Deciding when to take Social Security is one of the most important and stressful retirement choices Americans face. If you claim too early, you can lock in smaller checks for life. If you wait too long, you may worry you’re missing out on money you could be using now.

Here’s the reality most people don’t hear enough: First, there’s no single “best” age for everyone. Second, the smartest choice depends on your health, income needs, work plans, and how long you expect to rely on Social Security.

This guide breaks down early, full, and delayed Social Security retirement ages in an easy-to-understand way, explains how benefits really change over time, and helps you make a decision that supports both your present and your future.

What Is Social Security Full Retirement Age (FRA)?

Your full retirement age (FRA) is the age at which you’re entitled to receive 100% of your earned Social Security benefit, also known as your primary insurance amount (PIA).

Originally, FRA was 65 for everyone. That changed after Congress passed reforms in 1983 to strengthen Social Security’s finances. Today, your FRA depends entirely on your birth year. For older retirees, FRA is in the mid-60s, while for younger workers it gradually rises to age 67.

Instead of memorizing exact month-by-month schedules, the key takeaway is this:

- If you were born earlier, your FRA is closer to age 66

- If you were born in 1960 or later, your FRA is 67

This is important because FRA is the benchmark Social Security uses to calculate both the permanent reductions for claiming early and the permanent increases for delaying benefits. Every decision about when to start Social Security is measured against this age.

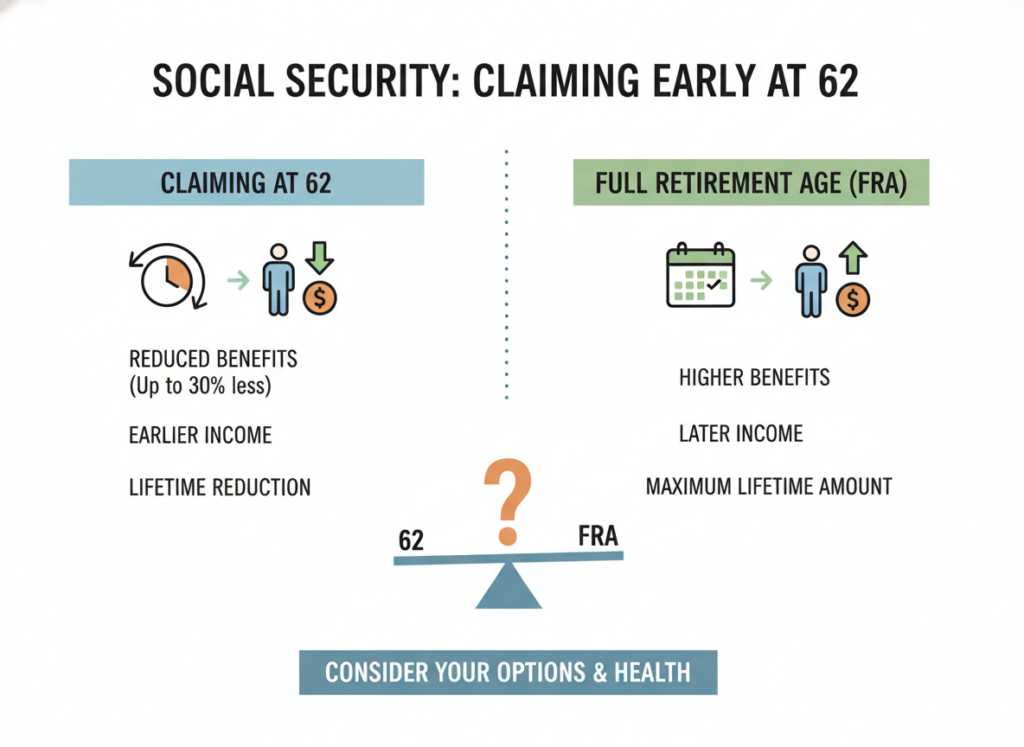

Claiming Social Security Early (Age 62–Before FRA)

You can start receiving Social Security as early as age 62, but that choice comes with a permanent trade-off. When you claim before your full retirement age, your monthly benefit is reduced for life. The earlier you file, the larger the reduction, and these cuts are calculated month by month, not just by year.

For someone whose full retirement age is 67, the impact can be significant. Claiming at 62 typically reduces benefits by about 30%, while claiming at 63 lowers them by roughly 25%, and claiming at 64 cuts them by around 20%. For example, if your full benefit at 67 would be $2,000 per month, starting at 62 could reduce that payment to about $1,400.

