Being self-employed comes with many rewards, such as flexibility and the potential for business growth, but it also comes with a significant responsibility: managing your taxes.

Understanding self-employment tax is crucial for freelancers, independent contractors, small business owners, and anyone who works for themselves. This tax covers your contributions to Social Security and Medicare, and unlike regular employees, self-employed individuals must pay both the employee and employer portions of these taxes.

In this article, we’ll break down what self-employment tax is, how to calculate it, how to file it, and share strategies to help you save money while staying compliant with the IRS.

What Is Self-Employment Tax?

Self-employment tax is a tax that covers the Social Security and Medicare taxes that would normally be split between an employer and employee. If you’re self-employed, you’re responsible for paying both the employee and employer portions, which equals 15.3% of your net earnings. This tax rate includes 12.4% for Social Security and 2.9% for Medicare. For high-income earners, an additional 0.9% Medicare tax may apply to income over a certain threshold.

In simpler terms, when you’re self-employed, you’re both the employer and the employee. While this gives you more freedom in your work, it also means more responsibility when it comes to handling your taxes. Unlike salaried employees, who only pay the employee portion of these taxes, self-employed individuals must pay both parts.

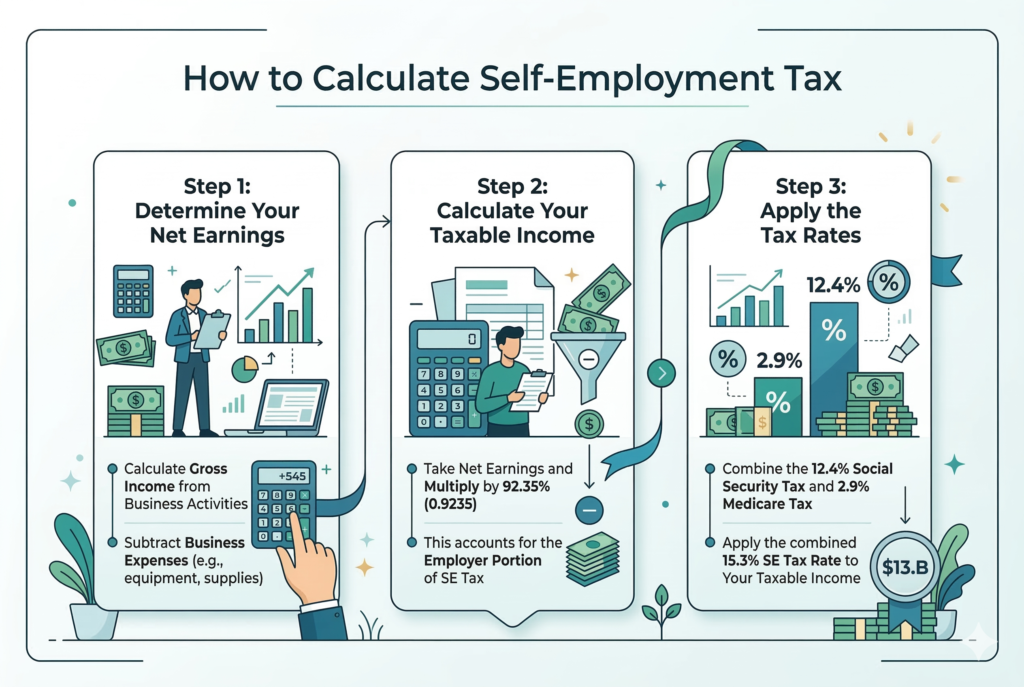

How to Calculate Self-Employment Tax

Calculating self-employment tax is straightforward, but you need to know how to determine your net earnings. Net earnings are your total income from self-employment, minus any allowable business expenses.

Step 1: Determine Your Net Earnings

Start with your total income from self-employment and subtract any eligible business expenses (such as office supplies, travel expenses, and equipment).

Step 2: Calculate Your Taxable Income

Multiply your net earnings by 92.35%. This reduces the amount of income subject to self-employment tax, as the IRS allows you to deduct the “employer” portion of the tax.

