Planning for retirement can feel overwhelming, especially when you’re trying to balance investing, risk, and changing market conditions over time. Target-date funds are designed to make that process simpler by offering a diversified, age-based investment strategy that becomes more conservative as retirement gets closer. For many long-term investors, especially those saving through workplace retirement plans, they can provide a practical and low-maintenance way to stay invested.

What Is a Target-Date Fund?

A target-date fund is a professionally managed mutual fund built around an expected retirement year. The year in the fund’s name, such as 2040, 2050, or 2065, generally reflects when an investor plans to retire and start using the money.

These funds are often called all-in-one investments because they usually hold a mix of stocks, bonds, and sometimes cash or short-term assets in a single portfolio. Instead of requiring investors to build and rebalance their own retirement allocation, the fund manager adjusts the mix over time.

In general, a target-date fund with a later retirement year holds a larger share of stocks because the investor has more time to ride out market swings. A fund with an earlier retirement year usually holds more bonds and other conservative investments to reduce volatility. This built-in shift is one of the main reasons target-date funds are widely used in 401(k) plans and other retirement accounts.

How Target-Date Funds Work

The core feature of a target-date fund is its glide path. A glide path is the schedule the fund follows as it gradually changes from a growth-focused portfolio to a more conservative one.

Early in an investor’s career, the fund typically emphasizes stocks because long time horizons support more growth exposure. As the target year approaches, the fund increases its bond allocation to help reduce risk. After the target date, some funds continue getting more conservative, while others level off. This means investors don’t have to keep adjusting their holdings every few years. The fund handles that automatically.

For example, someone in their early 30s saving for retirement around 2060 might choose a 2060 target-date fund. That fund may start with a high stock allocation. Over the next few decades, the fund slowly reduces stock exposure and adds more fixed-income investments. By retirement, the portfolio is generally more focused on preserving capital and generating steadier returns.

Even though the process is automatic, target-date funds aren’t identical. Two funds with the same retirement year can have different stock allocations, different fees, and different levels of risk. That’s why it’s important to look beyond the year in the name.

Key Benefits of Target-Date Funds

Target-date funds have become popular because they solve several common investing challenges at once.

Simple Portfolio Management

One of the biggest advantages is simplicity. Investors don’t need to choose multiple funds, decide how much to place in each one, or rebalance the account manually. For people who don’t want to actively manage a retirement portfolio, this can be a major benefit.

Built-In Diversification

Most target-date funds spread money across many investments. That usually includes large-cap stocks, small-cap stocks, international stocks, government bonds, and corporate bonds. This kind of diversification can help reduce the impact of poor performance in one area of the market.

Automatic Risk Adjustment

Many investors struggle with knowing when to reduce risk. A target-date fund does that on a preset schedule. As retirement gets closer, the portfolio generally becomes more conservative without requiring the investor to take action.

Helpful for Long-Term Discipline

A hands-off structure can also support better investor behavior. People sometimes panic during market declines or chase returns during bull markets. Because target-date funds are designed for long-term retirement saving, they can help investors stay focused on their goal instead of reacting emotionally to short-term market moves.

Convenient for Workplace Retirement Plans

In the United States, target-date funds are commonly offered in 401(k)s, 403(b)s, and similar employer-sponsored plans. They’re often used by default for participants who don’t make their own investment selections. That convenience makes them especially attractive for new investors or busy workers who want a straightforward option.

