When it comes to planning for your child’s future, saving money in an efficient and flexible way is crucial. One of the most effective tools for saving for children is the UGMA account (Uniform Gifts to Minors Act). This account allows you to transfer assets to a minor in a way that helps build their financial foundation while offering tax advantages. If you’re wondering how UGMA accounts work, what the benefits are, and how they can fit into your long-term financial strategy, you’ve come to the right place.

In this article, we’ll explore how UGMA accounts function, compare them to other savings options, and provide detailed advice on setting one up. Let’s dive into how UGMA accounts can help you build wealth for your child’s future.

What Is an UGMA Account?

An UGMA account is a type of custodial account designed to hold assets for a minor until they reach the age of majority, which is usually 18 or 21 depending on the state. The assets are held in the minor’s name, but managed by a custodian (typically a parent or guardian) until the minor reaches adulthood.

The key feature of an UGMA account is that it allows adults to transfer ownership of financial assets, such as cash, stocks, bonds, and mutual funds, to a child without needing to create a trust. The custodian manages the account on the child’s behalf, but once the child reaches adulthood, the custodian’s control over the account ends, and the child can use the funds however they choose.

Unlike other savings accounts like the 529 Plan (which is limited to educational expenses), UGMA accounts can be used for any purpose, such as purchasing a car, paying for college, or even starting a business. This flexibility is one of the biggest advantages of UGMA accounts.

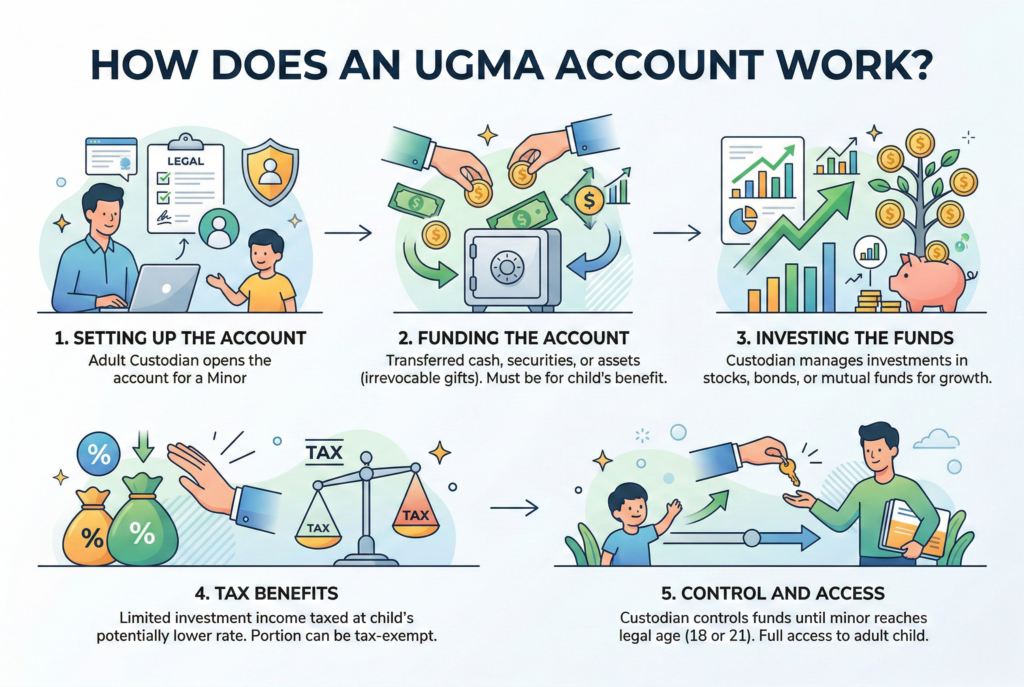

How Does an UGMA Account Work?

Setting Up the Account

To open an UGMA account, you must choose a custodian (typically a parent, but can also be a grandparent or another adult) and a financial institution (such as a bank or brokerage firm). The custodian manages the account until the child reaches adulthood.

Funding the Account

There are no annual contribution limits for an UGMA account, so you can contribute as much as you wish. However, contributions above a certain threshold may be subject to gift tax. The funds can include cash, stocks, bonds, mutual funds, and other types of investments.

Investing the Funds

The custodian can invest the funds in various investment vehicles, including stocks, bonds, and mutual funds, based on the child’s financial needs and the investment goals. The goal is typically to grow the funds over time so that they can be used by the child when they reach adulthood.

Tax Benefits

One of the key advantages of an UGMA account is its tax treatment. The income from the account is taxed at the child’s tax rate, which is usually lower than the parent’s rate. However, if the child’s income exceeds a certain threshold, the kiddie tax may apply, and the income will be taxed at the parent’s rate.

Control and Access

The custodian manages the account until the child reaches the age of majority (usually 18 or 21, depending on state law). After that, the child gains full control of the account and can use the funds for any purpose, such as buying a car or paying for college.

Benefits of UGMA Accounts

Flexibility in Usage

Unlike 529 plans that are specifically designed for education, UGMA accounts offer more flexibility. Once the child reaches adulthood, they can use the money for any purpose, whether that’s starting a business, buying a car, or even investing for the future.

No Contribution Limits

UGMA accounts don’t have annual contribution limits, unlike other savings vehicles like IRAs or 529 plans. This makes them ideal for families looking to contribute large amounts toward a child’s financial future.

