Savings Planner: Quick, Easy Strategies to Maximize Retirement Contributions")

Planning for retirement can feel overwhelming, especially when your 401(k) statements are full of numbers that don’t clearly answer the question you actually care about: Am I on track?

If you’re juggling bills, rising costs, career changes, or family priorities, retirement savings can easily slide to the bottom of the list. This guide is designed to change that. Using the source material you provided as a foundation, this article turns complex rules into simple, motivating strategies you can actually use without a finance degree required.

Whether you’re just starting out or trying to catch up, this 401(k) savings planner will help you make confident, practical decisions that move your future forward.

Why Your 401(k) Matters More Than You Think

For most Americans, a 401(k) is the backbone of retirement. It’s automatic, tax-advantaged, and often comes with employer contributions, but many people still underuse it.

Common challenges people face include: “I’m not saving enough, but I don’t know how much is enough,” “I don’t want to lock up money I might need,” and “I’m worried I started too late.” The truth is, it isn’t as complex as it may seem. What matters most is having a plan that works for your current life and financial situation. Start small, stay consistent, and adjust as you go. The progress, no matter how gradual, is key to building a secure financial future.

How a 401(k) Works

A 401(k) is a workplace retirement account that lets you save directly from your paycheck. The money goes in automatically, before you even see it hit your bank account, which makes saving easier and more consistent.

Here’s what makes a traditional 401(k) powerful: First, it offers tax-deferred growth, meaning you don’t pay income taxes on contributions or investment growth until retirement, allowing your money to grow faster. Many employers also offer a match when you contribute, which acts as a valuable part of your compensation. Additionally, the power of compounding over time comes into play: your money earns returns, and those returns then generate their own returns, creating a snowball effect that can significantly boost your retirement savings.

Therefore, even modest contributions can grow significantly when given enough time.

Traditional vs. Roth 401(k): Which One Should You Choose?

Choose a traditional 401(k) if you want a tax break today and expect your tax rate to be lower in retirement. It’s a good option if you’re focused on maximizing your take-home pay now, as contributions are made pre-tax, lowering your taxable income. On the other hand, choose a Roth 401(k) if you’re early in your career, earning less currently, or expect to face higher taxes in the future. With a Roth 401(k), your contributions are made after-tax, but withdrawals in retirement are tax-free, making it a strong choice if you want to avoid paying taxes on your retirement savings down the road.

The Employer Match: Don’t Leave Free Money Behind

Employer matching is one of the most powerful and most overlooked benefits in personal finance because it boosts your savings instantly without any extra effort.

Here’s how it works in real life:

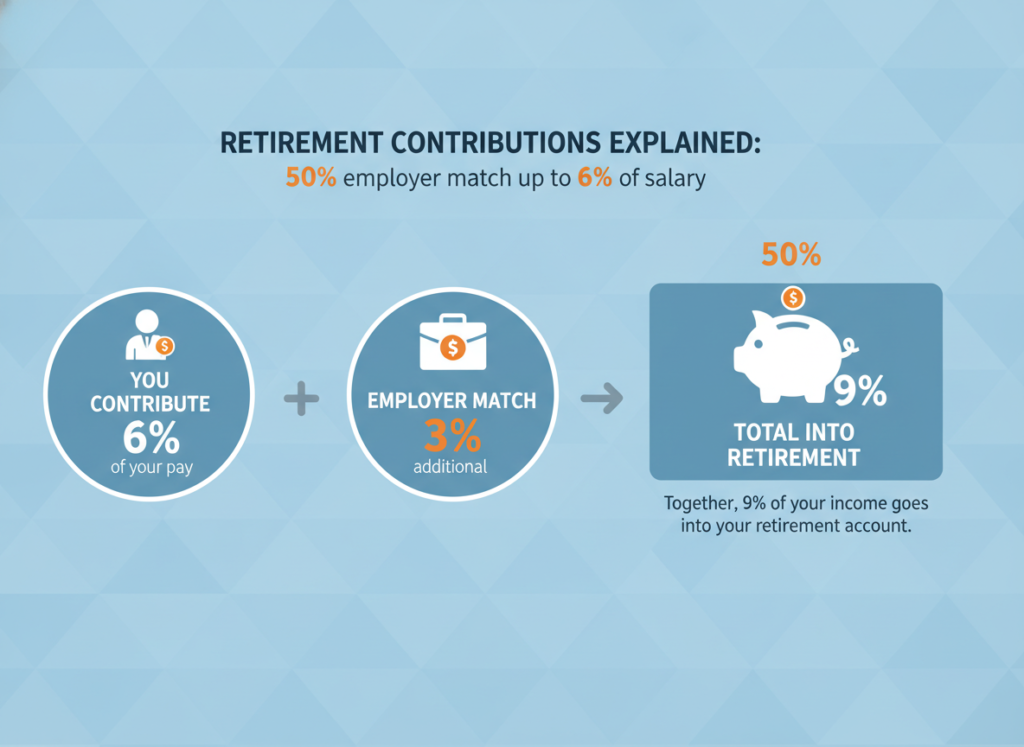

If your employer offers a 50% match on contributions up to 6% of your salary, this means: You contribute 6% of your pay while your employer contributes an additional 3%. Together, 9% of your income goes into your retirement account.

