: How It Works, Eligibility, and How to Maximize Your Refund")

The Earned Income Tax Credit (EITC) is one of the most significant tax benefits for low- and moderate-income individuals and families. It’s designed to provide financial relief to working people by reducing the amount of tax owed or even providing a refund if the credit exceeds the tax liability. Whether you’re a first-time filer or looking to maximize your refund, understanding how the EITC works and how to qualify is key to benefiting from this powerful credit. This guide breaks down everything you need to know about the EITC, including eligibility, how it works, and tips to make the most of it.

What is the Earned Income Tax Credit (EITC)?

The Earned Income Tax Credit (EITC) is a refundable tax credit, meaning that it can reduce your tax bill to zero and, if the credit exceeds the amount of taxes you owe, the IRS will refund you the remaining balance. This is particularly beneficial for families and individuals with lower incomes. The more you earn (within the eligibility limits), and the more children you have, the larger your potential credit.

The EITC differs from tax deductions, which lower your taxable income. The EITC directly reduces your tax liability, making it a dollar-for-dollar reduction. This means that if you qualify for a large EITC, it can directly reduce the amount of taxes you owe, and potentially provide you with a refund.

How Does the EITC Work?

The EITC is designed to increase as your earned income rises, but only up to a certain limit. The amount of the EITC you qualify for depends on several factors:

- Your earned income: The lower your income, the larger your credit will be. The credit increases as your income rises, but only until it reaches a peak.

- Family size: Families with more qualifying children are eligible for a larger credit. The credit peaks for families with three or more children, but you can still qualify with one or two children.

- Filing status: Whether you file as single, head of household, or married filing jointly will also affect your eligibility and the size of your credit.

The EITC is refundable, meaning that if your credit exceeds your tax liability, you’ll receive the difference as a refund. This makes it especially helpful for low-income households where tax liability may be low or nonexistent.

Who is Eligible for the EITC?

1. Earned Income

To qualify for the EITC, you must have earned income. This can include wages, salary, self-employment income, and tips. It doesn’t include income from investments, such as interest, dividends, or capital gains. Therefore, individuals with investment income above a certain threshold may not qualify for the credit.

2. Income Limits

The EITC has income limits that depend on your filing status and the number of qualifying children you have. The higher your income and fewer qualifying children, the smaller your potential credit. If your income exceeds the limits set by the IRS, your credit will be phased out.

Income limits are adjusted each year to keep up with inflation. Generally, single filers, heads of household, and married couples filing jointly with children can receive the largest credits, but even those without children can still qualify if their income is within the limits.

3. Qualifying Children

If you have children, they must meet specific criteria to qualify for the EITC. The child must:

- Be under 17 at the end of the tax year.

- Be a U.S. citizen or resident alien.

- Live with you for more than half of the year and be your biological child, adopted child, stepchild, or even a grandchild or sibling in certain cases.

Families with more children are eligible for larger credits, as the credit is designed to provide more support for families with greater needs.

4. Filing Status

To claim the EITC, you must file as single, head of household, or married filing jointly. Married individuals who file separately are not eligible for the EITC.

5. Social Security Number (SSN)

Both you and any qualifying children must have a valid SSN. The EITC is designed to help those working in the U.S. legally, so valid documentation is crucial for claiming this benefit.

How Much is the Earned Income Tax Credit Worth?

The EITC amount varies based on your earned income, filing status, and family size. The general formula works like this: the more qualifying children you have and the lower your income, the larger your EITC will be.

For the EITC, the credit typically ranges from a few hundred dollars for individuals with no children to over $8,000 for families with three or more children. If you are eligible for the credit and the amount exceeds your tax liability, you will receive the remaining credit as a refund.

