For many first-time homebuyers, the dream of owning a home can seem out of reach due to the high costs and complex mortgage requirements. Thankfully, FHA loans provide a solution for those looking to buy their first home without having to meet the stringent requirements of conventional loans. The Federal Housing Administration (FHA) insures these loans, making them more accessible to first-time buyers, especially those with lower credit scores or limited savings for a down payment.

This guide explains how FHA loans work, what the requirements are, and how you can qualify. We’ll also dive into the benefits of FHA loans, the income limits, and provide actionable steps to help you navigate the process of becoming a homeowner with an FHA loan.

What is an FHA Loan?

An FHA loan is a government-backed mortgage that is designed to help individuals with less-than-perfect credit qualify for homeownership. Because the FHA insures these loans, lenders are able to offer more favorable terms to borrowers, including lower down payments and more flexible credit score requirements. This is especially helpful for first-time homebuyers, who may not have a significant credit history or the funds for a large down payment.

The FHA loan is typically used for primary residences and can be applied to single-family homes, multi-family homes (up to four units), and even some manufactured homes. FHA loans come with a 30-year fixed rate mortgage, but there are also adjustable-rate options available.

Benefits of FHA Loans for First-Time Homebuyers

There are several key benefits of using an FHA loan for your first home purchase, particularly for those who may be struggling to qualify for a conventional loan.

Low Down Payment Requirements

One of the most attractive features of FHA loans is the low down payment requirement. You only need a down payment of 3.5% of the home’s purchase price if you have a credit score of 580 or higher. For example, if the home you’re purchasing costs $250,000, you would need to put down only $8,750, making homeownership much more attainable compared to conventional loans that often require 10% to 20% down.

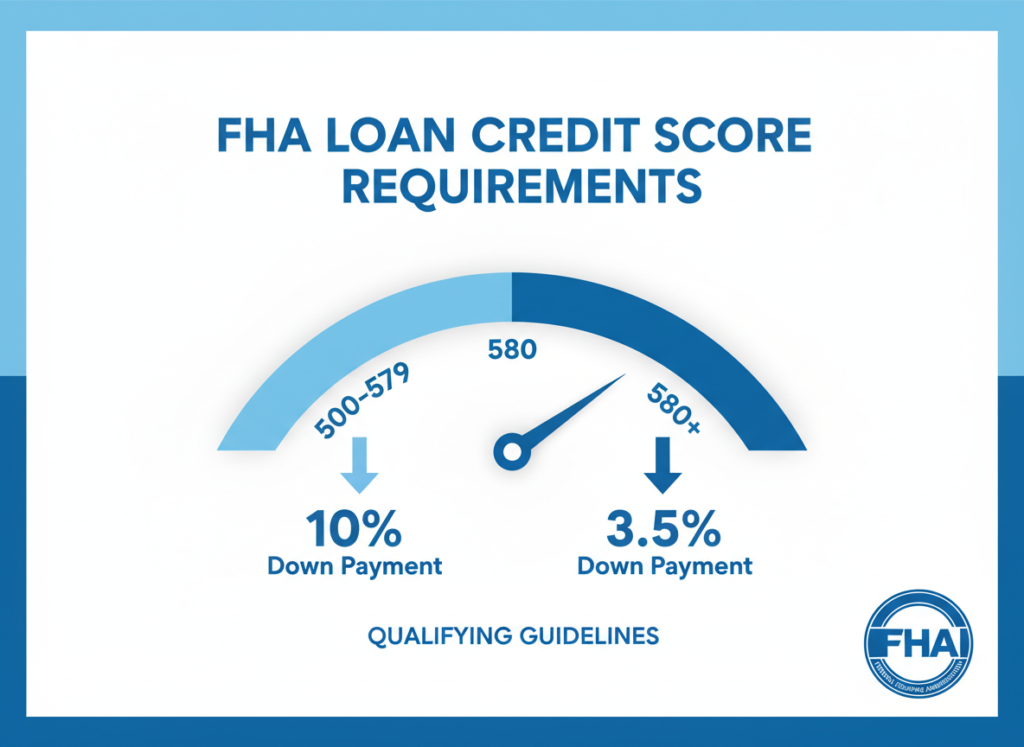

Lower Credit Score Requirements

FHA loans are more lenient on credit scores than conventional loans. While most conventional loans require a credit score of 620 or higher, FHA loans only require a minimum score of 580 to qualify for the 3.5% down payment. If your credit score is between 500 and 579, you may still qualify for an FHA loan, but you’ll need to put down 10%.