That employer contribution is part of your total compensation. If you don’t contribute enough to earn it, you’re effectively leaving money on the table.

What makes this especially powerful is the math behind it. A 50% employer match gives you an immediate, risk-free 50% return on your contributions. There’s no other investment that reliably offers that kind of return with zero downside.

Why this matters long-term: Employer match money compounds over decades, significantly boosting your retirement savings. It lowers the amount you need to save out of pocket, making it easier to reach your retirement goals. Over time, this match can add tens or even hundreds of thousands of dollars to your retirement fund, creating a substantial impact on your financial future.

Simple rule of thumb: Before investing anywhere else or before extra debt payments, taxable investments, or even increasing savings beyond the basics, you should always contribute enough to your 401(k) to get the full employer match. It’s the fastest, easiest way to accelerate your retirement savings and one of the smartest financial moves you can make.

How Much Should You Contribute? A Realistic Framework

Age-Based 401(k) Contribution Targets

(Percentages include both your contribution and your employer match)

- In your 20s: Aim for 10%–15%. The goal here is building the habit. Even modest contributions benefit enormously from time and compounding.

- In your 30s: Target 15%–20%. As income grows and finances stabilize, increasing contributions helps close early gaps and strengthen momentum.

- In your 40s: Work toward 20%–30%. This is often the highest-earning decade and a critical window to accelerate savings before retirement gets closer.

- In your 50s and beyond: Contribute as much as possible. Take advantage of IRS catch-up contributions to make up for lost time and maximize tax-advantaged savings.

If these ranges feel overwhelming, that’s completely normal, especially if you’re managing debt, housing costs, or family expenses. The most important thing isn’t hitting the perfect percentage overnight. It’s your consistency.

Contribution Limits You Should Know (2025–2026)

Here’s a simple breakdown of what you can contribute: 2025 employee contribution limit is $23,500 and $24,500 for 2026.

If you’re closer to retirement, the IRS allows additional savings. The first one is catch-up contributions (age 50 and older), with up to $8,000 in 2026 on top of the standard limit. The second one is special catch-up contributions (ages 60–63), in which eligible workers can contribute an extra $11,250 in both 2025 and 2026.

One important clarification that often causes confusion: Your employer’s contributions don’t reduce how much you’re allowed to contribute personally. However, they do count toward the plan’s overall annual maximum set by the IRS.

A Simple 401(k) Contribution Playbook

Use this step-by-step approach to prioritize without stress:

- Contribute enough to get the full employer match

- Build a basic emergency fund (3–6 months of expenses)

- Pay down high-interest debt

- Increase your 401(k) toward 15%+

- Consider IRAs or other investments if you max out

This order helps you balance today’s needs with tomorrow’s security.

What Actually Grows Your 401(k) Balance

Growing your 401(k) depends on building steady habits that work in any market. The people who succeed long term aren’t the ones who time things perfectly; they’re the ones who stay consistent, even when headlines are noisy or markets feel uncertain.

What truly drives 401(k) growth is surprisingly simple. Your contribution rate matters more than almost anything else. The amount you save, and how often you increase it, has a bigger impact over time than trying to pick the “perfect” investment. Time in the market is just as important. The longer your money stays invested, the more compounding can do its job.

The employer match adds another powerful layer of growth. Those matched dollars go into your account immediately and compound alongside your own contributions. Investment fees also play a quiet but critical role. High fees can slowly erode returns year after year, while lower-cost options allow more of your money to stay invested and work for you. And finally, staying invested through market ups and downs is essential. Market swings are normal, but pulling out during downturns often causes more harm than good. Remaining invested gives your portfolio the chance to recover and grow over time.

For many people, a simple, low-stress way to put all of this into practice is through target-date funds. These funds are designed around your expected retirement year and automatically adjust your investment mix as you age. If you don’t want to actively manage your investments or worry about rebalancing, target-date funds offer a true “set-it-and-forget-it” approach.

Fees: The Silent Growth Killer

Fees may seem harmless at first glance, but over time they can quietly become one of the biggest drags on your retirement savings. A difference that looks tiny, like 0.25% versus 1% can end up costing tens of thousands of dollars over the course of a few decades.

Protecting your 401(k) from fee drag starts with awareness. Every fund in your plan has an expense ratio, which is the annual cost of owning that investment. Even fractions of a percent matter when they’re applied year after year, so it’s worth taking a few minutes to review what you’re paying.

