Student loans have a way of following you into every stage of adulthood. They’re there when you rent your first apartment, when you’re deciding whether you can afford a home, and sometimes even when you’re planning for retirement. For millions of Americans, the real challenge isn’t just paying the loans; it’s figuring out which forgiveness programs actually apply to them, and what to do next without making costly mistakes.

This guide is designed to cut through the noise. It is clear, realistic guidance on student loan forgiveness programs, who qualifies, why they matter, and how to apply successfully in today’s changing landscape.

Understanding Student Loan Forgiveness

At its core, student loan forgiveness means some or all of your remaining federal student loan balance is erased after you meet specific requirements. This usually involves working in certain qualifying jobs, making on-time payments for a set number of years, or meeting service, income, or hardship-based criteria tied to a specific forgiveness program.

You’ll often hear forgiveness, cancellation, and discharge used interchangeably, but they apply in different situations. Forgiveness or cancellation is typically tied to your job or service (such as public service or teaching), while discharge occurs when repayment becomes impossible due to circumstances like permanent disability, school closure, or death. In all cases, forgiveness isn’t automatic, you must apply, document your eligibility, and stay compliant with program rules.

Start Here: Which Borrowers Should Pay Attention to Forgiveness Programs?

Student loan forgiveness programs aren’t one-size-fits-all. They tend to work best if at least one of these describes you:

- You work in government, education, healthcare, or a nonprofit.

- Your loan balance is high relative to your income.

- You’ve been paying for years but don’t feel like your balance is shrinking.

- You’re planning a long-term career, not job-hopping every year.

- You want predictable monthly payments instead of aggressive payoff pressure.

Federal Student Loan Forgiveness Programs You Should Know

Public Service Loan Forgiveness (PSLF)

Public Service Loan Forgiveness (PSLF) is one of the most powerful student loan forgiveness programs available. You may qualify if you work full-time for a government employer or a qualifying nonprofit, have Direct Loans (or consolidate into them), enroll in a qualifying repayment plan (typically income-driven), and make 120 qualifying monthly payments, which usually takes about 10 years.

What makes PSLF so valuable is that after those 120 qualifying payments, your remaining loan balance is forgiven tax-free. The biggest mistakes borrowers make include being on the wrong repayment plan, skipping the annual employer certification, and assuming payments count without officially verifying them.

Teacher Loan Forgiveness

If you’re an educator, there’s a second forgiveness path worth knowing about. To qualify, you must work full-time for five consecutive academic years at a low-income school or educational service agency. Eligible teachers can receive up to $17,500 in forgiveness if they teach math, science, or special education, while other qualifying teachers may receive up to $5,000. This program takes less time than PSLF, but the tradeoff is a lower forgiveness cap. In some cases, teachers eventually use both programs, just not for the same years of service.

Income-Driven Repayment (IDR) Forgiveness

If your income is modest relative to your loan balance, Income-driven repayment forgiveness may be your safety net. It caps your monthly payment based on income and family size. After 20 or 25 years of qualifying payments, any remaining balance may be forgiven.

Who Benefits Most

Income-driven repayment plans benefit borrowers with high student loan balances, those whose income isn’t expected to rise significantly over time, and people who need to prioritize cash flow for essential expenses like housing, family needs, or healthcare instead of aggressive loan payoff.

Important Timing Note

Many forms of IDR forgiveness are currently tax-free at the federal level through 2025, but future tax treatment may change. Planning ahead matters.

Forgiveness and Discharge for Special Circumstances

Total and Permanent Disability (TPD) Discharge

It allows federal student loans to be fully discharged if a borrower can no longer work due to a qualifying disability. Approval requires proper documentation and a review process, but once granted, the remaining loan balance is eliminated.

Borrower Defense to Repayment

If your school misled you or committed misconduct, you may qualify for loan discharge. These cases are highly individual and can take time, but the relief can be significant.

Closed School Discharge

If your school closed while you were enrolled (or shortly after), your federal loans may be canceled, and in some cases, past payments refunded.

What About State, Military, and Employer Assistance?

State Repayment Assistance Programs

Many states offer loan repayment assistance for teachers, healthcare workers, lawyers, and other professionals in high-need areas. These programs typically require service commitments but can dramatically reduce balances.

Military Forgiveness and Assistance

Active-duty service members, National Guard members, and veterans may qualify for loan forgiveness or repayment benefits tied to their service.

Employer-Sponsored Repayment Benefits

An increasing number of employers now contribute directly to employees’ student loans as a benefit. It’s worth asking HR for detailed information.