Higher Debt-to-Income Ratios

Unlike conventional loans, which often have strict debt-to-income (DTI) ratio limits, FHA loans allow for higher DTIs. Most lenders require a DTI of 43% or lower to qualify, but FHA loans may allow higher ratios depending on your credit score and other factors. This is particularly beneficial for those with student loans or other debts.

Competitive Interest Rates

FHA loans tend to offer competitive interest rates due to the backing from the government, which reduces the risk for lenders. This can save you a significant amount of money over the life of the loan.

Mortgage Insurance

While FHA loans do require mortgage insurance, it’s typically lower than conventional loans, making it a more affordable option for first-time buyers. FHA loans require both upfront mortgage insurance premiums (UFMIP) and annual mortgage insurance premiums (MIP), but these costs are often more manageable than the private mortgage insurance (PMI) required by conventional loans.

Eligibility Requirements for FHA Loans

Credit Score

To qualify for the 3.5% down payment, your credit score must be 580 or higher. If your score is between 500 and 579, you may still be eligible, but you’ll need to put down 10%. Your credit score will also affect your interest rate and monthly payments.

Down Payment

As mentioned, the minimum down payment for an FHA loan is 3.5% if your credit score is 580 or higher. If your credit score is between 500 and 579, the down payment requirement increases to 10%.

Debt-to-Income (DTI) Ratio

FHA loans allow for a DTI ratio of up to 43%, though some lenders may approve higher ratios under certain conditions. Your DTI ratio is calculated by dividing your total monthly debt payments (including your new mortgage) by your gross monthly income.

Employment History

The FHA requires at least two years of steady employment. This helps lenders ensure that you have a reliable income stream to make your mortgage payments. If you’ve recently changed jobs, as long as you’ve stayed in the same line of work, you may still be eligible.

Property Eligibility

The property must be your primary residence. Investment properties and vacation homes aren’t eligible for FHA loans. Additionally, the property must meet the FHA’s minimum property standards, which ensures that the home is safe and habitable.

How to Qualify for an FHA Loan: A Step-by-Step Guide

Step 1: Check Your Credit Score

Before applying for an FHA loan, check your credit score to ensure it meets the minimum requirement. If your score is below 580, you may want to focus on improving it before applying. Even a slight improvement can make a big difference in your down payment and loan terms.

Step 2: Assess Your Debt-to-Income Ratio

Take a look at your current debts and monthly expenses to ensure your DTI ratio is within the acceptable range. If your DTI is too high, consider paying off some debt before applying for the loan.

Step 3: Get Pre-Approved

Reach out to an FHA-approved lender to get pre-approved. Pre-approval will give you a better understanding of how much you can afford, the interest rate you can expect, and what your down payment will be.

Step 4: Find a Home Within Your Budget

Once you’re pre-approved, start searching for homes that fall within your budget. Make sure the property meets the FHA’s standards and that it’s within the price limit for your area.

Step 5: Submit Your Application

Once you’ve found a home, submit your FHA loan application along with the necessary documentation, including proof of income, employment history, credit score, and any other supporting documents.

Step 6: Close the Deal

After your application is processed and approved, you’ll go through the closing process. Be prepared to pay closing costs, which typically range from 2% to 5% of the loan amount. Once the deal is finalized, you’ll officially own your new home!

Drawbacks of FHA Loans

While FHA loans are beneficial, they do come with some drawbacks that you should consider:

- Mortgage insurance: FHA loans require both an upfront mortgage insurance premium (UFMIP) and monthly mortgage insurance premiums (MIP). These costs can add up, especially for buyers with smaller down payments.

- Property restrictions: The FHA has strict guidelines for the condition of the property. If the home needs significant repairs or doesn’t meet FHA standards, it may not qualify for the loan.

- Loan limits: FHA loan limits vary by region and can be lower than the purchase price of homes in high-cost areas. It’s important to check the loan limits for your area before applying.

Final Thoughts: Is an FHA Loan Right for You?

FHA loans offer an excellent opportunity for first-time homebuyers to achieve homeownership with less financial strain. With low down payments, flexible credit score requirements, and competitive interest rates, FHA loans make it easier for people with less-than-perfect credit or limited savings to enter the housing market.

However, it’s essential to carefully consider the costs, including mortgage insurance and potential property restrictions. By following the steps outlined in this guide, you can determine if an FHA loan is the best option for you and your family.

Start by assessing your financial situation, checking your credit score, and consulting with an FHA-approved lender. With the right preparation, you’ll be on your way to securing your first home with an FHA loan, bringing you one step closer to achieving your homeownership goals.

Related Articles

FHA Loans for Mobile Homes: Requirements, Property Rules, Loan Limits, and How to Qualify