Tax season has a funny way of sneaking up on you. One minute you’re cleaning out your email inbox, the next you’re staring at your tax software wondering, “Is it standard or itemized?”

If that moment sounds familiar, you aren’t alone. Choosing between standard vs. itemized deductions is one of the most common and surprisingly stressful decisions that U.S. taxpayers face each year. If you pick the right one, you could keep thousands of dollars in your pocket. Pick the wrong one, and you might leave money on the table without realizing it.

What Tax Deductions Really Do

A tax deduction lowers the amount of your income that’s subject to tax. Lower taxable income usually means a smaller tax bill, or a bigger refund. When it comes to federal taxes, you generally choose one of two paths: take the standard deduction or itemize deductions by listing specific expenses. You can’t do both. The goal is simple: pick the option that gives you the bigger deduction.

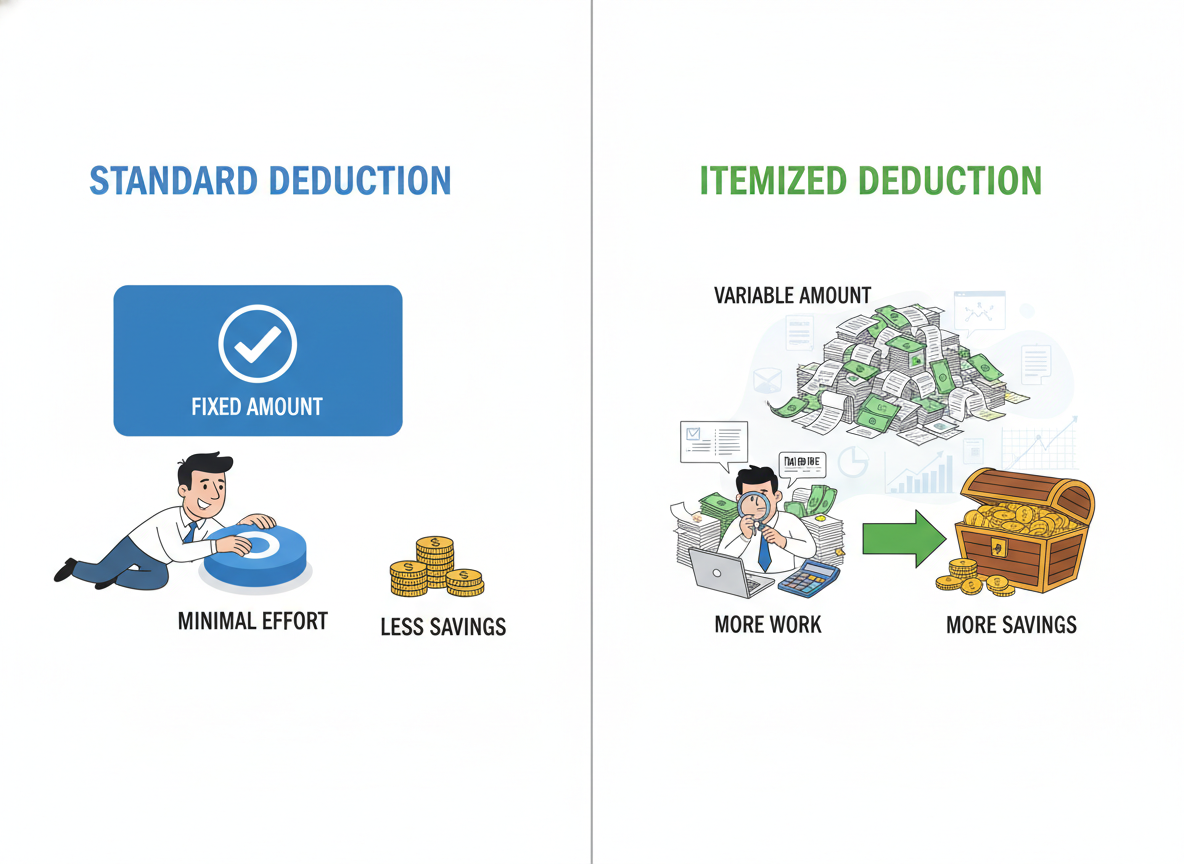

What Is the Standard Deduction?

The standard deduction is a fixed dollar amount set by the IRS each year. Instead of receipts, spreadsheets, or a shoebox full of paperwork, you just qualify based on your filing status.

Why the Standard Deduction Is So Popular

There’s a reason nearly 9 out of 10 taxpayers choose it: the standard deduction is simple because there’s no need to track expenses, fast because it requires fewer forms and decisions, and predictable since the amount is set in advance.

Who Usually Benefits Most From the Standard Deduction?