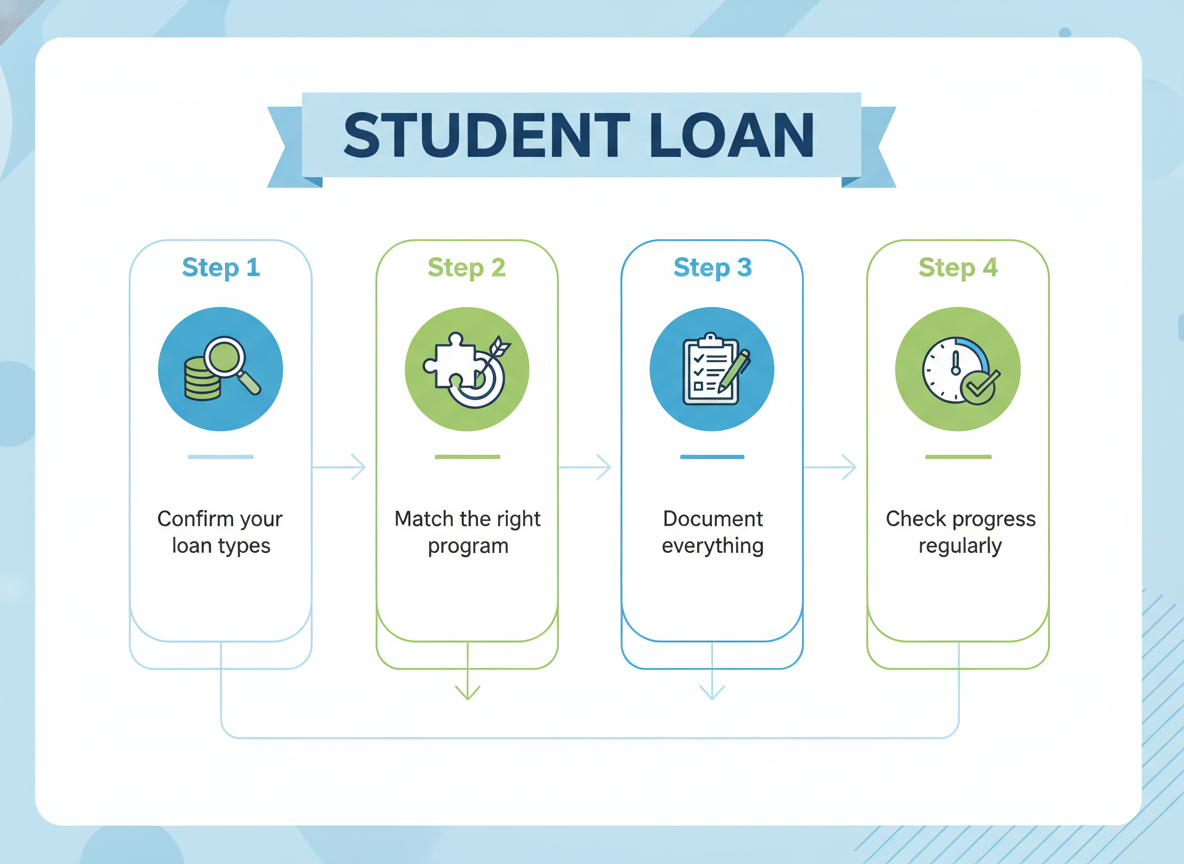

How to Apply for Student Loan Forgiveness Successfully

Step 1: Confirm Your Loan Types

Log into your Federal Student Aid account and verify whether you have Direct Loans or older FFEL or Perkins Loans, which may need to be consolidated to qualify for certain forgiveness programs.

Step 2: Match The Right Program

Choose forgiveness paths that align with your job and career plans, your repayment history, and where your income is likely headed over time.

Step 3: Document Everything

You should keep records of employment certification forms, payment confirmations, income recertifications, and communication with your loan servicer.

Step 4: Check Progress Regularly

Don’t wait 10 or 20 years to find out something went wrong. Annual reviews catch issues early, when they’re fixable.

Common Mistakes That Cost Borrowers Years

Even eligible borrowers can lose years of progress by being on the wrong repayment plan, missing income recertification deadlines, failing to consolidate when required, assuming deferment or forbearance payments count when they usually don’t, or overlooking servicer errors. Forgiveness rewards attention, not perfection, but ignoring the details can be costly.

Forgiveness Isn’t the Only Option (And That’s Okay)

If student loan forgiveness doesn’t fit your situation, there are still several alternatives that can make repayment more manageable. Income-driven repayment plans can lower your monthly payments based on your income, while federal consolidation can simplify multiple loans into a single payment and help you qualify for certain repayment options.

You can also use temporary deferment or forbearance during periods of financial hardship to pause payments, though interest may continue to accrue. Refinancing can be an option for private loans or for borrowers who aren’t pursuing federal forgiveness programs, but it’s important to note that refinancing federal loans into private ones permanently removes access to federal protections and relief options.

A Realistic Way to Think About Student Loan Forgiveness

Student loan forgiveness is a long-term agreement between you and the system: you commit to certain work, payments, or conditions, and in return, the balance eventually disappears.

For renters trying to build stability, families managing multiple financial priorities, or professionals choosing purpose-driven careers, forgiveness can be a powerful planning tool, when it’s used intentionally.

The key isn’t knowing every program. It’s knowing which one applies to you, and taking small, consistent steps to protect your progress.

Related Articles

Money Management for Students: Simple Budgeting Tips to Save More and Stress Less