A glide path is one of the most important concepts in retirement planning because it influences how your investment mix changes as you get older. Instead of keeping the same level of risk throughout your working years and into retirement, a glide path gradually adjusts your portfolio over time. That shift is meant to balance growth potential with the need for greater stability as retirement gets closer.

What a Glide Path Means in Retirement Planning

In retirement investing, a glide path is the schedule or strategy that determines how your asset allocation changes over time. Most often, it refers to the way a portfolio gradually moves from a higher allocation to stocks when retirement is far away to a more conservative mix of bonds and cash-like assets as retirement approaches.

The basic idea is simple. Younger investors usually have more time to recover from market downturns, so their portfolios often hold more stocks for long-term growth. As retirement gets nearer, the focus usually shifts toward reducing volatility and protecting accumulated savings. A glide path creates that transition in a structured way rather than leaving it to guesswork or emotion.

This concept is especially common in target-date funds, where the investment mix automatically becomes more conservative over the years. Still, a glide path can also be used in self-managed portfolios when investors rebalance according to a long-term retirement strategy.

Why a Glide Path Matters for Retirement Investors

A glide path matters because retirement investing isn’t only about pursuing the highest return. It’s also about managing risk in a way that fits your timeline, goals, and future spending needs. A portfolio that feels appropriate at age 30 may be far too aggressive at age 63, especially if retirement withdrawals are getting close.

Without a glide path, investors may take on either too much or too little risk for their stage of life. Too much risk can expose retirement savings to major market losses right before or during retirement. Too little risk can limit long-term growth and make it harder for savings to keep pace with inflation.

A well-designed glide path helps solve this problem by creating a gradual shift rather than a sudden change. That can make the portfolio feel more balanced over time and reduce the chance of making reactionary investment decisions during periods of market stress.

How a Glide Path Typically Works

Most glide paths begin with a growth-oriented allocation when retirement is decades away. That often means a heavier weighting toward stocks, which historically have offered stronger long-term return potential than more conservative assets, though they also come with more short-term volatility.

As the target retirement date gets closer, the allocation typically shifts in stages. Stock exposure decreases while bond exposure rises. In some cases, cash or short-term reserves may also increase. The exact pace depends on the strategy being used.

For example, someone early in their career might hold a portfolio that leans heavily toward stocks. Twenty or thirty years later, that same portfolio may look very different, with a larger share in bonds and fewer assets exposed to stock market swings. The transition doesn’t usually happen all at once. It unfolds gradually over many years. This gradual adjustment is what gives the glide path its name. The portfolio doesn’t abruptly jump from aggressive to conservative. It follows a descending path of risk as retirement approaches.

The Connection Between Glide Path and Target-Date Funds

Many people first encounter the idea of a glide path through target-date funds. These funds are built around a projected retirement year, and their asset allocation changes automatically as that date approaches.

For example, a target-date fund designed for someone planning to retire around 2055 will generally start with a more growth-focused mix than a fund built for someone retiring around 2030. Over time, the 2055 fund’s glide path will gradually reduce stock exposure and increase holdings in more conservative investments.

This automation is a major reason target-date funds are popular in retirement plans. Investors don’t need to manually adjust the allocation every few years. The fund follows a preset glide path based on the expected retirement timeline.

That said, not every target-date fund uses the same glide path. Two funds with the same retirement year can have noticeably different stock and bond allocations depending on the provider’s philosophy. That’s why investors shouldn’t assume all target-date funds behave the same way.

“To” Retirement vs. “Through” Retirement Glide Paths

One important distinction is whether a glide path is designed to retirement or through retirement. This difference affects how conservative the portfolio becomes by the target date and what happens after retirement begins.

A to retirement glide path generally becomes more conservative by the time the target date arrives. It’s designed with the idea that the investor may want stronger protection against volatility right around retirement age.

A through retirement glide path usually continues adjusting after the retirement date, often keeping a higher stock allocation for longer. The reasoning is that retirement may last for decades, so the portfolio still needs growth potential even after paychecks stop.

Neither approach is automatically better. The right fit depends on the investor’s withdrawal strategy, other income sources, spending needs, and tolerance for market fluctuations in retirement. Someone with a pension or substantial guaranteed income may feel comfortable with a more growth-oriented path, while someone relying heavily on portfolio withdrawals may prefer a more conservative structure.

How a Glide Path Helps Reduce Risk Over Time

A glide path reduces risk by lowering exposure to large market swings as retirement draws closer. This matters because market losses can be especially damaging when they happen near the point when withdrawals are about to begin.

This issue is often called sequence of returns risk. If a retiree experiences a major market decline early in retirement while also withdrawing money, the portfolio may have a harder time recovering. A glide path attempts to lower that vulnerability by gradually reducing stock exposure before and around retirement.

It also helps from a behavioral standpoint. Many investors find it easier to stay committed to a plan when risk is adjusted systematically rather than emotionally. Instead of making sudden changes during periods of fear, they follow a structure that already anticipates the need for lower volatility later in life.

That doesn’t mean a glide path eliminates risk. Even conservative portfolios can lose value, and inflation remains a serious concern in retirement. But it can help align the portfolio with a stage of life when preserving capital often becomes more important.

