When you’re facing multiple debts, deciding how to tackle them can be overwhelming. Whether it’s credit card debt, personal loans, or student loans, it’s easy to feel like you’ll never get ahead. But the debt avalanche method offers a clear and strategic way to pay down debt faster while saving money on interest.

In this article, we’ll explain how the debt avalanche method works, why it’s a great strategy for saving on interest, and how to implement it effectively. We’ll also compare it to the debt snowball method and discuss the emotional challenges you might face while paying off debt. By the end of this guide, you’ll have the tools to start tackling your debt with a proven strategy that works.

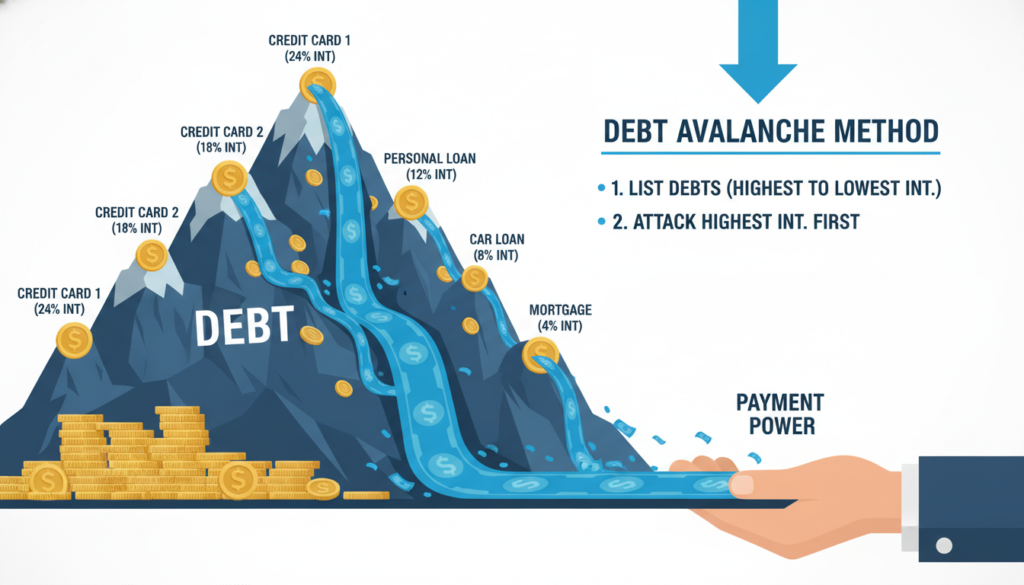

What is the Debt Avalanche Method?

The debt avalanche method is a debt repayment strategy that prioritizes paying off your debts with the highest interest rates first. The logic behind this approach is simple: by targeting the most expensive debt first, you minimize the amount of interest you pay over time, ultimately saving you money and reducing the time it takes to pay off all your debts.

The idea is to make the minimum payments on all of your debts except the one with the highest interest rate. For the highest-interest debt, you’ll make extra payments to pay it off as quickly as possible. Once that debt is paid off, you move on to the next highest-interest debt, and so on, until all your debts are cleared.

This method is particularly effective when dealing with high-interest credit cards and other types of high-interest loans, as it minimizes the impact of interest accumulation.

How Does the Debt Avalanche Method Work?

The debt avalanche method is built around prioritization and interest management.

List All Your Debts

Start by listing all of your debts, including the balances and the interest rates for each. This gives you a clear picture of what you’re dealing with and helps you prioritize which debts to pay off first.

Pay the Minimum on All Debts

Make the minimum payments on every debt, ensuring you stay in good standing with all your creditors. Avoid missing any payments, as this can lead to late fees and additional interest.

Target the Highest-Interest Debt

Focus any extra money you can put toward the debt with the highest interest rate. For example, if you have a credit card with a 25% interest rate, and a personal loan with a 5% interest rate, pay off the credit card first.

Repeat the Process

Once the highest-interest debt is paid off, take the amount you were paying toward that debt and apply it to the next highest-interest debt. Continue this process until all your debts are cleared.

