If you’ve ever looked at your bank balance and wondered where your money goes, it means you’re dealing with expenses that don’t show up neatly every month. Expenses like car repairs, holiday gifts, vet bills, property taxes, or even urgent appliance replacements don’t always arrive on a monthly schedule.

This is exactly when you need sinking funds, as a calm, practical way to stay ahead of life instead of reacting to it. This guide explains what sinking funds are and how you can start building them.

What Is a Sinking Fund?

A sinking fund is money you intentionally set aside, little by little, for a specific future expense you already know is coming. It isn’t an emergency, vague savings, or an “I’ll deal with it later” situation. Honestly, it’s saving on purpose.

Think of it this way: Instead of letting a big expense crash into your budget all at once, you gently lower it into your monthly life ahead of time. If you can name it and roughly predict it, it probably belongs in a sinking fund. For example, annual insurance premiums, holiday gifts, car maintenance, vacations, or property taxes.

Why Sinking Funds Exist (And Why They Work So Well)

Most budgets fail in the same quiet way: They only plan for monthly expenses. However, life doesn’t bill you monthly, so sinking funds exist to solve that mismatch. They break large, stressful expenses into manageable monthly amounts, reduce reliance on credit cards or “we’ll figure it out later” spending, and create clarity so you always know what your money is for. Just as importantly, they remove guilt when it’s time to spend.

Sinking Funds vs. Savings vs. Emergency Funds

| Sinking funds | Savings | Emergency funds | |

|---|---|---|---|

| Purpose | Planned, known expenses | Where money lives | Unexpected, urgent problems |

| Timeline | Future, predictable | Neutral | Unknown |

| Example | $1,200 holiday spending, saved over 12 months | The container that holds sinking funds | Job loss, medical emergency, major surprise repair |

Common Types of Sinking Funds

Annual Fixed Expenses

They include insurance premiums, property taxes, and professional fees, which are the easiest costs to plan for because the amounts are typically predictable and known well in advance.

Irregular but Predictable Expenses

They’re costs you can estimate based on past spending and adjust over time as needed. Common examples include car maintenance, home repairs, and medical deductibles.

Lifestyle & Events

These expenses are optional, but planning for them makes a huge difference. Vacations, weddings, holidays, and birthdays are meant to be enjoyable moments, not financial stress points.

Replacement Funds

Appliances, phones and laptops, and furniture all wear out eventually. When you plan ahead with a sinking fund, these replacements stop being surprises. Instead of scrambling when something breaks or slows down, you already have the money set aside and can replace it on your own terms.

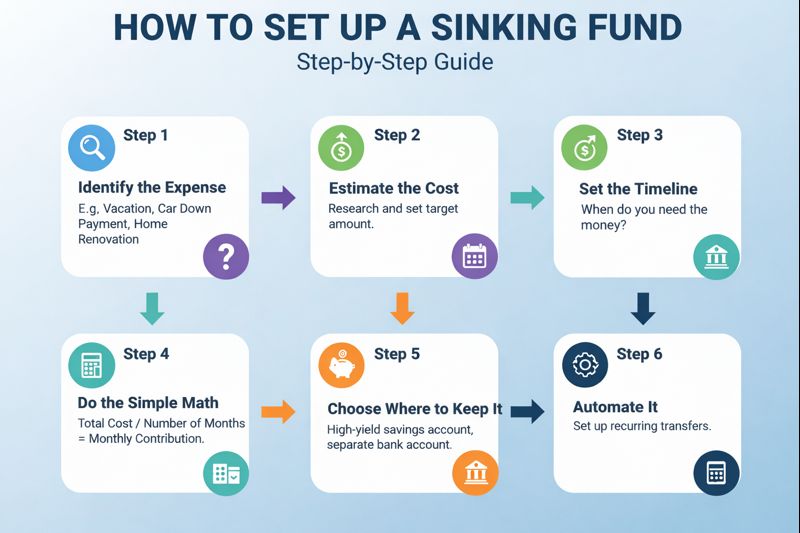

How to Set Up a Sinking Fund (Step by Step)

Step 1: Identify the Expense

The first step is simply identifying the expense you want to plan for. Think about the costs that seem to catch you off guard every year, even though they aren’t true surprises. Ask yourself what you already know you’ll need to pay for. If an expense makes you think, “I should have planned for this,” it probably belongs in a sinking fund. Write these expenses down so they move from vague worries to concrete plans you can actually manage.

