Saving for college can feel intimidating, especially when tuition, housing, and other education costs keep rising. A 529 plan is one of the most widely used tools for education savings because it offers tax advantages, flexible beneficiary rules, and the ability to invest for future qualified expenses. For families in the United States, understanding how a 529 plan works can make it easier to build a practical college savings strategy without overcomplicating the process.

What a 529 Plan Is

A 529 plan is a tax-advantaged education savings account designed to help pay for qualified education expenses for a named beneficiary. The IRS treats 529 plans as qualified tuition programs, and earnings in the account can grow tax-free when withdrawals are used for eligible education costs.

There are two broad forms of 529 plans: education savings plans and prepaid tuition plans. Education savings plans let you invest contributions in a portfolio of options that can later be used for qualified expenses. Prepaid tuition plans generally allow families to lock in tuition costs at participating schools, though availability and portability can be more limited. For most families, the education savings version is the more familiar and flexible option.

How a 529 Plan Works

A 529 plan works by allowing an account owner to contribute money for a beneficiary, usually a child, grandchild, or other family member. The account owner stays in control of the funds and decides when withdrawals are made. The money is typically invested in options such as age-based portfolios, target enrollment portfolios, or static fund selections, depending on the plan.

The main tax benefit is that investment earnings can grow free from federal tax, and withdrawals are also federally tax-free when used for qualified education expenses. Contributions aren’t deductible on your federal income tax return, but many states offer a state tax deduction or state tax credit for eligible contributions.

That means a 529 plan doesn’t reduce federal taxes upfront, but it can still create meaningful long-term tax savings if the money stays invested and is used correctly.

What 529 Plan Money Can Pay For

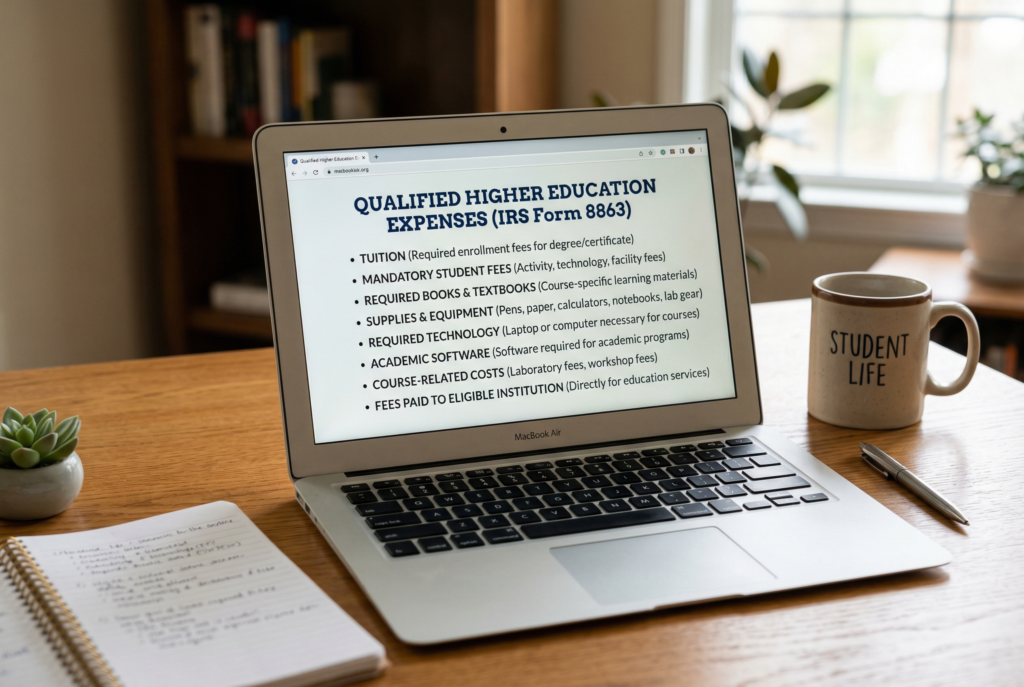

A major reason 529 plans are so popular is that qualified withdrawals can cover more than just tuition. Under IRS rules, qualified higher education expenses can include tuition, fees, books, supplies, and certain room and board costs for eligible students. Computers, peripheral equipment, software, and internet access may also qualify when used primarily by the beneficiary during enrollment.