Step 3: Apply the Tax Rates

Once you’ve calculated your taxable income, apply the self-employment tax rates: 12.4% for Social Security (up to the annual limit) and 2.9% for Medicare (applies to all income). If your income exceeds a certain threshold, apply an additional 0.9% Medicare tax on income over that amount.

Example: How Self-Employment Tax Is Calculated

Let’s say your net earnings from self-employment in 2026 are $50,000. Here’s how you would calculate your self-employment tax:

- Net earnings: $50,000

- Multiply by 92.35%: $50,000 × 0.9235 = $46,175

- Apply the 12.4% Social Security tax: $46,175 × 12.4% = $5,725.68

- Apply the 2.9% Medicare tax: $46,175 × 2.9% = $1,341.08

- Total self-employment tax: $5,725.68 + $1,341.08 = $7,066.76

How to File Your Self-Employment Taxes

As a self-employed individual, you’ll report your self-employment income and pay your taxes using IRS Form 1040 and Schedule C (Profit or Loss from Business). Schedule SE is also required to calculate and report your self-employment tax.

- Complete Schedule C: This form helps you report your income and deductions from self-employment.

- Fill out Schedule SE: This form is used specifically to calculate and report your self-employment tax.

- File your tax return: Submit your completed Form 1040, Schedule C, and Schedule SE by the April 15th deadline (or later if you file for an extension).

In addition to filing your taxes annually, self-employed individuals must also make quarterly estimated tax payments. These payments are due in April, June, September, and January. Failing to make these payments could result in penalties, so it’s important to stay on top of your quarterly tax obligations.

Tax Deductions for Self-Employed Individuals

Half of Your Self-Employment Tax

You can deduct 50% of your self-employment tax directly from your taxable income, which can significantly lower your overall tax liability. This deduction is an “above-the-line” deduction, meaning it reduces your taxable income, not just your tax liability.

Business Expenses

You can deduct ordinary and necessary business expenses that help you run your business. These expenses include things like office supplies, business-related travel expenses, marketing and advertising costs, software or subscriptions used for work, and equipment and tools.

Health Insurance Premiums

If you’re self-employed, you may also be able to deduct the cost of your health insurance premiums for yourself, your spouse, and your dependents. This is a great way to reduce your taxable income while also ensuring you’re covered for healthcare needs.

Retirement Contributions

Contributing to a Solo 401(k) or SEP IRA can also help reduce your taxable income while saving for retirement. These contributions are typically tax-deductible, and self-employed individuals can set aside a significant portion of their income for retirement. The contribution limits for 2026 are $23,000 for a Solo 401(k), with an additional $7,500 catch-up contribution for those aged 50 or older.

Home Office Deduction

If you work from home, you may qualify for the home office deduction. This allows you to deduct a portion of your home expenses, such as rent or mortgage interest, utilities, and internet, based on the percentage of your home used for business purposes.

Tips to Save Money on Self-Employment Tax

Keep Track of All Business Expenses

Keep detailed records of all your business expenses. The more expenses you can deduct, the less income you’ll be taxed on. Make sure to track every receipt and document your business-related purchases.

Contribute to Retirement Accounts

Contribute as much as you can to a Solo 401(k) or SEP IRA. This reduces your taxable income while helping you save for retirement.

Pay Estimated Taxes on Time

Avoid penalties by making quarterly estimated tax payments. Set aside money regularly for taxes so you aren’t hit with a large bill at the end of the year.

Consider Incorporating

If your business is growing, consider incorporating as an S-corporation to reduce your self-employment tax liability. By paying yourself a reasonable salary, you can reduce the amount subject to self-employment tax.

Conclusion: Take Control of Your Taxes

Self-employment tax can seem like a daunting responsibility, but understanding how it works and taking proactive steps to minimize your liability can help you keep more of your hard-earned money. By staying organized, taking advantage of tax deductions, and making quarterly estimated tax payments, you can confidently manage your tax responsibilities and reduce your overall tax burden.

Remember, if your situation is complex or you’re unsure of your tax obligations, it’s always a good idea to consult with a tax professional. With the right strategies and planning, you can maximize your savings and ensure you’re making the most of your self-employment tax deductions.