A savings account is one of the simplest and most dependable tools for building financial stability. It gives you a secure place to keep money you don’t plan to spend right away while earning interest over time. Whether you’re starting an emergency fund, setting aside money for a major purchase, or simply trying to separate spending from saving, the right savings account can make your financial life more organized and more resilient.

Why a Savings Account Matters

A savings account plays a different role from the account you use for everyday purchases and bill payments. Its main purpose is to hold money for short-term and medium-term goals while keeping those funds accessible when needed. That balance between safety, liquidity, and modest growth is what makes it so useful.

For many households, a savings account is where financial breathing room begins. Instead of leaving extra cash in a checking account where it may be spent too easily, money can be moved into savings and kept separate from day-to-day transactions. That separation helps reduce impulsive spending and makes progress easier to track. It also provides protection against uncertainty. Car repairs, medical bills, travel emergencies, and sudden job changes can all put pressure on a budget. When savings are already set aside, unexpected costs don’t always have to turn into debt.

How Savings Accounts Work

A savings account is a deposit account offered by a bank or credit union. You place money into the account, and the institution pays you interest based on the balance you keep there. In return, your funds remain available for withdrawals or transfers, though savings accounts aren’t intended for constant spending activity.

Interest is usually expressed as APY, or annual percentage yield. This figure shows how much your balance could grow over one year, taking compounding into account. Compounding means you earn interest not only on the money you deposit, but also on the interest that has already been added to the account.

For example, if you deposit money and leave it untouched, the account balance may gradually increase as interest is credited. The pace of growth depends on the APY, how often interest compounds, and whether you continue adding money. Even though savings accounts typically don’t produce high returns compared with long-term investments, they’re valuable because the money remains stable and accessible.

The Main Benefits of a Savings Account

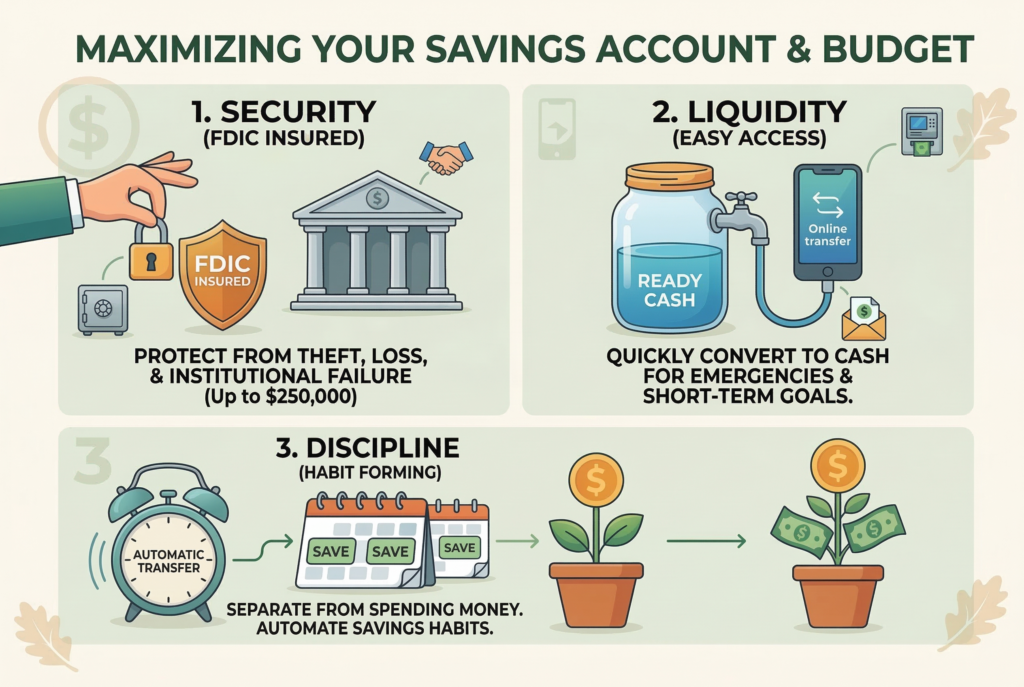

One of the biggest advantages of a savings account is security. Funds are generally held at regulated financial institutions, which makes them much safer than keeping large amounts of cash at home. That peace of mind matters, especially for money set aside for emergencies or upcoming bills.

