When it comes to personal finance and investment, understanding what a “fund” is can be a game-changer. Funds are a powerful way to pool resources and access diversified portfolios managed by professionals. They allow individuals, from beginners to seasoned investors, to grow wealth over time without the need for a high level of expertise or large capital.

In this article, we’ll explore what funds are, break down the different types of funds, explain how they work, and help you determine how to leverage them for your financial goals.

What Is a Fund?

At its core, a fund is a pool of money that is collected and managed to invest in various assets, such as stocks, bonds, real estate, or other securities. Instead of investing alone, people contribute money to a fund, allowing them to collectively invest in a diverse portfolio, which can spread out the risks of investing in individual assets.

Funds are typically managed by professional fund managers who use their expertise to select and manage the assets within the fund. This allows investors, especially beginners, to have access to professional management and diversified investments without needing substantial capital or time commitment.

Investing in a fund can be much more cost-effective than buying individual stocks, as the management fees are spread out among all investors.

Types of Funds

1. Mutual Funds

Mutual funds pool money from many investors to purchase a diversified set of stocks, bonds, or other securities. Investors buy shares in the fund, and the total value of the fund rises or falls based on the performance of the assets in the portfolio.

Mutual funds can be actively managed, where fund managers make decisions on which assets to buy and sell, or passively managed, where the fund simply tracks an index like the S&P 500. For those looking for long-term growth, mutual funds are an excellent choice, especially for retirement planning.

2. Exchange-Traded Funds (ETFs)

ETFs are similar to mutual funds in that they pool money to invest in various assets. The key difference is that ETFs trade like stocks, meaning they can be bought and sold throughout the day on the stock exchange. Unlike mutual funds, which are priced at the end of each trading day, ETFs have a constantly fluctuating price, giving investors flexibility in timing their trades. ETFs typically have lower fees than mutual funds and are often considered an excellent option for investors who want broad market exposure but prefer a more hands-off investment.

3. Index Funds

Index funds are a specific type of passively managed mutual fund designed to replicate the performance of a particular market index, such as the Dow Jones Industrial Average or the S&P 500. These funds invest in the same companies that make up the index, offering broad exposure to the stock market at a low cost.

The appeal of index funds lies in their low expense ratios and consistent performance over the long term, making them a solid choice for investors looking for stability and growth without high management fees.

4. Hedge Funds

Hedge funds are actively managed funds designed to generate high returns, often using complex strategies such as leverage, short selling, or derivatives. Hedge funds are typically only available to high-net-worth individuals and institutional investors, due to their high minimum investment requirements and risks involved.

Although hedge funds have the potential for high returns, they’re often much more speculative and come with higher fees compared to mutual funds and ETFs. They’re suited for experienced investors who can tolerate a high level of risk.

5. Target-Date Funds

Target-date funds are designed to automatically adjust their asset allocation based on a target date, such as retirement. These funds gradually become more conservative as the target date approaches, reducing exposure to high-risk assets like stocks and increasing exposure to low-risk assets like bonds.

Target-date funds are ideal for retirement planning because they require minimal effort once you’ve selected a fund. They’re often included in employer-sponsored retirement plans, making them a convenient option for employees.