The standard deduction often makes the most sense if you rent instead of own, don’t have high medical expenses, make modest charitable donations, and prefer a low-stress filing experience. When deductible expenses are relatively low, itemizing usually adds extra work without increasing your tax savings.

What is Itemized Deductions?

Choosing itemized deductions means listing specific IRS-approved expenses on Schedule A instead of taking the flat standard deduction. This approach takes more time and recordkeeping, but in some cases the extra effort can result in meaningful tax savings.

Common itemized deductions include mortgage interest on a primary or secondary home, state and local taxes (SALT) such as income and property taxes, charitable donations to qualified organizations, and medical or dental expenses that exceed 7.5% of your adjusted gross income (AGI). If the total of these expenses is higher than your standard deduction, itemizing could reduce your taxable income more.

Standard vs. Itemized Deductions: The Core Difference

At the heart of this decision is a simple comparison: the standard deduction offers a fixed amount with minimal effort, while itemized deductions vary based on your expenses and require more work but can lead to greater savings. The key rule to remember is straightforward: only itemize if your total itemized deductions exceed your standard deduction.

Standard vs. Itemized Deductions: A Side-by-Side Comparison

| Feature | Standard deduction | Itemized deduction |

|---|---|---|

| How it works | A fixed dollar amount set by the IRS | You list and total specific qualifying expenses |

| Paperwork required | Minimal | Detailed records and receipts needed |

| Time & effort | Fast and simple | More time-consuming |

| Flexibility | Same amount regardless of expenses | Changes based on your actual spending |

| Best for | Renters, simple finances, lower expenses | Homeowners, high medical or tax expenses |

| Common expenses included | None individually | Mortgage interest, State and local tax (SALT), medical, charity |

| Audit risk | Very low | Slightly higher due to documentation |

| Who usually benefits | About 90% of taxpayers | Roughly 10% of taxpayers |

How to use this table: If the right column feels like your life, such as mortgage statements, medical bills, donation receipts, itemizing may be worth the effort. If the left column feels more like you, the standard deduction likely gets you close (or better) with far less stress. Remember to choose the one that keeps more of your money with the least friction.

A Real-World Example

Let’s say you’re single and your standard deduction is $15,750. You total up your potential itemized deductions and find you have $8,500 in mortgage interest, $4,000 in state and local taxes, and $2,000 in charitable donations, for a combined total of $14,500. In that case, the standard deduction clearly wins.

However, if those same expenses added up to $17,000, itemizing would make more sense, even though it requires extra paperwork, because it would reduce your taxable income more than the standard deduction.

When Itemizing Starts to Make Sense

Homeownership Often Changes the Math

Owning a home can tip the scales, especially in the early years of a mortgage when interest payments are higher. Homeowners often itemize because of mortgage interest, property taxes, and combined charitable giving. If you’ve ever opened Form 1098 from your lender and thought, “Wow, that’s a lot of interest,” itemizing may be worth a closer look.

High Medical Expenses Can Push You Over the Edge

Medical costs are deductible only after they exceed 7.5% of your AGI, which rules many people out. But for those who had a rough health year, this can be a big deal.

Charitable Giving Can Be a Quiet Game-Changer

Regular donations, especially in a year when you give more than usual, can push itemized deductions past the standard threshold. Some families even “bunch” charitable donations into one year to make itemizing worthwhile, then take the standard deduction the next year.

A Quick Self-Check: Which Path Are You On?

Ask yourself these questions:

- Do I own a home and pay mortgage interest?

- Did I pay significant state or local taxes?

- Were my medical expenses unusually high this year?

- Did I donate more to charity than I normally do?

If you answered “yes” to more than one, itemizing deserves a serious look. If not, the standard deduction is probably your friend.

Why So Many People Still Take the Standard Deduction

Even when itemizing might save a little more, many taxpayers stick with the standard deduction. And that isn’t always a mistake because it’s time-saving, simple and reduces stress, especially for busy professionals, parents, and anyone already juggling too much.

Practical Tips to Make the Decision Easier

Keep Light Records

You can compare both options quickly instead of guessing by keeping key documents organized, such as mortgage interest statements, year-end charitable donation summaries, and large medical bills, so you can easily total your itemized deductions when tax time comes.

Let the Math Decide

Many people assume itemizing is better, or worse, without checking honestly. But you should consider the number, then compare both totals, choose the higher one, and move on.

The Bottom Line: Bigger Deduction Wins

Choosing between standard vs. itemized deductions isn’t about being “good at taxes.” It’s about making a clear comparison and picking the option that reduces your taxable income the most. These days, you can reevaluate this choice every single year. Your life changes, your expenses change, and your best option can change too.