Building a solid credit score is essential for your financial health, and if you’re just starting out or trying to repair your credit, credit builder cards are an excellent tool. These cards help individuals with limited or poor credit history establish or rebuild their credit score by offering an opportunity to demonstrate responsible borrowing and timely repayment. In this guide, we’ll break down how credit builder cards work, who should use them, and provide 10 actionable tips to help you maximize their benefits and build your credit faster.

What Are Credit Builder Cards?

Credit builder cards are specialized credit cards designed to help those with no credit or poor credit improve their credit score. These cards typically have low credit limits, and the interest rates can be higher than traditional credit cards. However, they offer an opportunity for you to show responsible credit use, which is key to improving your credit score.

What sets credit builder cards apart from regular credit cards is that they require a security deposit in some cases (for secured credit cards) or have very limited spending power. This deposit essentially serves as collateral, which makes these cards accessible to people with limited or damaged credit histories. The credit card issuer reports your payments to the major credit bureaus (Experian, TransUnion, and Equifax), helping you build a positive credit history.

How Do Credit Builder Cards Work?

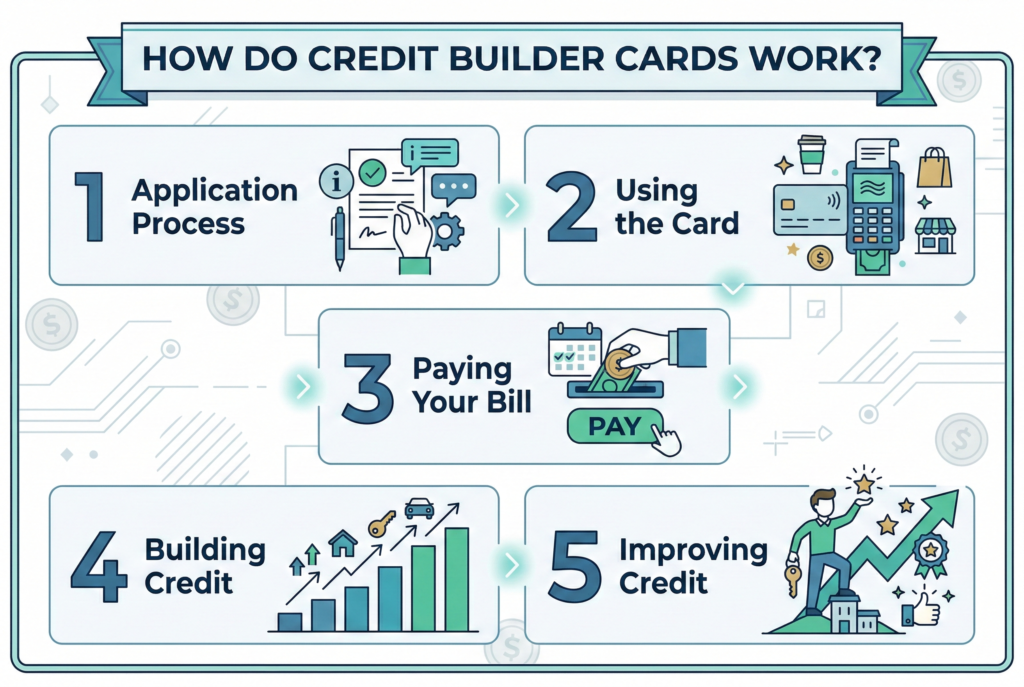

Application Process

First, you apply for a credit builder card. If you’re approved, the credit card issuer will either set a low credit limit or ask for a deposit if the card is secured. This deposit is often equal to your credit limit.

Using the Card

Once you have the card, you can use it just like any other credit card to make purchases, both in-store and online. Use it regularly, but only for purchases you can afford to pay off.

Paying Your Bill

To make the most of a credit builder card, you must pay your balance in full each month. Paying on time and avoiding carrying a balance will help your credit score improve over time by showing that you can manage your debt responsibly.

Building Credit

As the card issuer reports your payment history to the credit bureaus, you begin to build a positive credit history. Over time, this helps increase your credit score, especially if you’re diligent about making payments and keeping balances low.