Another major benefit is discipline. Saving tends to work better when there’s a dedicated place for it. A separate account can create a mental boundary between money meant for spending and money meant for future needs. This simple structure often helps people stay more consistent.

A savings account also provides liquidity. Unlike some financial products that lock up funds for a set term, savings accounts typically allow access when needed. That flexibility is essential for emergency savings or goals with uncertain timing. Then there’s the value of earning interest. While the returns may seem modest, interest still allows your money to grow without additional effort. Over time, especially when paired with regular deposits, that growth can become meaningful.

How Interest Growth Builds Over Time

Interest growth may look slow at first, but it becomes more noticeable when saving is consistent. The key factors are the account’s APY, the starting balance, and how often new contributions are made.

Someone who deposits a lump sum and never adds more will still earn interest, but a person who contributes regularly often sees stronger results because each deposit begins earning interest too. That’s why savings habits matter just as much as the account itself. Compounding is what gives savings momentum. Once interest is added, future interest calculations may include those earlier earnings. The effect isn’t dramatic overnight, but over months and years it supports gradual growth.

This is one reason people often use savings accounts for goals like emergency funds, insurance deductibles, vacations, holiday spending, or down payment reserves. The account may not deliver aggressive growth, but it offers predictable progress while keeping the funds within reach.

Types of Savings Accounts to Know

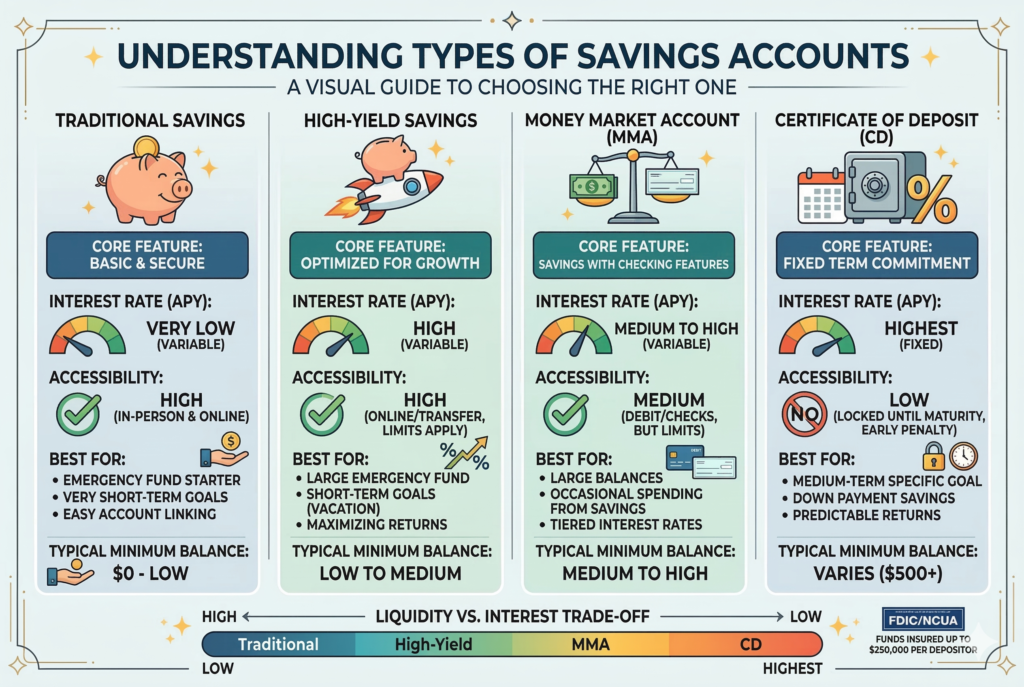

Not all savings accounts are built the same way. A traditional savings account at a branch bank may offer convenience and in-person access, but the interest rate may be relatively low. By contrast, an online savings account often pays a higher APY because online institutions may have lower operating costs.