529 plans can also be used for K-12 tuition, although there’s an annual cap. The IRS currently states that qualified elementary or secondary school tuition is limited to $20,000 per year from all of the beneficiary’s qualified tuition programs. Because the rules are specific, it’s important to match withdrawals carefully to qualified expenses in the same tax year.

Key Tax Benefits of a 529 Plan

Tax Treatment

The biggest advantage of a 529 college savings plan is the tax treatment. Earnings can grow free from federal tax, and qualified withdrawals are also federally tax-free. Over many years, that can make a meaningful difference compared with saving in a regular taxable investment account.

State Level

Another major benefit is at the state level. More than 30 states offer residents a state income tax deduction or tax credit for 529 plan contributions, although the rules vary widely. Some states require you to use the home-state plan for the tax break, while others allow deductions for contributions to any state’s plan. This means the best 529 plan for you isn’t always the one with the best investment menu on paper. In some cases, the home-state tax benefit can be valuable enough to influence the decision.

Why Families Use 529 Plans

A 529 plan can work well because it combines tax-free growth, flexible account ownership, and relatively high contribution capacity compared with many other education savings options. Unlike some custodial accounts, the account owner keeps control over the money, which can be useful if plans change or if the beneficiary doesn’t end up needing all the funds.

Another strength is flexibility around beneficiaries. IRS guidance allows account owners to change the beneficiary to another qualifying family member in many situations, which can help avoid waste if one child doesn’t use the full balance. That flexibility makes 529 plans more practical for families who want to start saving early but can’t predict every future education decision.

Smart Ways to Save for College With a 529 Plan

One of the smartest ways to use a 529 plan is to start early, even if the initial contributions are modest. Because earnings compound over time, years in the market often matter more than trying to contribute large amounts later. The IRS notes that earnings are usually a function of time, which is why earlier funding can be more useful than waiting until college is close.

Another smart move is to automate contributions. Regular monthly deposits can make saving more manageable and reduce the pressure to come up with large lump sums. This also helps smooth out investing over time. It’s also wise to check whether your state offers a tax deduction or credit before selecting a plan. In many cases, using your home-state plan may provide an immediate state tax benefit on top of the federal tax advantages.

Families should also think carefully about investment choices. Many plans offer age-based portfolios that automatically become more conservative as college approaches. That can help reduce risk as the time to use the money gets closer. The SEC’s recent investor bulletin encourages savers to review plan investment options, fees, and age-based features before opening an account.

How to Choose the Right 529 Plan

Choosing the right 529 plan usually comes down to three areas: tax benefits, investment options, and fees. Start with your state tax rules. If your state offers a meaningful deduction or credit, that may make the in-state plan especially attractive. If your state offers no tax break, or if the in-state plan is weak, an out-of-state plan may be worth considering.

Then review investment choices. A strong plan should offer diversified options, reasonable risk levels, and age-based portfolios if you want a more hands-off approach. The SEC also advises comparing fees carefully, because high expenses can reduce long-term returns. Finally, look at plan usability. Easy online management, simple beneficiary changes, and clear withdrawal procedures can make a difference over many years.

Potential Drawbacks to Understand

A 529 plan is powerful, but it isn’t perfect. The main limitation is that the strongest tax benefits apply only when withdrawals are used for qualified education expenses. If money is withdrawn for nonqualified purposes, the earnings portion may be subject to income tax and an additional federal penalty.

Investment risk is another factor. If the beneficiary is close to college age and the portfolio is too aggressive, a market downturn could reduce the account value at the wrong time. That’s why investment allocation matters just as much as account selection.

It’s also important not to overfund the account without a plan. While beneficiary changes add flexibility, families should still balance 529 savings against retirement needs, emergency savings, and other financial priorities.

Conclusion

A 529 plan can be one of the most effective ways to save for education because it combines tax-free growth, tax-free qualified withdrawals, flexible beneficiary rules, and potential state tax benefits. It can be used for a range of education costs, including eligible college expenses and, within limits, K-12 tuition.

The best approach is usually simple: start early, contribute consistently, compare plans carefully, and pay attention to fees and state tax rules. When used thoughtfully, a 529 plan can make college savings more manageable and help families keep more of their money working toward education goals.