Understanding how much money you have at your disposal is essential for effective budgeting and long-term financial planning. Two terms that are often confused but are crucial in managing personal finances are disposable income and discretionary income. These two types of income may sound similar, but they serve different purposes and are calculated differently.

In this article, we’ll break down the meaning of disposable income and discretionary income, explain how to calculate both, and provide clear steps to help you improve your financial situation. By understanding the key differences between these two, you’ll be able to better manage your spending, save for future goals, and make more informed financial decisions.

What is Disposable Income?

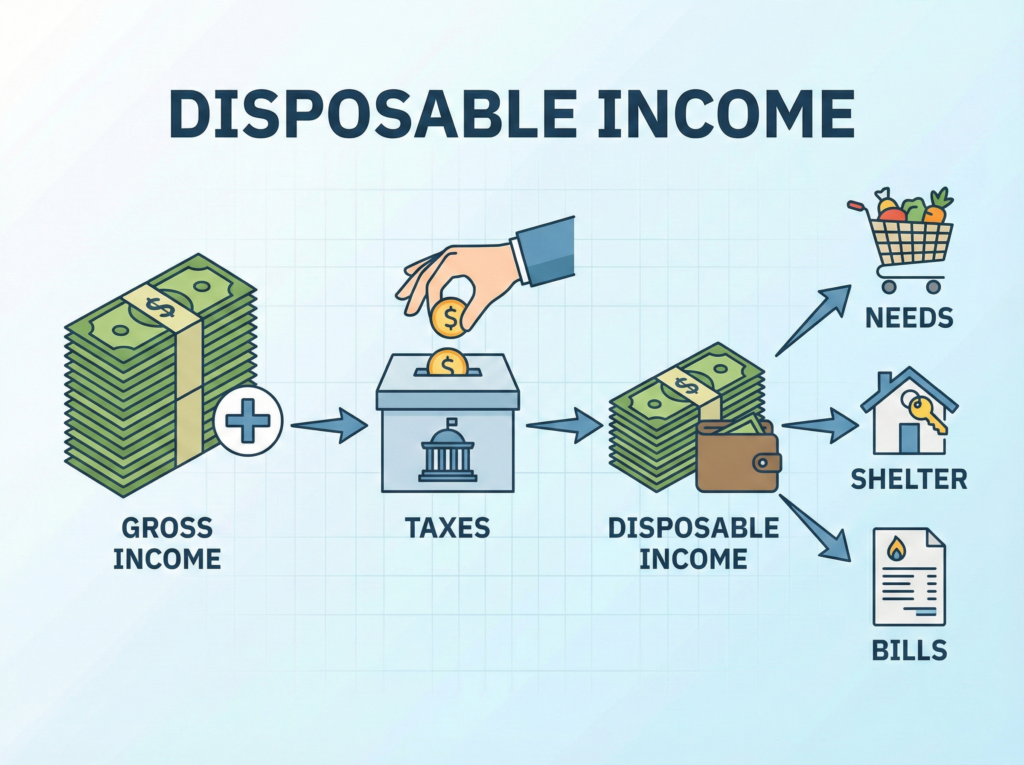

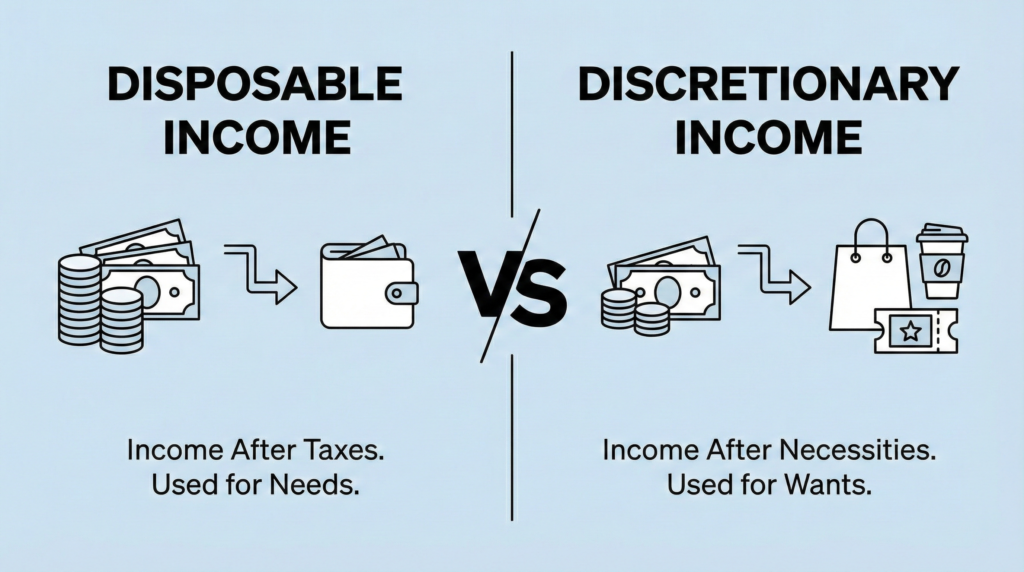

Disposable income refers to the money you have left after paying taxes. It’s the income available to you for spending, saving, or investing. Essentially, disposable income is what remains from your paycheck after all mandatory deductions, including federal, state, and local taxes, as well as any retirement contributions or other deductions.

