When you’re facing financial difficulties or looking to borrow money for an important purchase, it can be easy to fall into the trap of predatory lending. Predatory loans often come with high-interest rates, hidden fees, and unfavorable terms that can leave you struggling to repay them, trapping you in a cycle of debt.

Understanding how predatory loans work and learning how to avoid them is key to protecting your financial health. In this article, we’ll break down the red flags of predatory loans, provide safe borrowing tips, and show you how to make smarter loan choices that protect you and your future.

What Are Predatory Loans?

Predatory loans are financial products offered by lenders that are designed to benefit the lender at the expense of the borrower. These loans often come with high interest rates, hidden fees, and unfair terms that can make them difficult for borrowers to repay. Predatory lending can include payday loans, auto-title loans, subprime mortgages, and certain types of credit cards.

The key feature of a predatory loan is that it’s often marketed as a quick solution to urgent financial problems, but the costs and terms aren’t fully disclosed or explained in a transparent way. This leads to financial instability for the borrower and makes it extremely difficult for them to get out of debt.

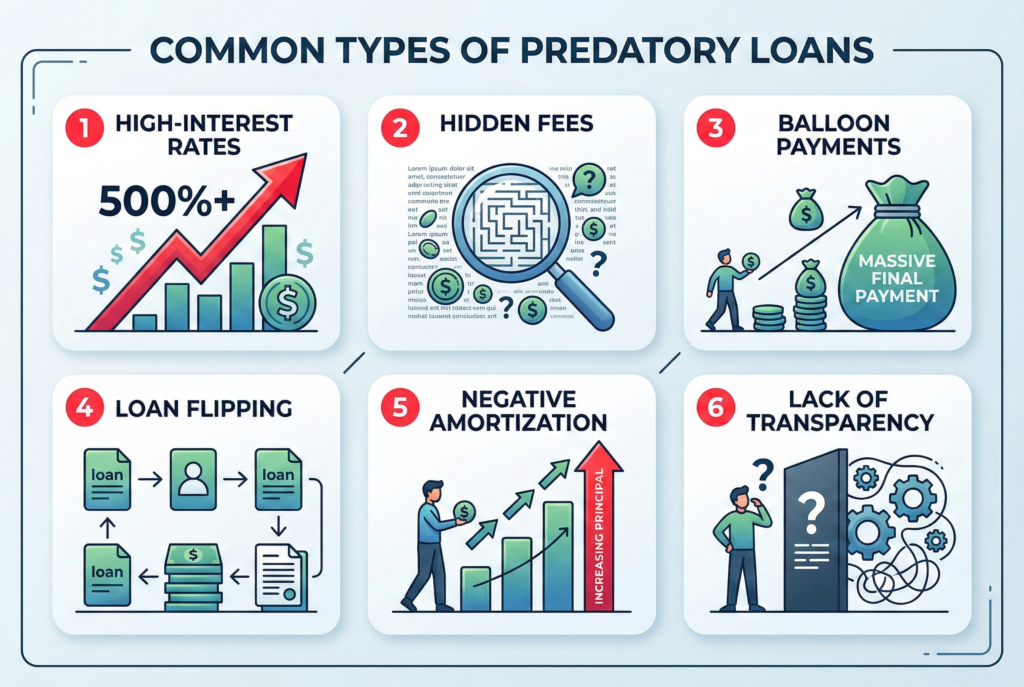

Common Types of Predatory Lending Practices

High-Interest Rates

Predatory lenders often charge exorbitant interest rates far beyond what is considered reasonable. This makes it incredibly difficult for borrowers to repay the loan, especially when the interest compounds quickly.

Hidden Fees

Many predatory lenders hide fees that aren’t clearly disclosed at the start. These might include administrative fees, loan origination fees, or early repayment fees. Such fees can add up quickly, making the loan much more expensive than it initially appears.

Balloon Payments

Some loans come with balloon payments, where a large payment is due at the end of the loan term. This is a significant financial burden for many borrowers, who may not be able to afford the lump sum payment.

Loan Flipping

In this practice, a borrower is encouraged to refinance or “flip” their loan repeatedly, each time with higher fees and increased interest rates. This can lead to a cycle of debt, with no real progress made on paying down the principal.

Negative Amortization

Predatory loans sometimes allow for lower monthly payments, but the unpaid interest is added to the principal, which causes the balance to increase over time. This results in the borrower owing more than when they first took out the loan.

Lack of Transparency

A hallmark of predatory lending is the lack of clear, upfront information. Lenders may not fully disclose the terms of the loan or may use complex language to confuse borrowers, leading them to make decisions they don’t fully understand.