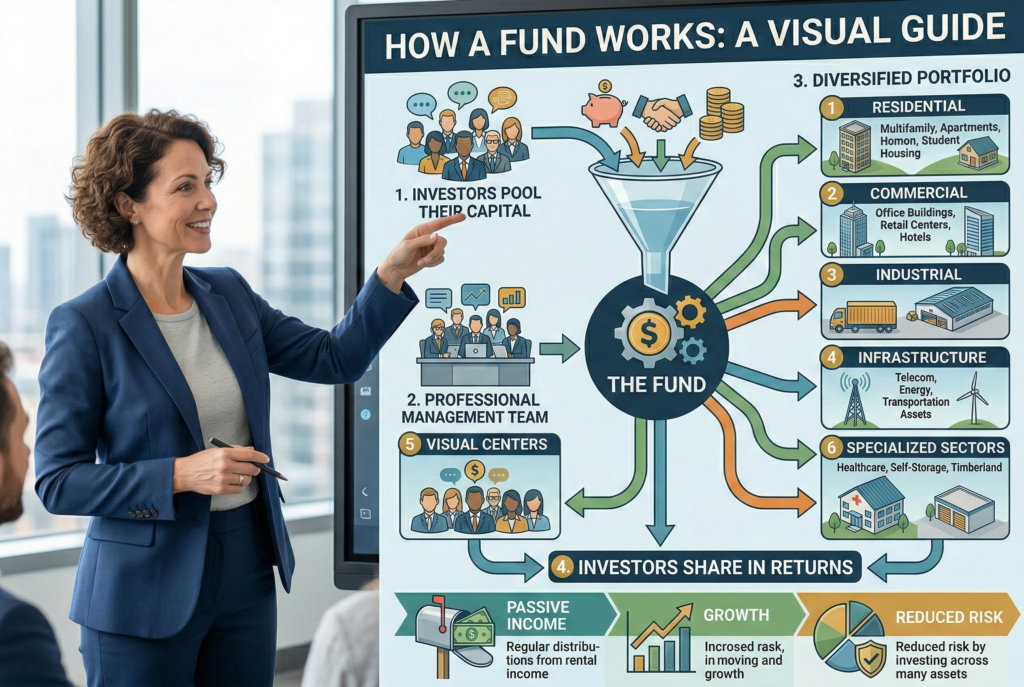

6. Real Estate Investment Funds

Real estate funds allow you to invest in real estate without actually buying property. These funds pool investors’ money to invest in residential, commercial, or industrial properties. Real estate investment funds offer the potential for steady income through rental properties and can also provide capital appreciation if property values increase.

7. Money Market Funds

Money market funds are low-risk, short-term investment funds that typically invest in high-quality, short-term debt instruments such as government securities, certificates of deposit (CDs), or commercial paper. These funds are designed to offer liquidity while providing a modest return. Money market funds are ideal for investors looking for a safe place to park their money with little risk, especially if they need quick access to cash.

8. Bond Funds

Bond funds invest in fixed-income securities (such as government, corporate, or municipal bonds) to generate steady income through interest payments. These funds offer a more stable, conservative investment option compared to stocks but may have lower returns. Bond funds are typically preferred by investors seeking regular income or those who are closer to retirement and want to reduce risk in their portfolios.

How Funds Work

Funds work by pooling together the money of multiple investors. Once pooled, the fund manager invests that money in assets that align with the fund’s investment strategy. The goal of a fund is to make investment decisions that will maximize returns over time while minimizing risk.

When you invest in a fund, you buy shares or units of that fund. Your returns depend on the performance of the assets the fund holds. If the fund performs well, the value of your shares increases, and you earn a return. If the fund performs poorly, the value of your shares decreases.

The key advantage of funds is diversification. Instead of investing in a few individual assets, funds typically invest in a variety of stocks, bonds, and other securities, which helps spread risk. For example, if one stock in the fund loses value, the impact on your investment is minimized by other stocks that may perform better.

Key Benefits of Investing in Funds

- Diversification: By pooling your money with others, funds allow you to invest in a variety of assets, helping you manage risk more effectively.

- Professional management: Funds are managed by professionals, which takes the burden of day-to-day investment decisions off your shoulders.

- Accessibility: Funds often have low minimum investment requirements, allowing even those with limited funds to get started with investing.

- Liquidity: Most funds allow you to buy and sell shares easily, making it simple to access your money when needed.

How to Choose the Right Fund for Your Goals

Choosing the right fund for your goals depends on your financial objectives, risk tolerance, and investment horizon. If you’re looking for growth and are comfortable with some risk, a mutual fund or stock-based fund may be right for you. If you prefer a more conservative approach, consider a bond fund or money market fund.

Always research the fund’s strategy, fees, and performance history before making a decision. It’s essential to ensure the fund aligns with your financial goals and risk profile.

Final Thoughts

Understanding what a fund is and how it works is essential for making informed investment decisions. Whether you choose a mutual fund, ETFs, or real estate investment funds, the key is to select a fund that fits your financial goals, risk tolerance, and time horizon.

By carefully evaluating the various types of funds available, you can build a diversified portfolio that suits your needs and helps you achieve your long-term financial objectives.

Related Articles

Investment Funds Explained: What They Are, How They Work, and Key Benefits for Investors