What is Discretionary Income?

Discretionary income is the portion of your disposable income that remains after you have paid for essential expenses. These expenses typically include housing costs, groceries, utilities, and transportation. Discretionary income, therefore, is the money available for non-essential spending: things like entertainment, dining out, vacations, or investments.

Key Differences Between Disposable and Discretionary Income

While disposable income and discretionary income are closely related, the key difference lies in their definition and usage. Disposable income is the income left after taxes are deducted from your earnings. It’s the money you can spend on both essential needs (like rent, utilities, and groceries) and non-essentials (like vacations, dining out, or entertainment). In short, disposable income represents the total funds available to meet your basic living expenses and some optional spending.

On the other hand, discretionary income is more specific: it’s the money remaining after covering your essential expenses. This is the portion of your income that you can use for things that aren’t strictly necessary but enhance your lifestyle, such as traveling, entertainment, savings, or even investing in assets that build long-term wealth. Discretionary income is often viewed as a buffer that helps people maintain their quality of life while working toward their financial goals.

How to Calculate Disposable Income

Calculating your disposable income is straightforward. Here’s how to do it:

- Start with your gross income: This is the amount of money you earn before taxes.

- Subtract taxes: Deduct federal, state, and other taxes from your gross income. If you’re an employee, this is usually done for you, and you’ll see your after-tax income on your paycheck.

Example:

- Gross income: $4,000

- Taxes: $800

- Disposable income = $4,000 – $800 = $3,200

Your disposable income is now the amount you have to cover both essential and non-essential expenses.

How to Calculate Discretionary Income

Now that you have your disposable income, you can calculate your discretionary income by subtracting your essential expenses. Essential expenses typically include things like housing (rent or mortgage), utilities (electricity, water, or gas), groceries, transportation (car payment, insurance, gas, or public transport), and health Insurance or other necessary expenses.

Example:

- Disposable income = $3,200

- Essential expenses = $2,500

- Discretionary income = $3,200 – $2,500 = $700

This $700 is the amount available to spend on non-essentials, saving, or investing.

Why Both Disposable and Discretionary Income Matter for Your Financial Health

Both disposable income and discretionary income play critical roles in your financial health. Understanding and managing these two types of income are crucial steps in budgeting and achieving your financial goals.

Your disposable income gives you a clear picture of how much money you have after taxes to cover all of your necessary expenses. This allows you to plan for your basic needs and see where you can free up funds for other financial priorities, such as savings or debt repayment.

On the other hand, your discretionary income is important because it shows you the financial flexibility you have to achieve your goals. This is the portion of your income that can be used for investments, long-term wealth building, or even short-term luxuries like dining out or entertainment. Managing your discretionary income wisely is key to maintaining a balanced financial life, ensuring that you enjoy life’s pleasures while also securing your future.

Tips for Managing Disposable and Discretionary Income Effectively

Track Your Expenses

The first step is to keep track of your expenses: both necessary and discretionary. Use a budgeting app or create a spreadsheet to monitor where your money is going and adjust your spending habits accordingly.

Prioritize Savings

Once you know your discretionary income, prioritize putting a portion of it into savings and investments. Aim to save at least 20% of your discretionary income for your emergency fund, retirement, or future goals.

Limit Non-Essential Spending

Look for areas where you can reduce unnecessary spending. Cutting back on dining out, subscriptions, or impulse purchases can free up more of your discretionary income for savings or investments.

Set Financial Goals

Use your discretionary income to work towards specific financial goals. Whether it’s saving for a down payment on a home, contributing to your retirement fund, or paying off high-interest debt, having clear goals will keep you motivated and focused.

Final Thoughts: Master Your Disposable and Discretionary Income for Financial Success

Understanding the difference between disposable income and discretionary income is crucial for managing your finances effectively. By calculating these figures and making conscious decisions about how to allocate your money, you can improve your financial health, reduce stress, and reach your long-term goals.

With careful budgeting, smart savings, and a clear financial plan, you can make the most of your disposable income and discretionary income. The more you focus on your financial goals, the more control you’ll have over your spending and wealth-building efforts.