Life has a habit of showing up unannounced. One minute everything’s fine. Next, your car won’t start, your kid wakes up sick, or your job suddenly feels less “secure” than it did last week. These moments don’t wait for payday, bonuses, or a convenient time to adjust your budget.

That’s exactly why an emergency fund matters.

Not as a vague financial “nice-to-have,” but as a practical buffer that keeps everyday surprises from turning into long-term money stress. Let’s break down what it is, how much you actually need, and how to build it faster than you think, without extreme budgeting or unrealistic advice.

What an Emergency Fund Really Is (and What It Isn’t)

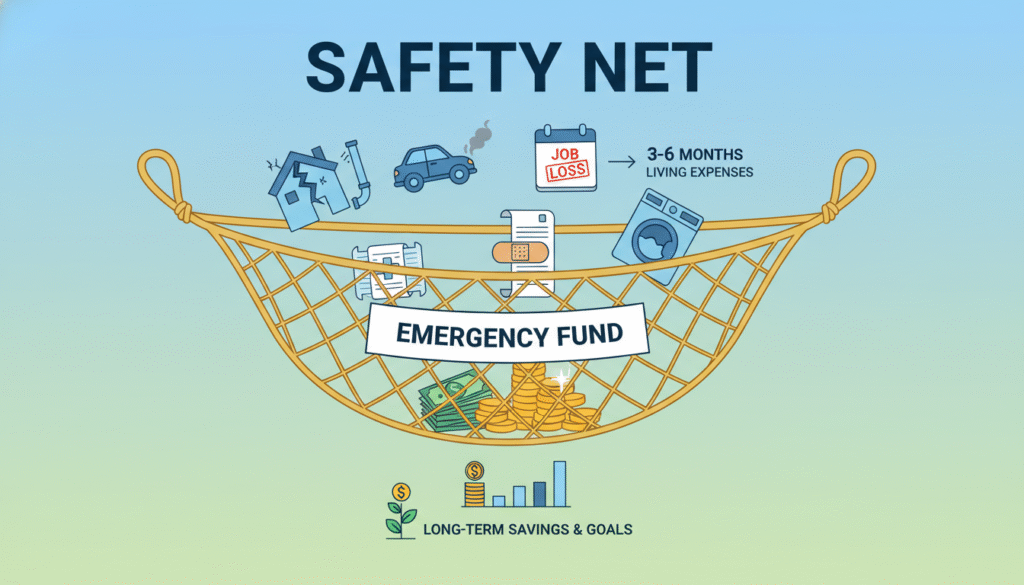

An emergency fund is cash set aside specifically for the unexpected, like the stuff you didn’t plan for and couldn’t reasonably predict. For example, a car repair you need to get to work, a medical bill insurance didn’t fully cover, a sudden drop in income, or even an urgent home repair. It isn’t for vacations, holiday gifts, or expenses you know are coming. Those belong in separate savings buckets.

At its core, an emergency fund does one powerful thing: It gives you options when life gets messy.

Why an Emergency Fund Changes Everything

Without emergency savings, even small problems can spiral quickly. A $900 repair becomes credit card debt. Missed work turns into late fees. Stress piles on top of stress. With an emergency fund, you can avoid high-interest debt. It also keeps your other financial goals intact and helps you make calmer, smarter decisions. And honestly, you sleep better. For renters, having an emergency fund provides them with flexibility. For homeowners, it’s protection. For families, it’s breathing room.

How Much Emergency Fund Do You Really Need?

Start with a Starter Emergency Fund

If you’re starting from zero, don’t aim for perfection. Aim for momentum. A strong first milestone: $500 to $1,000 in cash. This alone can cover most everyday emergencies and keep you from reaching for a credit card.

Build Toward a Fully Funded Emergency Fund

Three months of expenses may be enough if:

You have a stable, salaried job.

Your household has two incomes.

Your expenses are predictable.

Six months (or more) makes sense if:

You’re self-employed or freelance.

You’re a single-income household.

Your job is commission-based or seasonal.

You support dependents.

Once you have a base, the longer-term target depends on your life. The key word here is expenses, not income. Focus on what it actually costs to keep your life running, such as housing, food, utilities, insurance, and transportation.

Where to Keep Your Emergency Fund

Your emergency fund has one job: to be there when you need it. That means it should be easy to access, carry no risk of loss, and come with no penalties. Good options that meet those requirements include high-yield savings accounts and money market accounts that allow quick, simple transfers.