Potential Drawbacks to Know Before Investing

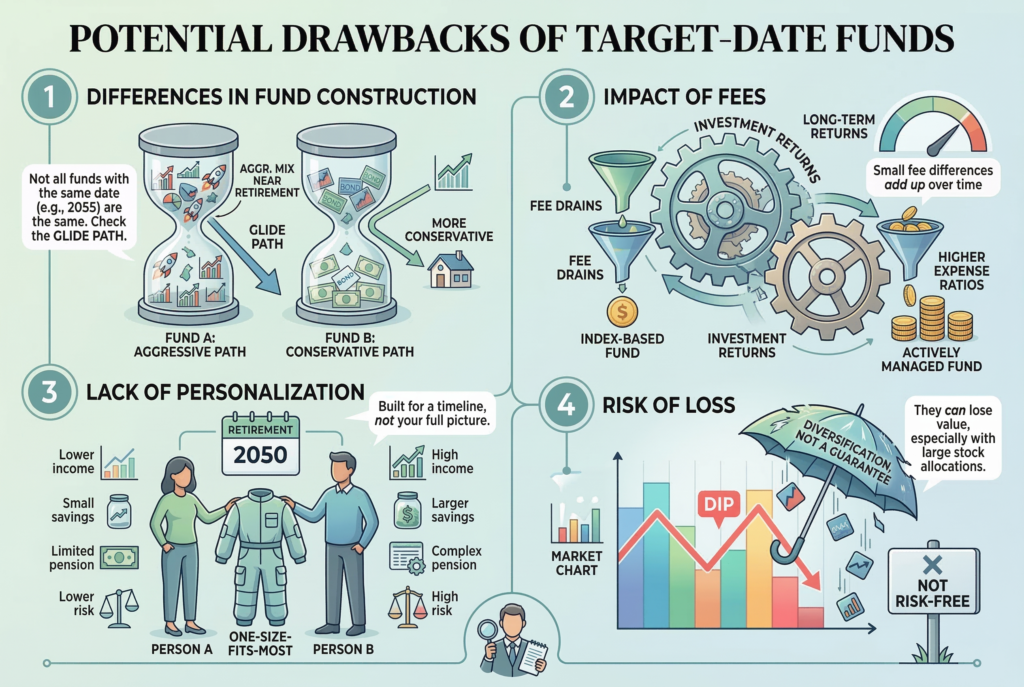

Although target-date funds are convenient, they aren’t the right fit for everyone in every situation. One concern is that investors may assume all funds with the same target year are basically the same. They aren’t. One 2055 fund might still hold a relatively aggressive mix near retirement, while another may be noticeably more conservative. Fund companies build their glide paths differently.

Fees also matter. Some target-date funds are low-cost index-based products, while others are actively managed and may charge higher expense ratios. In the long run, even small fee differences can reduce long-term returns. Another issue is personalization. A target-date fund is built around a general retirement timeline, not your full financial picture.

Two people planning to retire in 2050 may have very different incomes, savings levels, pensions, risk tolerance, or goals. A one-size-fits-most solution may not perfectly match either person. Investors should also remember that target-date funds can still lose value, especially those with a significant stock allocation. They may be diversified, but they aren’t guaranteed or risk-free.

Who Should Invest in a Target-Date Fund?

Target-date funds can be a strong option for several types of investors. They often make sense for beginning investors who want retirement exposure without having to learn how to build a multi-fund portfolio right away. They can also work well for people who prefer a set-it-and-forget-it approach and don’t want to rebalance regularly.

They’re especially useful for workers contributing to a 401(k) or IRA who want broad diversification in a single fund. For someone with a long-term retirement goal and limited time to manage investments, a target-date fund can be a practical starting point. These funds may also appeal to investors who know they’re unlikely to stay on top of portfolio maintenance. In that case, automation can be better than having a neglected or poorly allocated account.

That said, target-date funds may be less appealing for experienced investors who want more control over tax strategy, asset allocation, or withdrawal planning. Someone who prefers customizing domestic and international exposure, bond duration, or retirement income positioning may want to build a portfolio independently instead.

How to Choose the Right Target-Date Fund

Choosing a target-date fund starts with estimating when you’ll likely retire. That gives you a rough idea of which year to consider. Still, the year on the label shouldn’t be your only factor.

Look closely at the fund’s asset allocation. How much is in stocks today? How quickly does the fund become more conservative? Does that match your comfort level with risk? Next, review the expense ratio. Lower costs can make a meaningful difference over decades, especially in retirement accounts where long-term compounding matters.

It’s also smart to check whether the fund uses mostly index funds or active management, and whether it continues changing after the target year. Some investors want a portfolio that stays fairly growth-oriented in retirement, while others prefer a faster shift toward capital preservation.

Finally, consider how the fund fits within your broader retirement strategy. If most of your money is already in one target-date fund, adding other funds could create overlap or unintentionally change your risk level.

Target-Date Funds vs. Building Your Own Portfolio

A target-date fund offers convenience, professional management, and automatic rebalancing. Building your own portfolio offers more flexibility and customization.

Neither approach is universally better. The right choice depends on how involved you want to be and how confident you are managing investments over time.

A self-directed portfolio may be better for investors who understand allocation strategy and want tighter control over taxes, rebalancing, and income planning. But for many retirement savers, especially those focused on consistency and simplicity, a target-date fund can be a smart and efficient solution.

In other words, the best retirement investment approach isn’t always the most complex one. Sometimes a simpler option is more effective because it’s easier to stick with over the long run.

Conclusion

Target-date funds are designed to simplify retirement investing by combining diversification, professional management, and automatic risk adjustment in one fund. They can be especially useful for people saving through a 401(k) or IRA, new investors, and anyone who wants a more hands-off strategy.

Still, convenience doesn’t mean every target-date fund is equally strong. Investors should compare fees, glide paths, and overall asset allocation before choosing one. When used thoughtfully, a target-date fund can offer a clear, practical path toward long-term retirement saving without requiring constant portfolio decisions.