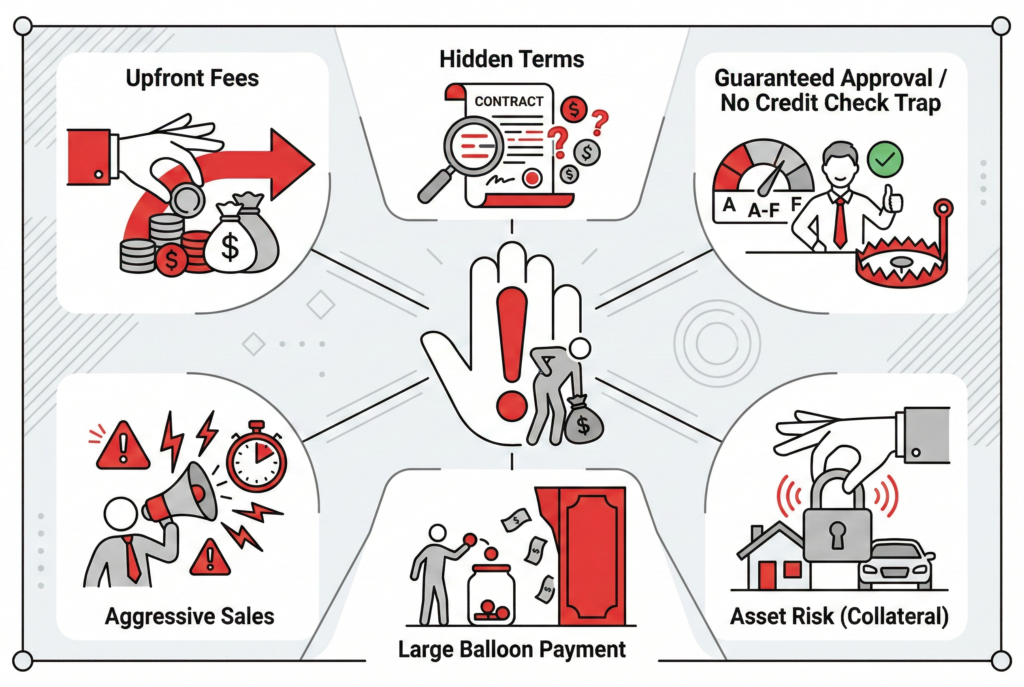

Red Flags to Watch Out For in Predatory Loans

Unreasonably High Fees or Interest Rates

If the fees or interest rates seem disproportionate to the loan amount or are significantly higher than market rates, this is a major warning sign.

Pressure to Act Quickly

Predatory lenders often pressure borrowers into making quick decisions. This could be a sign that they’re trying to prevent you from fully understanding the terms of the loan or from considering other, better options.

Guaranteed Approval

If a lender promises you instant approval, especially without reviewing your financial situation, it’s likely a predatory practice. Reputable lenders will assess your ability to repay the loan before approving it.

Lack of Transparency

If the lender is vague about loan terms, fees, or repayment schedules, or if they’re unwilling to provide clear answers to your questions, it’s a major red flag.

Unclear or Confusing Loan Documents

Always read the fine print before signing anything. If the loan documents are too complex or unclear, it’s likely that important details are being hidden.

Safe Borrowing Tips to Avoid Predatory Lending

Research and Compare Lenders

Before taking out any loan, always shop around and compare loan offers from different lenders. Look for transparent terms, reasonable interest rates, and clear fees. Websites like NerdWallet or Bankrate can help you compare loan options.

Understand the Loan Terms

Make sure you fully understand the interest rate, fees, payment schedule, and total cost of the loan. If anything seems unclear or too complicated, ask the lender for clarification.

Look for Government-Backed Loans

If you’re eligible, consider applying for a government-backed loan like those offered by the FHA or VA. These loans tend to have more favorable terms and protections for borrowers.

Only Borrow What You Need

Avoid taking out more money than necessary. Predatory lenders often try to upsell you on larger loans with higher fees and interest rates. Borrow only what you can afford to repay.

Read Reviews and Check Lender Reputation

Research any lender you’re considering by checking their reviews and ratings. Look for feedback from past borrowers to get an idea of the lender’s reputation and practices. Reputable lenders will have positive reviews and a solid track record.

Check Lender Credentials

Always ensure that the lender is properly licensed and regulated. In the United States, lenders must be licensed by the state in which they operate. You can verify a lender’s credentials through the Consumer Financial Protection Bureau (CFPB) or your state’s department of financial services.

What to Do if You’ve Already Taken Out a Predatory Loan

If you’ve already fallen victim to a predatory loan, there are steps you can take to address the situation:

- Contact the lender: If possible, try to negotiate the loan terms with the lender. Many lenders may be willing to work with you on more reasonable terms if you explain your financial situation.

- Consider debt consolidation: If you have multiple loans or debts, you may want to consider debt consolidation. This can help you combine your debts into one manageable payment with a potentially lower interest rate.

- Seek legal advice: If you feel you’ve been treated unfairly, consult with a consumer protection lawyer or contact your state’s attorney general. You may have legal recourse for predatory lending practices.

Reporting Predatory Lending Practices

If you believe you’ve been a victim of predatory lending, it’s important to take action. File a complaint with the Consumer Financial Protection Bureau (CFPB) or your state’s consumer protection office. You can also report unfair practices to the Federal Trade Commission (FTC). These organizations can investigate the lender, take enforcement actions, and help you understand your rights under the law.

Final Thoughts: Protect Yourself and Make Smarter Financial Choices

While predatory lending is a serious problem, there are steps you can take to protect yourself. By being aware of red flags, doing thorough research, and ensuring that any loan you take on has fair terms, you can avoid falling into a debt trap.

Financial literacy and prudent borrowing habits are your best defense. Armed with the knowledge of how predatory loans work, you can make more informed, smarter financial decisions and keep your finances on track.