When possible, favor low-cost index funds or target-date funds, which tend to offer broad diversification with lower fees, allowing more of your returns to stay invested and grow over time. It’s also important to resist the urge to overtrade or chase recent performance. Frequently switching funds often leads to higher costs and weaker results, while a steady, long-term approach typically wins out.

The bottom line is simple: you can’t control what the market does, but you can control how much you pay to invest. Keeping fees low is one of the easiest and most effective ways to improve your long-term retirement outcomes.

Life Happens: What If You Change Jobs?

If you leave a job, your 401(k) doesn’t disappear. Instead, you do need to decide what to do with it, normally with these four main options:

- Leave the money in your former employer’s plan: If the plan allows it, you can keep your savings where they are and let them continue to grow, though you won’t be able to make new contributions.

- Roll the balance into your new employer’s 401(k): This keeps all your retirement savings in one place and maintains the tax advantages, making your accounts easier to manage.

- Roll the funds into an IRA: An IRA rollover often provides more investment choices and potentially lower fees, while preserving the tax-deferred status of your savings.

- Cash out the account: This option usually comes with income taxes and early-withdrawal penalties if you’re under 59½, making it the least favorable choice for long-term retirement goals.

One important note: many people lose track of old 401(k) accounts over time. Consolidating your retirement savings can simplify your finances, reduce fees, and make it much easier to stay organized.

Early Withdrawals, Loans, and RMDs: What to Watch For

Accessing your 401(k) comes with important rules, and understanding them ahead of time can help you avoid expensive surprises.

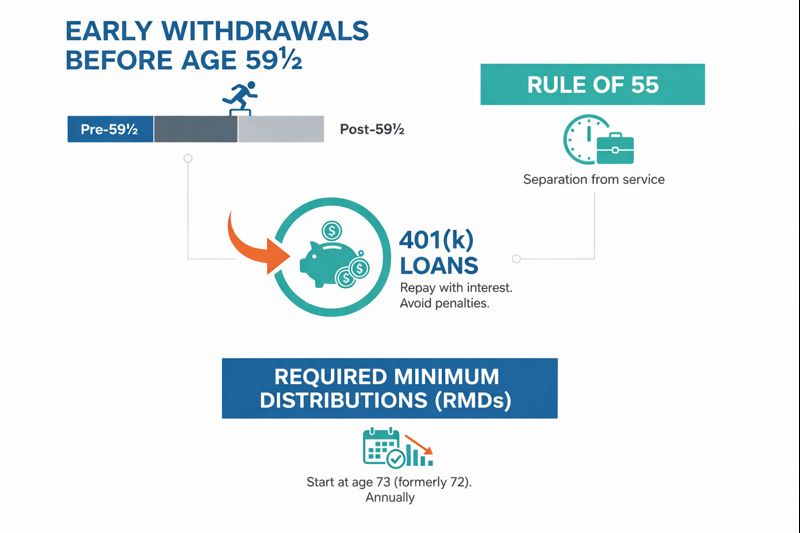

With early withdrawals before age 59½, the IRS generally treats the money as taxable income and adds a 10% early-withdrawal penalty. There are limited exceptions, but in most cases, tapping your 401(k) early comes at a cost.

The Rule of 55 can offer some flexibility. If you leave your job in or after the year you turn 55, you may be able to take withdrawals from that employer’s 401(k) without the 10% penalty, though regular income taxes still apply.

Some plans also allow 401(k) loans, which can provide short-term access to funds in an emergency. While this avoids taxes and penalties upfront, loans carry risks, especially if you leave your job before the loan is repaid.

Later in life, Required Minimum Distributions (RMDs) come into play. For most people, RMDs begin at age 73, with the starting age increasing to 75 in 2033. Missing a required withdrawal can trigger penalties, but the IRS has reduced those penalties if the mistake is corrected quickly.

The Mindset Shift That Makes the Biggest Difference

The most important thing in retirement planning is staying consistent and understanding what actually moves the needle. Almost everyone has moments of doubt, thinking, “I’m already behind,” or “I’ll figure this out later.” Those thoughts are normal, but they don’t have to define your future.

Yes, the best time to improve your 401(k) may have been years ago, but the second-best time is right now. Reviewing your current contributions, increasing them by just 1%, or switching to lower-cost, better-aligned funds can quietly reshape your long-term outlook. Plus, they create confidence, reduce financial stress, and give you more options.

Final Takeaway: Make Your 401(k) Work for You

Your 401(k) is a long-term collaboration between your paycheck, your employer’s contributions, and the life you want in the future. When you approach it with the right mindset, it doesn’t have to feel overwhelming.

You don’t need to max it out all at once, and you don’t need flawless timing to succeed. What truly matters is having a plan that evolves as your income, responsibilities, and goals change. Begin with what’s realistic today, make small adjustments along the way, and stay consistent.

Related Articles

401(k) vs IRA vs Roth IRA: Key Differences Explained for Every Income Level