDs can be one of the most reliable tools in a real-life financial plan.

What Is a Certificate of Deposit (CD)?

A certificate of deposit (CD) is a type of bank account that pays a fixed interest rate for a set period of time, called the term. In exchange for that guaranteed rate, you agree to leave your money untouched until the CD reaches its maturity date. It’s essentially a way of telling the bank you don’t need access to those funds right away, and in return, the bank rewards your patience with a higher rate than a typical savings account.

CD terms usually range from about three months to five years, and the interest rate is locked in from day one. CDs generally don’t charge monthly fees, are FDIC insured up to $250,000 per depositor at insured banks, and provide predictable returns. The main trade-off is limited flexibility, taking money out early typically results in an early withdrawal penalty.

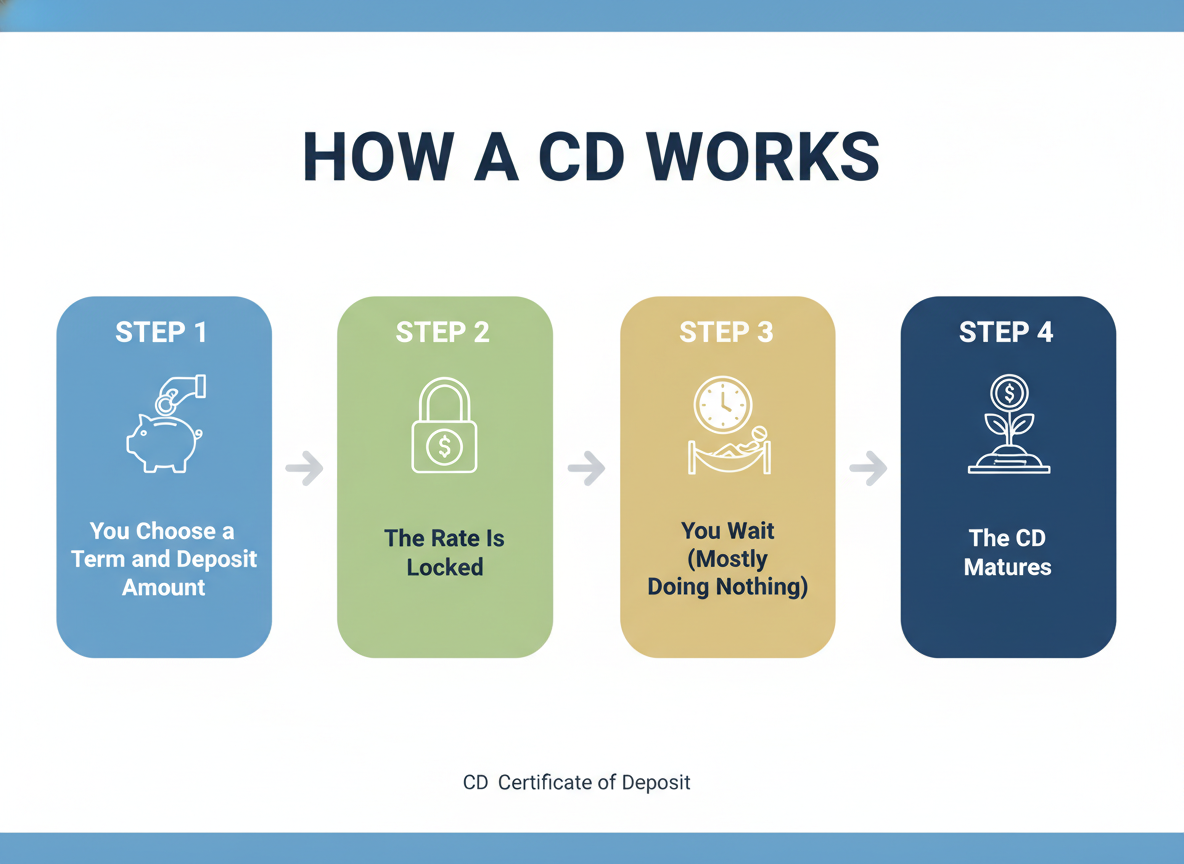

How CDs Work

Step 1: You Choose a Term and Deposit Amount

You decide how much money to put in and how long you can leave it alone. Common choices are 6 months, 1 year, or 2 years.

Step 2: The Rate Is Locked

Once the CD is open, the rate doesn’t change, even if the market shifts. That predictability is the entire appeal.