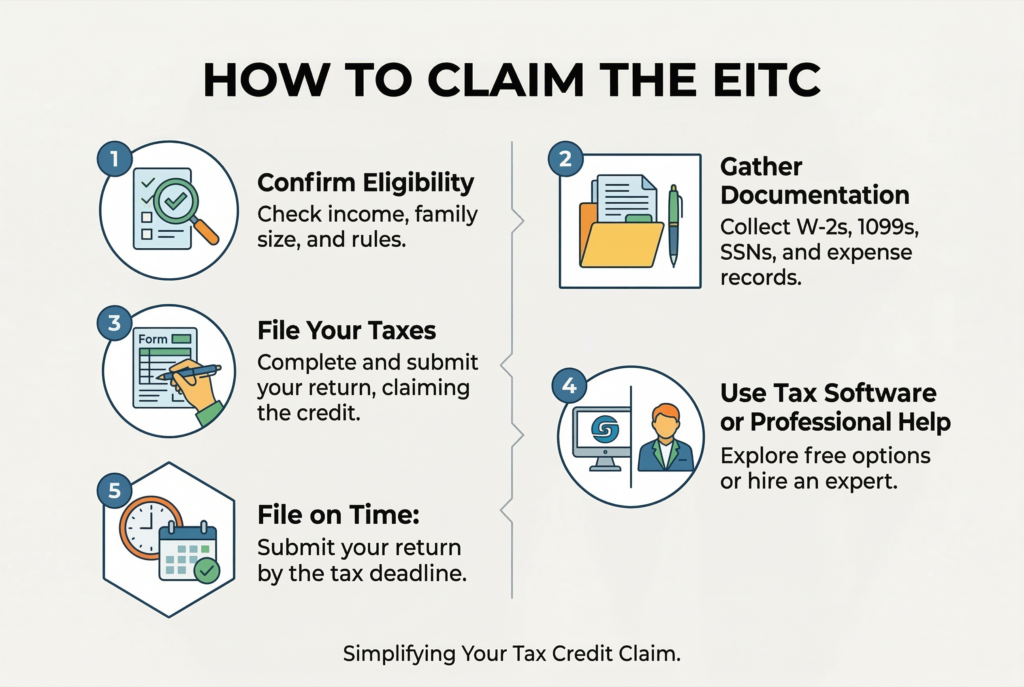

How to Claim the EITC

Step 1. Confirm Eligibility

Check your income, family size, and filing status to ensure you meet the eligibility requirements. The IRS website and tax software tools provide eligibility calculators that can help you verify if you qualify for the credit.

Step 2. Gather Documentation

Before filing, gather the necessary documentation, including:

- W-2 and 1099 forms that show your earned income.

- Social Security Numbers (SSN) for you and your qualifying children.

- Proof of residency for your children, such as school records or medical records.

Step 3. File Your Taxes

To claim the EITC, you must file your taxes using Form 1040. If you’re claiming the credit for children, you’ll also need to complete Schedule EIC, which reports the number of children and their relationship to you.

Step 4. Use Tax Software or Professional Help

If you’re unsure about how to claim the EITC, use reliable tax software or consider getting help from a tax professional. Software like TurboTax or H&R Block will guide you through the process and ensure you claim the maximum credit possible.

Step 5. File on Time

Make sure to file your tax return on time to avoid delays and ensure you receive your refund promptly. Filing early, especially electronically, can help speed up the process. Direct deposit is the fastest way to receive your refund.

Tips to Maximize Your EITC

File Early

Filing your taxes as soon as possible ensures you receive your EITC quickly. The IRS processes most e-filed returns in about 21 days, and direct deposit guarantees faster delivery of your refund.

Use Retirement Accounts

If you’re near the income phase-out limits, consider contributing to a 401(k) or IRA to reduce your taxable income. This can help you stay under the limits and qualify for a larger credit.

Explore Other Tax Benefits

The EITC is just one of many credits and deductions you may qualify for. Be sure to check for other credits, such as the Child Tax Credit or Saver’s Credit, which can further reduce your tax burden.

Conclusion

The Earned Income Tax Credit (EITC) is a powerful tool for working families and individuals with lower incomes. By understanding how it works, confirming your eligibility, and following the correct steps to claim it, you can reduce your tax liability and receive a refund that could significantly improve your financial situation.

To ensure you receive the full benefit of the EITC, file your taxes on time, gather the correct documentation, and consider using tax software or consulting a professional to help navigate the process. Don’t miss out on this essential credit, check your eligibility today and maximize your refund in 2026!