Building home equity is one of the most important steps toward achieving financial stability and long-term wealth. Home equity is the value of your home that you truly own, and understanding how it works can open up a wealth of opportunities. Whether you’re looking to use your equity for home improvements, debt consolidation, or retirement savings, knowing how to build and use your home equity smartly can help you achieve your financial goals. In this guide, we’ll explore what home equity is, how to build it, and the smartest ways to leverage it for your future.

What Is Home Equity?

Home equity refers to the difference between the current market value of your home and the amount you owe on your mortgage. If your home is worth more than what you owe, the difference is your equity.

For example, if your house is valued at $350,000 and you have a $200,000 mortgage balance, you have $150,000 in home equity. Over time, your equity increases as you pay off your mortgage or if the value of your home rises due to market appreciation or improvements.

Your home equity grows in two ways:

- Paying down the mortgage: Each monthly payment reduces the loan balance, gradually increasing your ownership stake in the home.

- Appreciation: If your home’s market value increases over time, so does your equity. This could happen due to neighborhood improvements, renovations, or rising home prices in the broader market.

How Does Home Equity Work?

Understanding how home equity works can help you make more informed decisions about your property and finances. As you pay off your mortgage, a portion of each payment goes toward reducing the principal balance, which increases the equity you hold in your home. Additionally, if the market value of your home increases, your equity will grow as well.

For instance, if you bought your home for $250,000 and, after five years, it’s now worth $280,000, your equity has grown simply due to the increase in value, even if you haven’t made any extra payments on the principal. However, it’s important to remember that your equity could also decrease if the value of your home drops due to changes in the housing market.

How to Build Equity in Your Home

Make Extra Payments

Paying more than your required monthly mortgage payment can help you pay down your principal faster. Even small additional payments, like $100 extra per month, can significantly reduce your principal balance and increase your equity over time.

Choose a Shorter Loan Term

If you’re in a position to afford higher monthly payments, consider refinancing your mortgage into a shorter loan term, such as 15 years instead of 30 years. While this increases your monthly payment, it reduces the total amount of interest you pay, helping you build equity faster.

Renovate or Improve Your Home

Making smart home improvements can increase the market value of your property, which in turn boosts your equity. Upgrades like kitchen remodels, bathroom renovations, or even landscaping improvements can yield a high return on investment and increase the perceived value of your home.

Avoid Refinancing Too Often

While refinancing may offer a lower interest rate, doing it repeatedly can extend your loan term and result in paying more interest over time. It’s better to stick with your original mortgage if you want to build equity faster.

