Your credit score isn’t just a number hiding in a banking app. It shapes the interest rates you’re offered, the apartments you qualify for, and how expensive it is to borrow money when life demands it, whether that’s a car, a home, or breathing room on a credit card.

If you’ve ever wondered “Is my score actually good?” or “Why did it drop when I didn’t do anything wrong?”, this article is worth a careful reading. Credit score ranges can feel abstract and frustrating until someone finally explains what they really mean, and what actually moves the needle.

This guide breaks it all down in an easy-to-understand way. You’ll learn what each credit score range means, how lenders see you at each level, and how to improve your score faster without doing anything risky or unrealistic.

What Credit Score Ranges Really Mean (And Why They Matter)

Credit scores in the U.S. generally fall between 300 and 850. The higher the score, the less risky you appear to lenders.

But lenders don’t look at your score as a single number. They see it as a range, and each range tells a story about how you’ve handled money in the past, and how likely you are to repay what you borrow next.

The Five Credit Score Ranges Explained

| Level | Credit score range |

|---|---|

| Excellent credit | 800–850 |

| Very good credit | 740–799 |

| Good credit | 670–739 |

| Fair credit | 580–669 |

| Poor credit | Below 580 |

Excellent Credit (800–850)

This is the top tier. Borrowers in this range have long, steady credit histories and rarely miss payments.

This means you gain access to the lowest available interest rates, face fewer hurdles when applying for mortgages, auto loans, or premium credit cards, and may even qualify for lower insurance premiums in many states. Strong credit also gives you more leverage and flexibility when negotiating loan terms.

Reality check: An 850 score is rare, and chasing perfection isn’t necessary. There’s often little practical difference between an 810 and an 850.

Very Good Credit (740–799)

Getting this score range means you’ve demonstrated consistency and restraint, even if your credit file isn’t flawless. For most people, this range is the sweet spot, having excellent benefits without the pressure of maintaining a “perfect” score.

With a very good credit score, you’re likely to be approved for most loans, qualify for competitive interest rates that are close to the best available, and receive higher credit limits along with better credit card rewards.

Good Credit (670–739)

Within this range, you’ll generally qualify for many loans and credit cards, receive interest rates that are reasonable but not the lowest available, and have more choices with fewer obstacles compared to subprime borrowers.

This is the most common range for U.S. adults. That said, this is where borrowing quietly gets more expensive. A “good” score can still cost you tens of thousands of dollars more in interest over time compared to a very good or excellent score.

Fair Credit (580–669)

This range signals some bumps in the road, such as late payments, higher balances, or a limited credit history. Borrowers in this category usually face fewer loan options, higher interest rates, and stricter terms, and they may also be required to pay deposits for utilities, rentals, or phone plans. Fair credit is a transition zone, and even small, consistent improvements can make a noticeably bigger impact than many people expect.

Poor Credit (Below 580)

This credit range typically signals serious credit challenges or very limited credit history. As a result, loan approvals are harder to obtain, approved rates tend to be very high, and everyday costs often increase due to rejections or added fees. However, poor credit can be improved by some consistent and positive habits.

FICO vs. VantageScore: Why You Might See Different Numbers

You don’t have just one credit score. There are multiple scoring models, but the two most common are the FICO Score and VantageScore.

Both use the same 300–850 scale, but they weigh information slightly differently. That’s why you might see a 702 in one app and a 689 in another. The important elements that affect you are the range you’re in and how lenders interpret it.

What Actually Affects Your Credit Score

- Payment history (the biggest factor): Paying bills late or not paying hurts more than almost anything else. Even one missed payment can sting.

- Credit utilization: This is how much of your available credit you’re using. Keeping balances low relative to limits makes a big difference.

- Length of credit history: Older accounts help. This is why closing long-standing cards can backfire.

- Credit mix: A healthy blend of credit cards and installment loans helps slightly.

- New credit applications: Applying for multiple accounts in a short time can temporarily drag your score down.