Stay Consistent

While it may take time to see progress, consistency is key. Even though you might not see immediate results like the debt snowball method (where you pay off smaller debts first), the debt avalanche method saves you more money in the long run.

Pros of the Debt Avalanche Method

Saves More Money on Interest

By focusing on high-interest debt first, you pay less in interest over time, helping you clear your debt faster and with fewer costs.

Faster Debt Repayment

Since you’re tackling the highest-interest debts first, you can reduce your total debt load more quickly, which gives you more freedom to save and invest.

Financial Discipline

This method encourages a structured, disciplined approach to debt repayment, which can lead to long-term financial success.

Cons of the Debt Avalanche Method

Slow Progress Initially

The downside is that the method can feel slow at first. Since you’re prioritizing high-interest debts, the smaller debts may take longer to pay off, which can feel discouraging.

Psychological Challenges

Some people may find it demotivating to see high-interest debts sitting around while they’re focusing on bigger balances. If you’re someone who needs quick wins to stay motivated, this method can be harder to stick with.

Requires Extra Discipline

Staying disciplined and sticking to the plan is crucial, especially if you face any unexpected expenses. The longer the process takes, the harder it can be to stay committed.

Debt Avalanche vs Debt Snowball: Which One Is Right for You?

Both the debt avalanche method and the debt snowball method are popular strategies for paying off debt. The debt snowball method involves paying off your smallest debts first, which provides quick wins and boosts motivation. However, while it offers psychological benefits, it’s less efficient in terms of interest savings compared to the debt avalanche method, which focuses on high-interest debts first.

Debt avalanche is best suited for individuals who are motivated by saving money and who are comfortable with longer-term payoff periods. Debt snowball may be a better fit for those who need immediate progress and psychological encouragement to keep going.

It’s essential to choose the method that aligns with your financial goals and emotional needs. If you need fast wins, go with the snowball. If you’re focused on minimizing interest and accelerating long-term repayment, the avalanche method is your best bet.

A Practical Example of the Debt Avalanche Method

Let’s look at an example to illustrate how the debt avalanche method works:

Imagine you have the following debts:

- Credit Card 1: $3,000 balance, 20% interest rate

- Credit Card 2: $5,000 balance, 15% interest rate

- Personal Loan: $4,000 balance, 10% interest rate

Here’s how you would apply the debt avalanche method:

- Step 1: Start by paying the minimum payments on Credit Card 2 and the Personal Loan.

- Step 2: Use any extra funds you have to pay off Credit Card 1 first, as it has the highest interest rate.

- Step 3: Once Credit Card 1 is paid off, take the money you were putting toward that card and apply it to Credit Card 2, which now becomes your highest-interest debt.

- Step 4: Once Credit Card 2 is paid off, move on to the Personal Loan.

By using this method, you save money on interest by tackling the highest-interest debt first. Over time, you’ll make faster progress toward becoming debt-free.

Tips for Staying Motivated with the Debt Avalanche Method

Track Your Progress

Celebrate milestones along the way, such as paying off each high-interest debt. Tracking your success visually (using charts or apps) can help you stay focused.

Set Small Rewards

While the process might take time, reward yourself when you achieve significant milestones, like paying off a debt or reaching a certain percentage of your goal.

Stay Disciplined

Even when it feels like you aren’t making much headway, remember that the longer you stick with the plan, the more money you save on interest in the long run. Patience pays off.

Final Thoughts: Is the Debt Avalanche Method Right for You?

The debt avalanche method is an effective strategy for anyone looking to pay off high-interest debt as quickly as possible while saving money on interest. By focusing on the debts with the highest interest rates, you can reduce your overall debt load faster and more efficiently than with other strategies.

If you’re disciplined and patient, the debt avalanche method could be a perfect fit for your debt repayment plan. If you need smaller victories to stay motivated, however, the debt snowball method might be a better option. Ultimately, your approach to debt repayment should match your goals, personality, and financial situation.

Related Articles

Debt Management Programs Explained: How They Work and When They’re the Smartest Debt Solution