Potential for Investment Growth

Since UGMA accounts allow for a variety of investment options, such as stocks and bonds, they have the potential for greater growth compared to traditional savings accounts or CDs.

Tax Advantages

The income generated by the assets in the UGMA account is typically taxed at the child’s rate, which is often much lower than the parent’s tax rate. However, the kiddie tax can apply if the child’s income exceeds a certain threshold, and in that case, the income is taxed at the parent’s rate.

Drawbacks of UGMA Accounts

Control Over Funds

Once the child reaches the age of majority, they gain full control of the account and can use the funds for any purpose. This means they could potentially use the money for non-essential items or decisions that don’t align with the original intent (such as funding college expenses).

Impact on Financial Aid

Since the funds in the UGMA account belong to the child, they’re considered the child’s assets for financial aid purposes. This could reduce the amount of financial aid the child qualifies for when applying to college.

Kiddie Tax

While UGMA accounts can offer tax advantages, the kiddie tax could apply if the child’s investment income exceeds a certain threshold, meaning that the income is taxed at the parent’s tax rate, which could result in higher taxes.

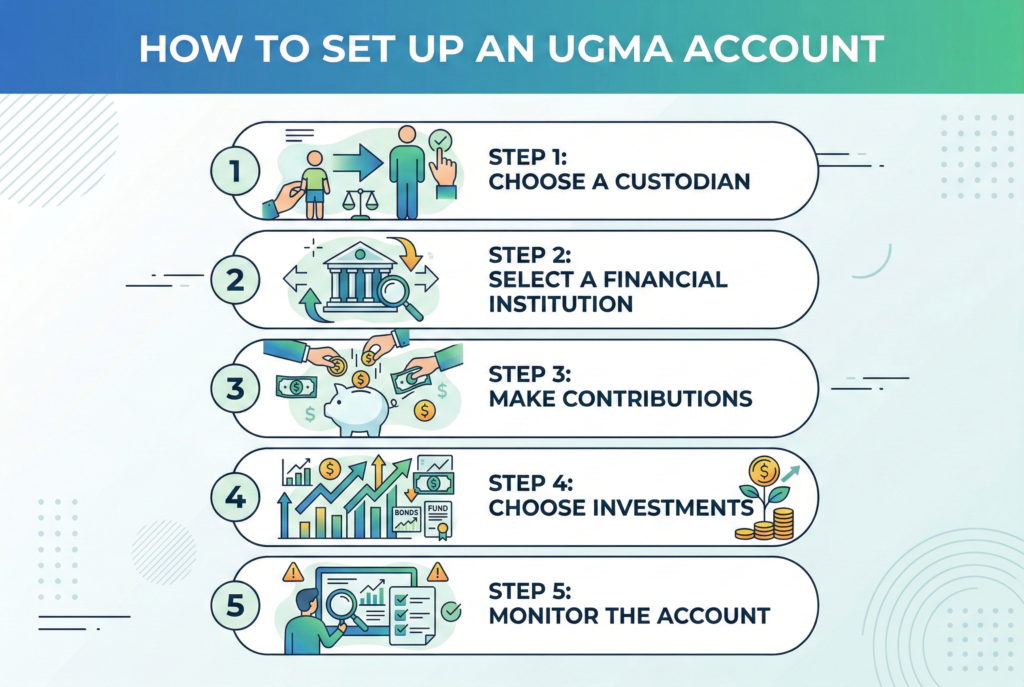

How to Set Up an UGMA Account

Choose a Custodian

The custodian is typically a parent or guardian, but it can also be a grandparent or another adult. The custodian is responsible for managing the account until the child reaches the age of majority.

Select a Financial Institution

UGMA accounts can be set up through banks, credit unions, or brokerage firms. Research different institutions to find one that offers the best investment options and fees.

Make Contributions

Anyone can contribute to the UGMA account, including family members and friends. However, the contributions are considered gifts and may be subject to gift tax if they exceed certain limits.

Choose Investments

The custodian will select the investments for the UGMA account based on the child’s age and long-term financial goals. It’s important to review the account periodically and adjust investments as needed.

Monitor the Account

Once the UGMA account is set up, it’s important to regularly review the account’s performance, ensure that the investments are performing well, and make adjustments as necessary.

UGMA Accounts vs. Other Savings Accounts

UGMA vs. UTMA

The primary difference between UGMA and UTMA accounts is the types of assets they can hold. While UGMA accounts are limited to financial assets like cash, stocks, and bonds, UTMA accounts can hold a wider range of assets, including real estate, art, and even intellectual property.

UGMA vs. 529 Plans

UGMA accounts offer more flexibility than 529 plans, which are designed solely for education savings. However, 529 plans provide tax-free growth when used for educational expenses, which can be a significant advantage for families saving specifically for college.

Final Thoughts: Why UGMA Accounts Are a Great Option for Saving for Your Child’s Future

An UGMA account is a powerful tool for parents and guardians who want to save for a child’s future with flexibility, tax advantages, and the potential for growth. Whether you’re saving for college, a first car, or a down payment on a home, the UGMA account offers a versatile and tax-efficient solution.

By understanding how UGMA accounts work and the benefits and drawbacks, you can make a well-informed decision about whether this savings vehicle is right for your child’s financial future. Start planning today and take advantage of the many benefits UGMA accounts offer to secure a brighter tomorrow for your child.