Improving Credit

As your credit score improves, you may become eligible for higher-limit cards or loans with better interest rates. With consistent on-time payments, your credit score will rise, allowing you to qualify for more credit products at lower rates.

10 Smart Ways to Build Credit Faster with Credit Builder Cards

1. Make On-Time Payments Every Month

The most important factor in building credit is paying on time. Make sure to always pay your credit card bill by the due date. Consider setting up automatic payments to ensure you never miss a payment, as late payments can damage your credit score.

2. Pay Off Your Balance in Full Each Month

To avoid interest charges and improve your credit score faster, always pay your balance in full each month. Carrying a balance can result in high-interest costs, which add up over time, diminishing the value of using a credit card to build credit.

3. Keep Your Credit Utilization Low

Credit utilization refers to the percentage of your available credit that you’re using. A lower utilization ratio (below 30%) is ideal for improving your credit score. Try to only use a portion of your available credit and pay it off each month.

4. Don’t Apply for Too Many Cards at Once

Each time you apply for a credit card, the issuer will conduct a hard inquiry on your credit report, which can cause a temporary dip in your credit score. Avoid applying for multiple credit cards within a short period.

5. Check Your Credit Report Regularly

Monitoring your credit report is essential to track your progress and ensure the on-time payments are reflected. You can get a free report from each of the three major credit bureaus annually at AnnualCreditReport.com. Look for any discrepancies or errors that may affect your credit score.

6. Use Your Card Regularly

Using your credit builder card for small, manageable purchases each month is a great way to demonstrate that you can handle credit responsibly. Just make sure you don’t overextend yourself, paying off the balance monthly is key.

7. Avoid Missing Payments by Setting Up Reminders

Set reminders on your phone or use an app that helps you keep track of payment due dates. Staying organized with your payment schedule ensures you never miss a payment, which is crucial to maintaining a healthy credit score.

8. Consider a Secured Credit Builder Card

If you’re just starting or have difficulty getting approved for unsecured cards, consider a secured credit builder card. This type of card requires a security deposit as collateral, making it easier to qualify for. The deposit serves as your credit limit, and after you demonstrate responsible use, you may be able to transition to an unsecured card.

9. Avoid High Fees

While some credit builder cards come with annual fees, make sure to choose a card with low fees. Excessive fees can erode the value of your efforts to build credit. Compare different options and choose the card that provides the best benefits without hidden costs.

10. Consider Credit Builder Loans

In addition to credit builder cards, consider applying for a credit builder loan, which allows you to borrow a small amount and pay it back over time. These loans can also help boost your credit score as the payments are reported to the credit bureaus.

Why Use a Credit Builder Card?

Credit builder cards are an ideal tool for anyone looking to improve their credit score. Whether you’re starting fresh or recovering from past credit mistakes, these cards offer a simple, effective way to demonstrate responsible credit use. They’re particularly useful for:

- Building credit from scratch if you’re new to credit or have little to no credit history.

- Rebuilding your credit score after financial setbacks like missed payments or high debt levels.

- Improving credit for better loans and rates as you move closer to your financial goals.

Things to Keep in Mind with Credit Builder Cards

While credit builder cards can be a great way to improve your credit score, they do come with some drawbacks:

- High APRs: Credit builder cards typically come with higher interest rates, which means that if you don’t pay off your balance in full, you could face significant interest charges.

- Low credit limits: These cards usually come with low credit limits, which can be limiting in terms of purchasing power.

- Fees: Some cards come with annual fees or other hidden costs, so always read the terms and conditions carefully.

Final Thoughts: The Path to Better Credit Starts with Responsible Use

Credit builder cards are an excellent way to start building or rebuilding your credit score. By following smart strategies and maintaining responsible habits, such as paying on time, staying within your credit limit, and checking your credit report regularly, you can significantly improve your financial future. These cards are designed to help you take control of your credit, boost your score, and make better financial decisions.

Start today by applying for a credit builder card and commit to using it responsibly. With dedication and patience, you’ll soon see your credit score improve, opening doors to better financial opportunities.

Related Articles

What Is a Good Credit Score? Meaning, Ranges, and How to Reach It Faster