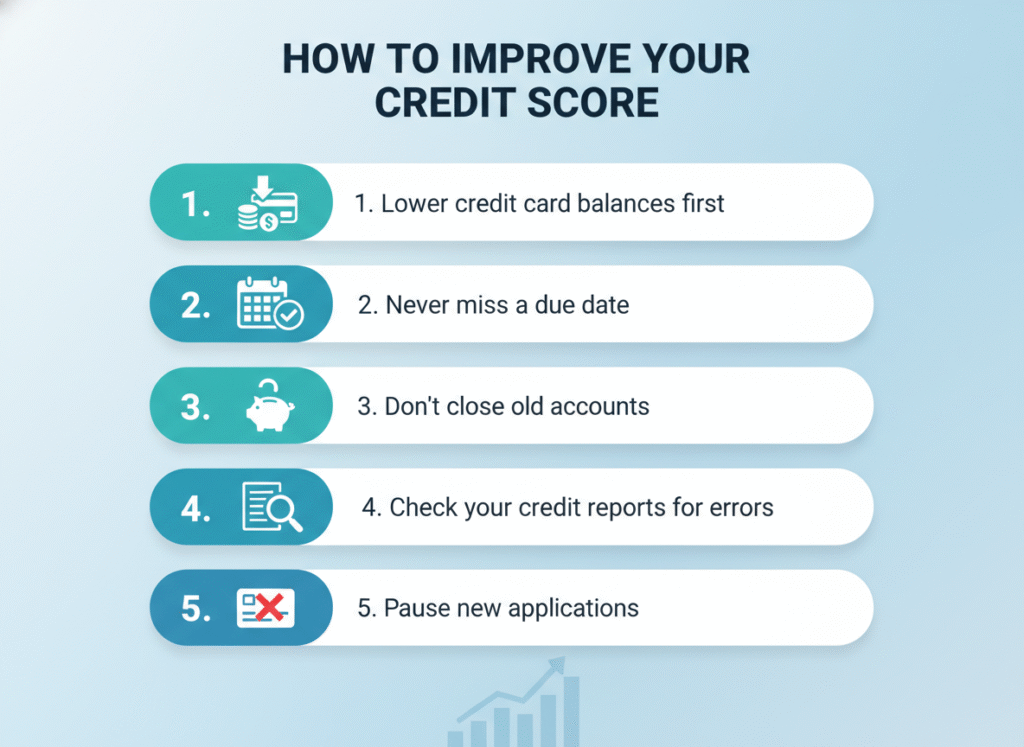

How to Improve Your Credit Score Fast

1. Lower Credit Card Balances First

One of the fastest ways to see movement in your credit score is by paying down revolving balances. Bringing your usage at least below 30% of your available limit signals to lenders that you’re managing credit responsibly rather than relying on it to get by. Even a single payment that drops your balance into a safer range can lead to noticeable score improvements within one or two billing cycles, especially if high utilization was holding you back.

2. Never Miss a Due Date

Payment history carries more weight than any other credit factor, so missing even one due date can undo months of progress. Because of this, you should set up autopay for at least the minimum amount, or use calendar and app reminders to prevent forgetfulness.

3. Don’t Close Old Accounts

Length of credit history plays a meaningful role in your score, so closing older accounts can quietly work against you, even if you’ve paid them off. Keeping long-standing, no-fee cards open helps preserve your average account age and your total available credit. If you aren’t using a card often, an occasional small charge you pay off right away is usually enough to keep it active.

4. Check Your Credit Reports for Errors

Credit reports sometimes have mistakes, and they can drag down your score for no good reason. Some errors such as incorrect balances, outdated accounts, or payments marked late when they weren’t can all hurt you unnecessarily. Taking the time to review your reports and dispute any errors can often result in quick, meaningful score improvements.

5. Pause New Applications

Every new credit application triggers a hard inquiry, which can temporarily lower your score and raise red flags for lenders. Giving your credit profile time to settle can help you qualify for better rates and smoother approvals when it matters most.

How Long Does It Take to See Improvement?

How long it takes to improve your credit depends on where you’re starting, but there are some general patterns. In the first 30–60 days, lowering balances and correcting errors can lead to small gains. Over the next 3–6 months, consistent on-time payments begin to make a noticeable difference. Many people move from fair to good credit within 6–12 months, while rebuilding after major damage typically takes 12–24 months of steady, positive habits.

Credit Scores Are Important, But They Aren’t Your Worth

A low score doesn’t mean you’re irresponsible. It often means you made decisions without good information, or went through something life-changing. Your credit score is a tool, so it gets more useful the better you understand how it works.

If you’re improving from poor to fair, that matters. If you’re climbing from good to very good, that matters too. Each step gives you more freedom, lower costs, and fewer barriers.