Because an emergency fund is insurance money, you should avoid investing it in stocks, which can lose value when you need the money most, locking it into CDs with early-withdrawal penalties, and mixing it into your everyday checking account, where it’s more likely to be spent unintentionally.

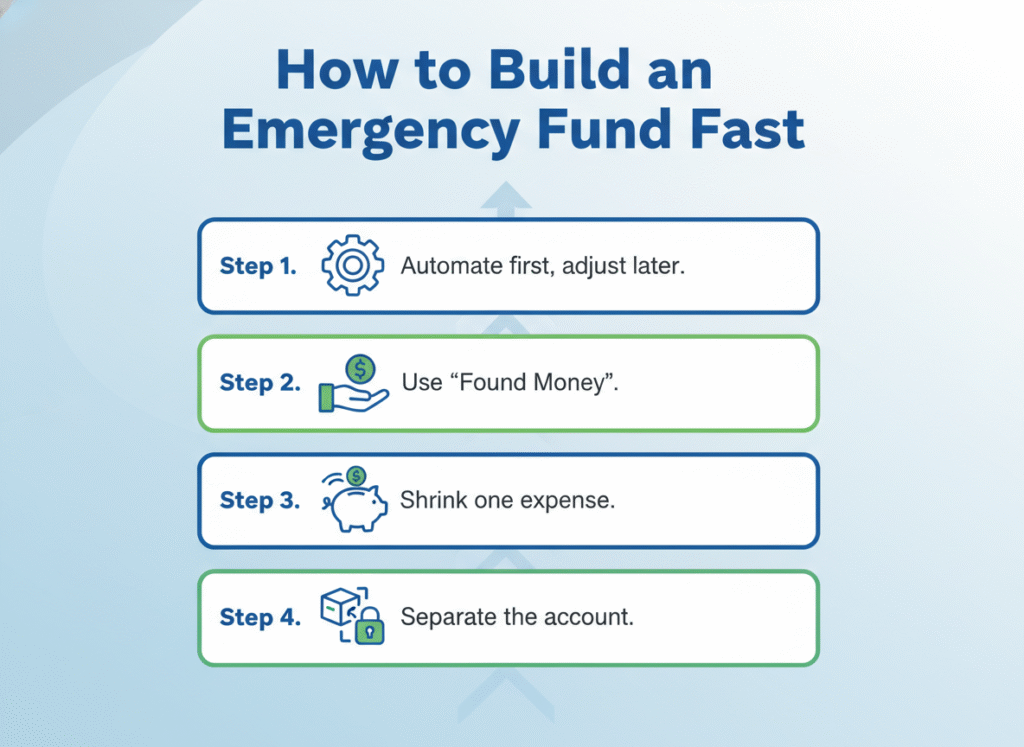

How to Build an Emergency Fund Fast

Step 1. Automate First, Adjust Later

Set up an automatic transfer right after payday, even if it’s small because consistency beats intensity every time.

Step 2. Use “Found Money” Strategically

Try saving half (or even all) of these powerful accelerators: tax refunds, bonuses, side hustle income, and cash gifts to move you forward quickly.

Step 3. Shrink One Expense Temporarily

This is about making one intentional change for a short window of time. Pick a single adjustment for 60–90 days, such as eating fewer takeout meals, pausing a subscription, or delaying a discretionary upgrade. That small, temporary discomfort can create breathing room in your budget and lead to long-term financial stability without feeling overwhelming.

Step 4. Separate the Account

When your emergency fund lives somewhere else, you’re less tempted to treat it like spending money.

What Counts as a Real Emergency?

Here’s a simple rule of thumb: a true emergency is unexpected, necessary, and urgent. Before using your emergency fund, ask yourself whether you could have planned for the expense, if it can wait without serious consequences, and whether it threatens your ability to work, live, or stay safe. If your answers point to “yes, this is serious,” then that’s exactly what your emergency fund is for.

Common Mistakes That Slow People Down

Even motivated savers can get tripped up by trying to save too much, too fast, feeling discouraged by big numbers, dipping into emergency savings for convenience, or waiting for the “perfect” time to start. Remember, progress doesn’t come from doing everything right, it comes from showing up consistently.

Emergency Fund vs. Other Financial Goals

You might also be paying off debt, saving for a home, or investing for retirement. An emergency fund doesn’t compete with these goals, it protects them. Without it, one unexpected expense can undo months, or even years, of progress elsewhere.

The Bottom Line

An emergency fund isn’t about fear. It’s about freedom.

Freedom to handle surprises without panic. Freedom to say no to bad financial choices. And freedom to move through life with a little more confidence. So if you don’t have one yet, start small and start this week.