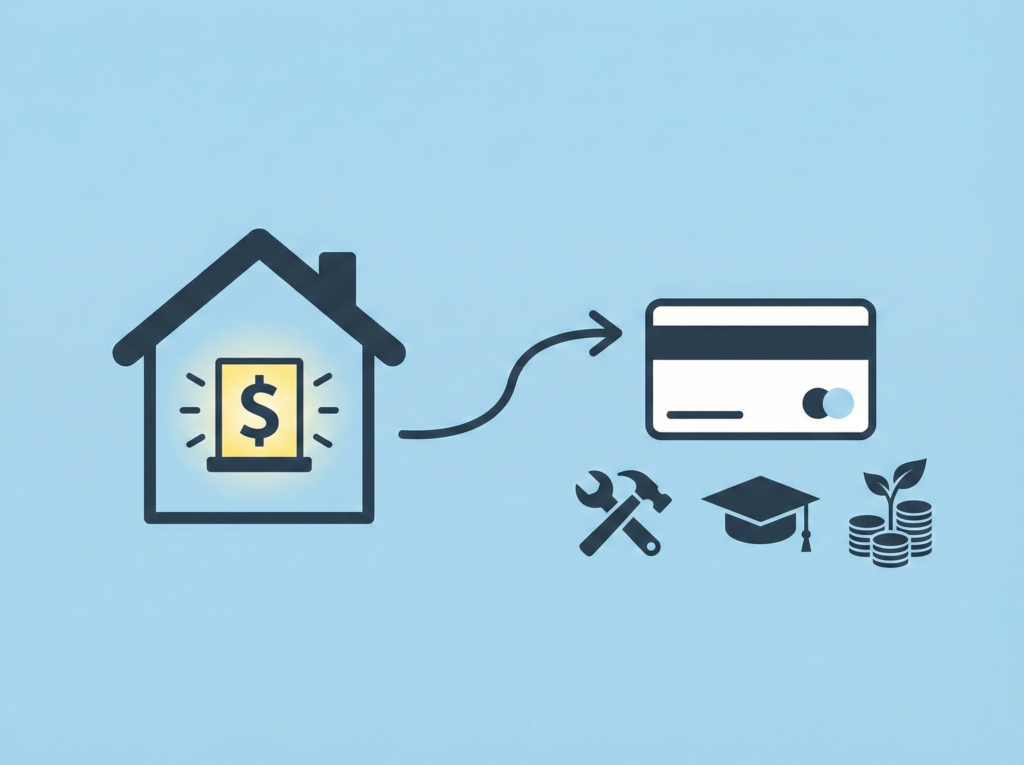

How to Use Your Home Equity

Home Equity Loans

A home equity loan is a lump-sum loan that allows you to borrow against your home’s equity. These loans usually have fixed interest rates and a set repayment period. They’re ideal for funding large expenses like home renovations, college tuition, or medical bills. However, since your home is used as collateral, failing to repay the loan could result in losing your home.

Home Equity Line of Credit (HELOC)

A HELOC works like a credit card. It allows you to borrow up to a certain limit, but only when you need the money. HELOCs usually come with variable interest rates. While they can be useful for ongoing expenses, like emergency repairs or funding a small business, they carry the risk of fluctuating interest rates that could increase your payments over time.

Cash-Out Refinance

A cash-out refinance replaces your existing mortgage with a larger one, and you receive the difference in cash. This option allows you to access your home equity at a potentially lower interest rate than other forms of borrowing. However, it’s important to note that refinancing may come with closing costs, and you’ll be paying interest on the entire new loan amount.

Each of these options has its pros and cons, so it’s important to assess your financial situation, goals, and ability to repay before using home equity.

Key Benefits of Using Home Equity

Lower Interest Rates

Home equity loans and HELOCs typically have lower interest rates than credit cards or personal loans, making them a cost-effective way to borrow money.

Tax Deductions

The interest paid on home equity loans used for home improvements may be tax-deductible, which can make borrowing more affordable. Be sure to consult with a tax advisor to understand the specifics.

Access to Large Sums of Money

If you need access to a large amount of money, home equity can be an effective way to borrow. With the right loan, you can access substantial funds for things like debt consolidation or major life events.

Flexible Uses

You can use the funds from home equity loans and HELOCs for a variety of purposes, from home renovations to starting a business or paying for educational expenses.

Risks of Borrowing Against Home Equity

Risk of Foreclosure

Since home equity loans and HELOCs are secured by your property, failing to make payments can lead to foreclosure, where the lender takes possession of your home.

Increased Debt

Borrowing against your home equity increases your total debt. If you don’t manage it wisely, you could find yourself in a worse financial position, especially if you fail to make timely payments.

Fees and Costs

Home equity loans and HELOCs come with various fees, such as application fees, closing costs, and annual maintenance fees. These costs can eat into the potential benefits of using your home equity.

Fluctuating Interest Rates

If you use a HELOC, your interest rate could increase if market rates rise, which may result in higher monthly payments and more interest over time.

Conclusion: Should You Use Home Equity?

Home equity can be a powerful tool for building wealth and accessing funds for major expenses, but it should be used responsibly. By understanding how equity works, how to build it, and how to use it wisely, you can make informed decisions about leveraging your home’s value. Whether you need a loan for home improvements, education, or debt consolidation, using your equity can provide significant financial flexibility.

However, it’s important to consider the risks, such as potential foreclosure and the impact on your long-term financial stability. Always weigh your options carefully and consult with a financial advisor to make sure you’re making the right move for your future.