The Main Factors That Shape a Glide Path

There’s no single glide path that works for everyone. Several factors influence what the right path may look like.

One of the biggest is the time horizon. Someone who is 25 and saving for retirement has a very different timeline from someone who is 60 and planning to retire in five years. The longer the time horizon, the more room there may be for growth-focused investing.

Another factor is risk tolerance. Some investors can handle market volatility without panicking, while others lose sleep when balances fall sharply. A glide path should reflect not only financial theory but also the investor’s real-world comfort level.

Expected retirement income also matters. People with pensions, Social Security benefits, rental income, or other reliable cash flow may be able to tolerate more investment risk than those relying mainly on their retirement accounts. Spending needs, health, family situation, and legacy goals can also influence how conservative or aggressive a glide path should be over time.

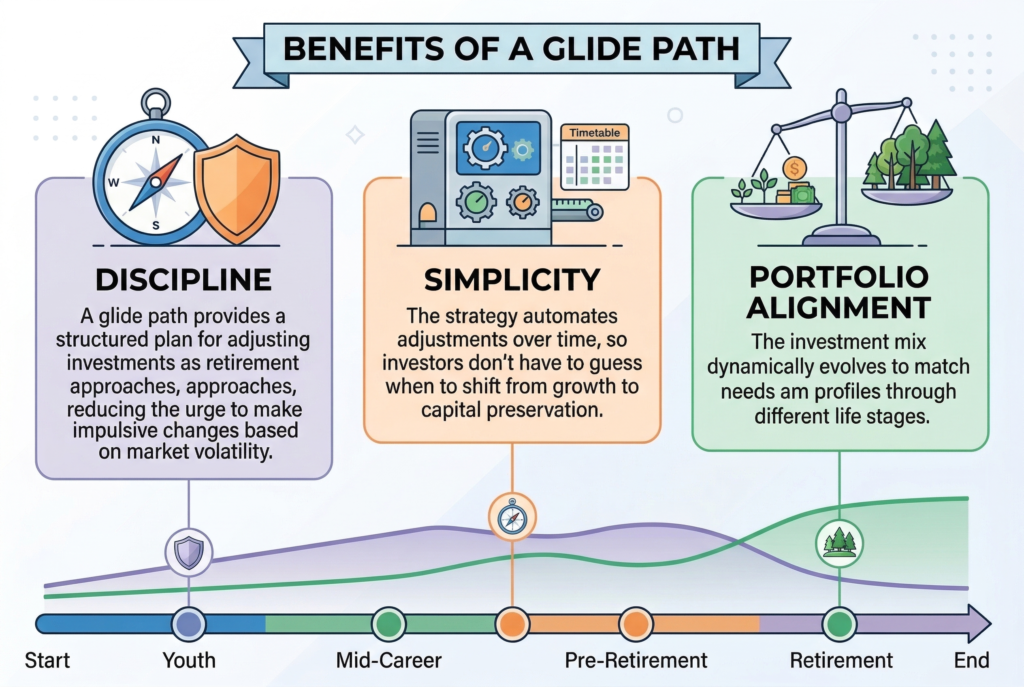

Benefits of Using a Glide Path

One of the biggest benefits is discipline. A glide path creates a clear plan for adjusting investments as retirement gets closer, which reduces the temptation to make impulsive changes based on market headlines.

Another benefit is simplicity. Investors don’t need to guess when to shift from aggressive growth to greater preservation. The strategy already includes a timetable or framework for making those changes.

A glide path can also improve portfolio alignment. Instead of using the same allocation at every stage of life, the investment mix evolves along with the investor’s needs. That creates a more realistic relationship between risk and retirement timing. For many people, the real value is peace of mind. Knowing that the portfolio is designed to become more balanced over time can make long-term investing feel more manageable.

Common Misunderstandings About Glide Paths

One misunderstanding is that a glide path guarantees safety. It doesn’t. Even portfolios with a lower stock allocation can lose value, especially during bond market stress or inflationary periods. The goal is risk reduction, not risk elimination.

Another misconception is that age alone should determine the entire portfolio. Age is important, but it isn’t the only factor. Two people of the same age may need very different glide paths depending on their income sources, savings level, health, and retirement goals.

Some investors also assume a glide path should stop at retirement. In reality, many portfolios need to keep evolving after retirement begins, particularly if the investor may need the portfolio to last for 20 or 30 years.

Should You Use a Glide Path in Your Retirement Strategy?

For many retirement savers, the answer is yes. A glide path can provide structure, reduce unnecessary risk near retirement, and make long-term investing easier to manage. It can be especially useful for people who prefer a hands-off approach or want a retirement portfolio that adjusts over time without constant manual decisions.

Still, the best glide path is one that matches your full financial picture. Investors shouldn’t choose a strategy based only on age or a fund label. It’s important to consider how the portfolio fits with retirement income sources, withdrawal plans, tax strategy, and personal comfort with risk.

Conclusion

A glide path plays a central role in retirement investing by gradually shifting a portfolio from growth-focused assets toward a more conservative mix as retirement gets closer. That transition can help reduce volatility, manage sequence of returns risk, and better align your investments with changing financial needs over time. Whether it’s built into a target-date fund or used as part of a self-directed portfolio, a thoughtful glide path can bring more structure, discipline, and clarity to long-term retirement planning.