There are also high-yield savings accounts, which are designed to offer stronger interest rates than standard savings products. These can be especially appealing for people focused on maximizing short-term cash growth without taking market risk.

Some credit unions offer member-focused savings options with competitive rates and lower fees. In other cases, banks may provide specialized savings accounts for students, children, or specific goals. The best fit depends on your priorities. If easy branch access matters most, a traditional institution may feel more practical. If earning a stronger yield is the main goal, an online or high-yield account may deserve closer attention.

How to Choose the Right Savings Account

Choosing the right savings account starts with understanding how you plan to use it. If this account will hold an emergency fund, accessibility and low fees may matter more than anything else. If it’s meant for a goal several months or years away, you may care more about earning a competitive APY.

The first feature to compare is the interest rate or APY. Even small differences in yield can matter over time, especially on larger balances. Still, rate alone shouldn’t decide everything. Fees are just as important. A monthly maintenance fee can quietly reduce the value of your savings, particularly if your balance is still growing. It’s wise to check whether the account requires a minimum balance, charges excess withdrawal fees, or imposes other account costs.

Digital access also matters. A strong mobile app, easy transfers, account alerts, and clear transaction history can make saving much easier to manage. If the process feels inconvenient, people are less likely to stay engaged with it. Customer service, transfer speed, and account linking options should also be considered. A savings account should support your habits, not complicate them.

Savings Account vs. Other Places to Keep Money

A savings account is often compared with checking accounts, money market accounts, and certificates of deposit. Each serves a different purpose.

A checking account is designed for frequent spending, bill pay, and direct deposit activity. It usually offers easier transaction access but lower interest. A savings account, by contrast, is better suited for money you want to protect from daily use.

A money market account may combine some savings features with limited check-writing or debit access, sometimes alongside competitive interest rates. A certificate of deposit, or CD, usually offers a fixed rate in exchange for keeping funds locked in for a set term. That can work well for money you won’t need soon, but it’s less flexible than a savings account. Because of that, savings accounts often fill the middle ground. They’re more growth-oriented than checking and more flexible than term-based products.

Common Mistakes People Make With Savings Accounts

One common mistake is choosing an account without reviewing the fee structure. A savings account that looks appealing on the surface can become less useful if maintenance fees or balance requirements make it harder to grow the account.

Another mistake is leaving too much money in a very low-yield account for too long. Convenience matters, but if the APY is far below what’s available elsewhere, your money may not be working as effectively as it could.

Some people also treat savings as optional rather than routine. In practice, savings tends to build more successfully when transfers are automatic. Waiting to save whatever is left at the end of the month often leads to inconsistency. There’s also the issue of mixing goals together. Keeping every savings objective in one account can make it harder to know what the money is really for. Separating goals, whether through multiple accounts or internal savings buckets, can make planning more precise.

Who Should Have a Savings Account?

Almost anyone who wants greater financial control can benefit from a savings account. It’s useful for workers building an emergency cushion, families preparing for irregular expenses, students learning money habits, and retirees managing cash reserves.

It’s especially important for people trying to avoid relying on credit for unexpected costs. Even a modest savings balance can reduce financial stress and create more options when life becomes expensive. A savings account isn’t a replacement for long-term investing, but it is a foundational part of a balanced financial setup. Before many bigger financial goals become realistic, the habit of saving usually comes first.

How to Make a Savings Account Work Better for You

The most effective approach is usually simple. Open an account with strong terms, set a clear purpose for the money, and automate contributions whenever possible. Regular deposits, even small ones, often matter more than waiting for the perfect moment to save a large amount.

It also helps to review progress periodically. Watching the balance grow can reinforce the habit and make the goal feel more tangible. Whether you’re saving for emergencies, home repairs, travel, or peace of mind, consistency is what turns the account from a good idea into a useful financial tool.

Conclusion

A savings account remains one of the most practical ways to build financial security, earn interest on cash, and prepare for planned or unexpected expenses. It offers a combination of safety, accessibility, and steady growth that makes it valuable for a wide range of financial goals. By comparing account features carefully, paying attention to fees and APY, and contributing consistently, you can choose a savings account that supports both your present needs and your future stability.