Finding the right mortgage lender is one of the most important steps in purchasing a home. A mortgage is a long-term commitment, and the lender you choose can greatly impact your financial future. Whether you’re a first-time homebuyer or refinancing, understanding how to choose the best mortgage lender will help you make informed decisions, save money, and secure the right loan for your needs. Here’s a comprehensive guide to understanding how mortgage lenders work, what factors to consider, and how to navigate the mortgage process to find the best deal.

What is a Mortgage Lender?

A mortgage lender is a financial institution or individual that provides the funds for purchasing a home. Mortgage lenders can range from traditional banks and credit unions to online lenders and mortgage brokers. They offer different loan types, rates, and terms, making it essential to compare options before committing.

Mortgage lenders can also play a vital role in the home-buying process by offering guidance, helping you understand loan documents, and ensuring your eligibility for the loan you want. The mortgage lender you choose can have a significant impact on the overall cost of your loan, so it’s essential to evaluate lenders based on key factors such as loan types, customer service, rates, fees, and more.

Key Factors to Consider When Choosing a Mortgage Lender

Loan Types and Options

There are several types of loans available, and different lenders specialize in different products. These can include:

- Conventional loans: Most common and offered by banks and credit unions.

- FHA loans: Government-backed loans for first-time homebuyers and those with less-than-perfect credit.

- VA loans: Loans for veterans and active military personnel with favorable terms.

- Jumbo loans: Loans for purchasing high-value properties.

Understanding which loan type works best for your situation will help you choose the right lender.

Interest Rates and APR

Interest rates directly affect the total amount you pay over the life of the loan. Lenders offer different rates based on factors like your credit score, loan type, and down payment size. Mortgage rates can be either fixed or variable, with fixed rates providing stability and predictability in monthly payments, while adjustable rates may offer lower initial rates that can fluctuate over time.

The APR (Annual Percentage Rate) includes not just the interest rate but also fees and additional costs of the loan, giving you a more accurate sense of the loan’s total cost.

Customer Service and Support

Buying a home is a major financial decision, and the process can be complex and stressful. A lender with strong customer service and responsive support can make a big difference. Look for a lender who offers clear communication, has a user-friendly application process, and is available to answer your questions quickly.

Fees and Closing Costs

All mortgages come with fees, but the types and amounts can vary by lender. These fees can include application fees, origination fees, underwriting fees, and closing costs. It’s important to get a detailed estimate of all associated fees and ask about any potential hidden charges. Some lenders may offer to waive certain fees to make their offer more attractive.

Loan Terms and Flexibility

Look at the terms of the loan, such as the length of the repayment period and whether there are options for early repayment without penalties. Some lenders also offer more flexibility in payment options, allowing you to make extra payments toward your principal or choose a repayment schedule that works best for your financial situation.

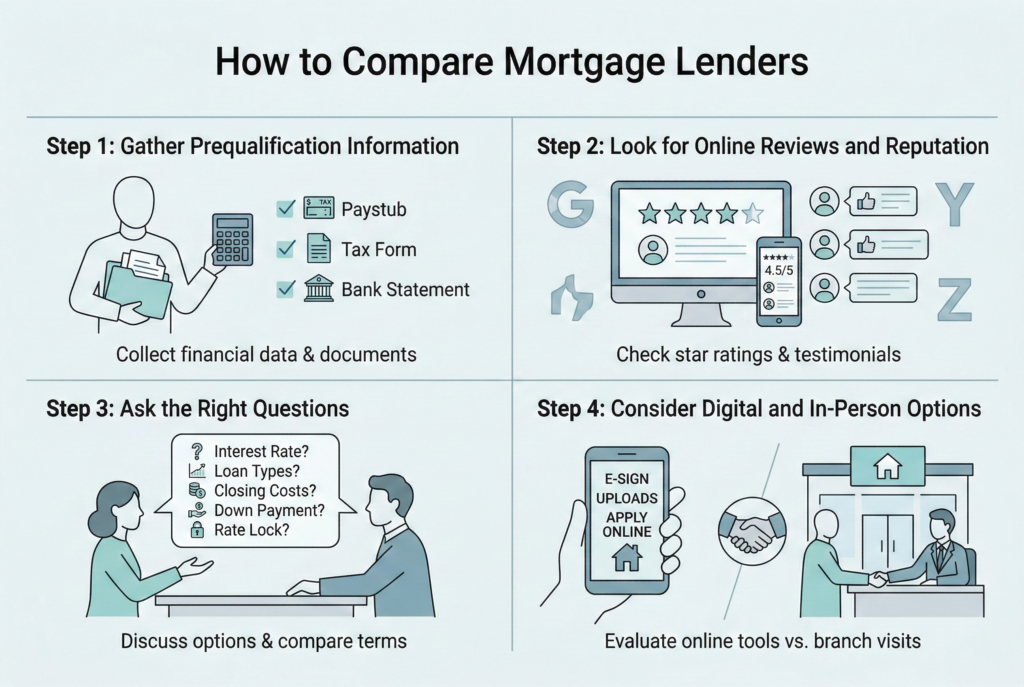

How to Compare Mortgage Lenders

Step 1: Gather Prequalification Information

Start by gathering the necessary information about your income, credit score, and debt-to-income ratio. This will help lenders provide you with accurate prequalification offers. You should compare multiple lenders at this stage, using the details of their offerings to determine which one best fits your needs.

Step 2: Look for Online Reviews and Reputation

Customer reviews and ratings on websites like NerdWallet, Bankrate, and Zillow can provide insights into the experience of other borrowers. Look for a lender with a solid reputation for transparency, competitive rates, and excellent customer service.

Step 3: Ask the Right Questions

When you’ve narrowed down your list of potential lenders, it’s time to ask them a few important questions. These questions can include:

- What loan types do you offer?

- What are your interest rates and APRs?

- Are there any lender-specific fees?

- How long does the approval process take?

These questions will help you understand what to expect from each lender and allow you to make an informed decision.

Step 4: Consider Digital and In-Person Options

With the rise of digital mortgage lenders, it’s now easier than ever to shop for a loan online. However, some people prefer face-to-face interactions, especially if they have complex financial situations. Decide which option works best for you and compare both digital and traditional lenders.

The Importance of Mortgage Preapproval

Once you’ve compared lenders and found a few that match your needs, the next step is preapproval. Mortgage preapproval is a process in which the lender reviews your financial situation and provides you with a loan offer. This not only helps you understand how much you can borrow but also shows sellers that you’re a serious buyer. The preapproval process typically requires documentation like:

- Proof of income (pay stubs, tax returns)

- Credit report

- Proof of assets (bank statements)

By getting preapproved, you’ll be better equipped to negotiate terms and finalize your loan.

Final Thoughts: Choosing the Right Mortgage Lender

Choosing the right mortgage lender is a critical step in the home-buying process. By carefully considering your options, comparing multiple lenders, and understanding the various types of loans, you can find the best deal for your financial situation. Take the time to research different lenders, ask the right questions, and ensure you feel comfortable with your decision.

Remember, shopping around for the best mortgage lender can save you money in the long run. With the right lender by your side, you can confidently navigate the home-buying process and move into the home of your dreams.