Early claiming can still make sense in certain situations. It may be the right move if you need income right away to cover basic living expenses, if health concerns suggest a shorter life expectancy, or if you’re the lower-earning spouse and your partner plans to delay benefits to secure a larger long-term payment for the household.

Claiming at Full Retirement Age (FRA)

Claiming Social Security at your full retirement age means you receive 100% of the benefit you’ve earned. This option often appeals to people who want a balance between getting income now and preserving long-term financial security, plan to keep working part-time, or simply don’t want to lock in a permanently reduced benefit.

Reaching FRA also changes how work income is treated. Before FRA, earning too much can temporarily reduce your Social Security payments. Once you reach full retirement age, those earnings limits disappear entirely. Therefore, FRA is a major milestone in retirement planning.

Delaying Social Security (FRA–Age 70)

Delaying Social Security past your full retirement age earns you delayed retirement credits. These credits add roughly 8% per year and accrue monthly. The increase stops at age 70, so there’s no financial advantage to waiting beyond that point.

For someone with a full retirement age of 67, the boost can be substantial. Claiming at 68 raises benefits to about 108% of the full amount, waiting until 69 increases them to roughly 116%, and delaying until 70 delivers around 124%. In practical terms, a $2,000 monthly benefit at 67 could grow to approximately $2,480 per month by age 70.

Delaying benefits often works best if you expect to live into your 80s or beyond, have other income sources such as savings, a pension, or continued work, or are the higher-earning spouse and want to maximize survivor benefits for your partner later on.

How Social Security Retirement Age Affects Spouses and Survivors

Your Social Security claiming decision doesn’t just affect you. Spousal benefits are tied to full retirement age, and survivor benefits are based on what the deceased spouse was receiving at the time of death. Delaying benefits can significantly increase the income a surviving spouse receives, which is why coordination is especially important for married couples.

Social Security, Work, and Earnings Limits

If you claim Social Security before reaching full retirement age and continue working, your benefits may be temporarily reduced if your earnings exceed the annual limit. However, those withheld benefits aren’t lost. Once you reach full retirement age, the earnings limit disappears, and your benefit is recalculated to account for the amounts that were previously withheld. The key mindset shift is this: continuing to work doesn’t “waste” your Social Security benefits. In many cases, it actually increases what you receive over time.

Taxes on Social Security Benefits

Many retirees are caught off guard to discover that Social Security benefits aren’t always tax-free. In fact, up to 85% of your benefits may be subject to federal income tax, depending on your combined income, not just the amount you receive from Social Security. Combined income includes your adjusted gross income (AGI), any nontaxable interest, and half of your Social Security benefits. Because these factors can change based on when you claim benefits and how long you continue working or drawing from other income sources, the timing of your Social Security decision can influence your tax bill for years.

Social Security’s Future: Should You Be Worried?

You’ve probably heard alarming headlines about Social Security “running out of money,” but the reality is more nuanced. Current projections show the trust funds facing shortfalls in the mid-2030s, not a complete shutdown. Even without changes, ongoing payroll taxes would still cover roughly 75% to 80% of scheduled benefits. Historically, Congress has stepped in before major reductions took effect, adjusting taxes, benefits, or both. While uncertainty is real, Social Security isn’t disappearing, and smart retirement planning is about building flexibility and options, not rushing to claim benefits early out of fear.

How to Choose the Right Social Security Retirement Age

Before choosing when to claim Social Security, it helps to step back and evaluate your personal situation. Ask yourself whether you truly need the income right away or if you can afford to wait for a higher benefit later. Consider your health and family history and think about your work plans as well. If you’re married, factor in how your decision affects spousal or survivor benefits, not just your own check. Finally, look at the tax side: claiming earlier or later can influence how much of your Social Security is taxed. There’s no one-size-fits-all answer, but asking the right questions leads to a smarter, more confident decision.

Quick Decision Guide

Consider claiming early if:

- Cash flow is tight

- Health concerns limit longevity

- You lack other income sources

Consider FRA if:

- You want balance and flexibility

- You’re still working part-time

- You prefer stability over optimization

Consider delaying to 70 if:

- You’re healthy and expect a long retirement

- You’re the higher earner in a couple

- You want maximum guaranteed income later in life

Final Takeaway: Social Security Is a Planning Tool, Not a Deadline

Your Social Security retirement age is a lever that shapes your income for the rest of your life. The goal is to build income you won’t outlive, reduce stress, and protect the people who depend on you.

If you’re unsure, the smartest next step is to run multiple scenarios, such as early, full, and delayed, and see how each one fits your real life. A thoughtful decision today can mean decades of greater financial confidence tomorrow.