Step 2: Estimate the Cost

Once you know what you’re saving for, take a few minutes to estimate the cost. Look at past bills, receipts, or bank statements, or do a quick online search to see what the expense typically runs. Prices change, fees pop up, and life has a way of being slightly more expensive than expected, so just aim for reasonable costs.

Step 3: Set the Timeline

Next, decide on your timeline. Ask yourself when you’ll realistically need the money, maybe in six months, a year, or two years down the road. The timeline matters because it determines how much you need to set aside each month. A longer runway means smaller, easier contributions, while a shorter timeline requires a bit more focus. Either way, choosing a clear deadline turns a vague goal into a manageable plan.

Step 4: Do the Simple Math

Now it’s time for the easiest part: the math. Take the total cost of the expense and divide it by the number of months you have to save. That number becomes your monthly sinking fund contribution.

Step 5: Choose Where to Keep It

Common ways to keep sinking funds include using a high-yield savings account, setting up separate sub-accounts, or using budgeting apps that digitally label money for specific purposes. The best option is the one that keeps the money visible but hard to accidentally spend.

Step 6: Automate It

Finally, automate the process. Automation is what turns good intentions into actual habits. By setting your sinking fund transfers to happen right after payday, the money moves before you have a chance to spend it elsewhere.

Mistakes That Make Sinking Funds Fail

Sinking funds are simple, but they aren’t immune to human behavior. The most common mistakes come from underestimating costs by forgetting taxes, fees, or inflation, dipping into the fund for unrelated spending, skipping contributions “just this month,” or creating too many sinking funds at once. Starting small, staying consistent, and expanding gradually makes the system far more sustainable and effective over time.

How Many Sinking Funds Should You Have?

You can have as many sinking funds as your budget can realistically support, but usually fewer than you might want. When you spread your money too thin, none of the funds grow fast enough to feel meaningful. A better approach is to start with two or three high-impact sinking funds, focus on what’s most urgent or important, and add more as your cash flow improves.

Why Sinking Funds Reduce Financial Stress

Sinking funds not only help your bank account but also your nervous system. Instead of feeling behind, you know what your money is doing, which future expenses are already covered, and that spending, when it’s planned, doesn’t equal failure.

A Real-Life Example: How Sinking Funds Actually Work

Meet Sarah and Mark, a couple in their mid-30s with two kids, a mortgage, and busy jobs. On paper, they’re doing fine. Decent income. No major financial disasters. But every year, the same thing keeps happening.

December hits, and suddenly holiday gifts blow past their budget, one car needs repairs, property taxes are due, and a credit card balance quietly creeps up.

Before Sinking Funds

Sarah and Mark used a basic monthly budget. But anything that didn’t happen every month felt like a surprise, even though it wasn’t.

So when $1,800 in holiday spending showed up, $1,200 in car repairs popped up, or $2,400 in annual insurance premiums came due, they reached for credit cards and told themselves they’d “pay it off soon.” They usually did, but each time it added unnecessary stress, interest charges, and a lingering sense of guilt that made those predictable expenses feel heavier than they needed to be.

After They Started Using Sinking Funds

Instead of changing their entire financial life, they made one shift. They set up three sinking funds: a Holiday Fund with $150 set aside each month, a Car Maintenance Fund at $100 per month, and an Insurance Fund funded with $200 per month. That’s $450 per month total, money they were already spending anyway. Then they automated transfers into a high-yield savings account and treated those transfers like bills.

What Changed

By the end of the year:

- Holiday spending was fully covered without using credit cards.

- Car repairs were annoying, but not stressful.

- Insurance premiums were paid in full, on time.

- Their emergency fund stayed untouched.

- The “Where did the money go?” conversations disappeared.

They stopped dreading certain months of the year. Spending no longer came with regret because it had already been planned. And for the first time, their budget matched how life actually works.

The Bottom Line

If you’re tired of being surprised by expenses you knew were coming, a sinking fund is the missing piece. Sinking funds won’t make you rich overnight. But they’ll smooth out your cash flow, keep you out of unnecessary debt, turn “uh-oh” expenses into non-events, and give you confidence with money.