Step 3: You Wait (Mostly Doing Nothing)

Your money earns interest quietly in the background. You usually can’t add more money during the term.

Step 4: The CD Matures

At maturity, you receive your original deposit (the principal) along with all the interest you’ve earned. At that point, you can withdraw the money, move it to another account, or roll it into a new CD if you want to continue earning interest.

Why People Choose CDs (The Real Benefits)

Predictable, Guaranteed Returns

With CDs, you know exactly how much you’ll earn from the start. That predictability can be especially reassuring if you’re saving for a specific date, want stable returns without surprises, or feel worn out by rates that seem to change every few weeks.

Low Risk, High Peace of Mind

Because CDs are federally insured at most banks and credit unions, they’re considered one of the safest places to store cash. That makes them appealing during uncertain economic periods or when you simply don’t want stress attached to your savings.

Higher Rates Than Regular Savings (Usually)

While high-yield savings accounts can be competitive, CDs often offer better rates when you’re willing to lock money up for a bit.

The Trade-Offs (What CDs Don’t Do Well)

One downside of CDs is limited access to your money. If you break a CD early, you’ll likely pay a penalty, often equal to several months’ worth of interest, which is why emergency funds don’t belong in CDs. Another trade-off is lack of flexibility if rates rise. Once you lock in a rate, you’re stuck with it until maturity, even if better rates become available later. And while CDs offer stability, they typically grow more slowly than stocks or diversified investments over the long term, making them better for preserving money than aggressively growing it.

When a CD Makes Sense (And When It Doesn’t)

CDs are a good fit if:

- You’re saving for a known expense (down payment, wedding, tuition).

- You don’t need the money until a specific date.

- You want returns without market risk.

- You’re tempted to spend money that’s sitting in savings.

CDs aren’t usually a good fit if:

- This is your emergency fund.

- You need frequent access to the money.

- You’re focused on long-term investing growth.

- You’re still building savings little by little.

Common Types of CDs You Might See

| Traditional CDs | The standard option: fixed rate, fixed term, and penalty for early withdrawal. |

|---|---|

| No-penalty CDs | You can withdraw early without a fee, but the rate is usually lower. This can be a good option if you want flexibility. |

| High-yield CDs | These offer above-average rates and are often found at online banks with lower overhead. |

| Jumbo CDs | Require large deposits (often $50,000+). Sometimes it can offer better rates. |

| IRA CDs | Held inside a retirement account. They offer safety and predictability but still follow IRA withdrawal rules. |

What Happens When a CD Matures?

When your CD reaches maturity, there’s usually a short grace period, often around 7 to 10 days, during which you can withdraw the money, transfer it to another account, or open a new CD. If you don’t take action during that window, many banks will automatically renew the CD, often at a lower rate. Keeping track of maturity dates can help you avoid auto-renewals and make sure you don’t miss better options.

A Smarter Strategy: CD Laddering

How CD Laddering Works

Instead of one large CD, you split your money across multiple CDs with different terms. For example: $2,000 in a 1-year CD, $2,000 in a 2-year CD, and $2,000 in a 3-year CD. Each year, one CD matures. You can use the cash or reinvest it, keeping flexibility while still earning higher rates over time.

CDs vs. Savings Accounts: Which Is Better?

Savings accounts make more sense when you need easy access to your money, are building an emergency fund, or plan to add funds regularly over time. Their flexibility allows you to deposit or withdraw without penalties, which is important for goals that may change or require quick access.

CDs work better when your goal has a clear timeline, you don’t need to touch the money until a specific date, and you value predictable, guaranteed returns.

In practice, many people use both: keeping flexible savings for emergencies and short-term needs, while using CDs for planned goals with defined timeframes.

A Quick Reality Check Before You Open a CD

Before committing, ask yourself:

- Do I truly not need this money until the term ends?

- Am I comfortable with limited flexibility?

- Does this fit into my broader financial plan?

If the answers feel solid, a CD can be a calm, dependable part of your strategy.

The Bottom Line

Certificates of deposit are designed for real life: planned expenses, cautious savers, and moments when peace of mind matters more than chasing returns. If you use CDs thoughtfully, they can protect your savings, reduce temptation, and help your money grow quietly in the background.

They won’t replace investing. They won’t solve every financial problem. But for the right goal, at the right time, CDs do exactly what they promise, and that’s their strength.