When it comes to investing, one of the most crucial elements to consider is your investment time horizon. This refers to the length of time you plan to hold an investment before needing the funds for a specific goal. Whether you’re saving for retirement, a down payment on a home, or a child’s education, understanding how your time horizon impacts your investment strategy is essential to making smart decisions that align with your financial goals.

In this article, we’ll explain what an investment time horizon is, how it impacts your investment choices, and how to choose the right strategy based on your goals and risk tolerance.

What is an Investment Time Horizon?

An investment time horizon is the period during which you plan to hold an investment before needing access to the funds. Your time horizon is critical because it helps determine your investment strategy, including the level of risk you’re comfortable with and the types of assets that are appropriate for your goals.

For example, if you’re saving for a down payment on a house in the next 2-3 years, your time horizon is short, meaning you’ll likely focus on low-risk investments that provide stability and liquidity. On the other hand, if you’re saving for retirement in 20-30 years, your time horizon is long, and you may choose to invest in higher-risk assets like stocks, which can offer higher returns over time. The length of your time horizon directly affects the asset allocation and the types of investment vehicles you should use.

How Time Horizon Affects Your Investment Strategy

Short-Term Investment Goals

For short-term goals, typically defined as goals you expect to achieve in less than 5 years, the focus is on capital preservation and liquidity. With a short time frame, you’ll want to prioritize investments that are low risk and allow you to easily access your funds when needed.

If you’re saving for a vacation, a new car, or an emergency fund, your investment choices will likely include money market funds, short-term bonds, or high-yield savings accounts. These types of investments offer stability and minimal risk, but they may not provide high returns. The goal is to protect your principal while maintaining enough flexibility to access your funds when the need arises.

Medium-Term Investment Goals

If your goal is 5 to 10 years away, your investment strategy will likely fall between the extremes of safety and growth. For medium-term goals, such as saving for a child’s college tuition or a home down payment, you might be able to take on a little more risk, but you’ll still want to keep your investments balanced. At this stage, a diversified portfolio could include stocks, bonds, and mutual funds.

With a medium-term horizon, it’s often best to strike a balance between growth and stability. You may want to invest in a mix of growth stocks for higher potential returns and bonds or bond funds to ensure more stable income streams.

Long-Term Investment Goals

For long-term goals, typically defined as 10 years or more, your time horizon allows you to ride out market fluctuations. Long-term investing often involves higher-risk assets like stocks and equity mutual funds, which offer the potential for greater returns over time. The reason you can afford to take on more risk is that you have time to recover from any downturns in the market before you need to access your funds.

If you’re saving for retirement or building wealth over the long run, you can afford to invest in riskier assets because you don’t need immediate access to the money. With a long-term horizon, you can focus on growth and take advantage of compounding to maximize your returns.

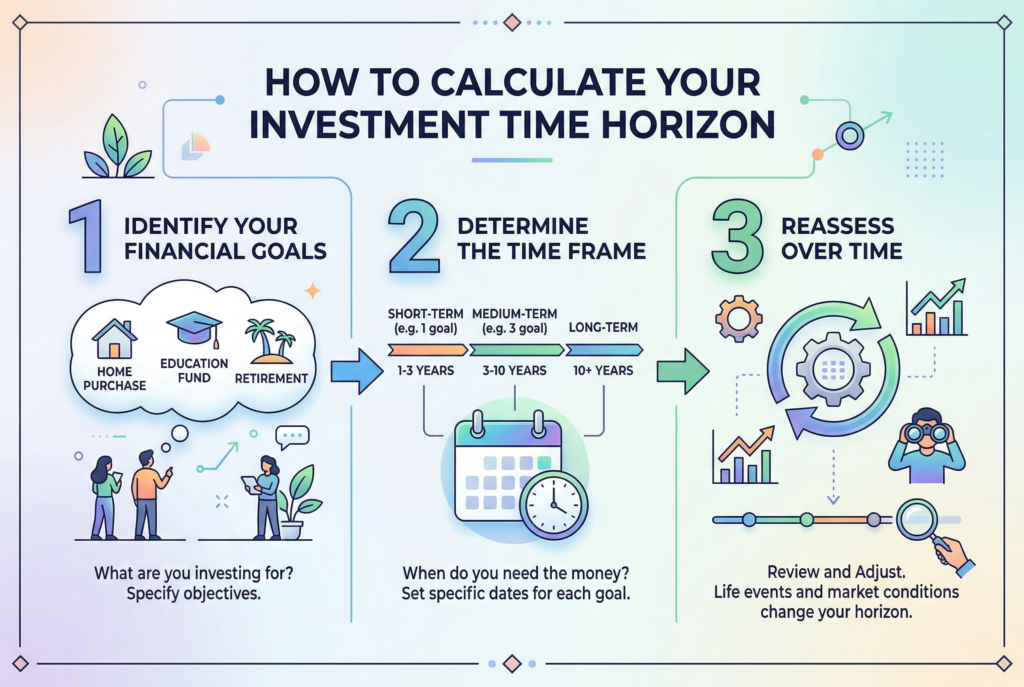

How to Calculate Your Investment Time Horizon

- Identify your financial goals: What are you saving for? Are you buying a home in 3 years? Or are you planning for retirement in 30 years?

- Determine the time frame: Based on your goals, calculate how long you’ll need to keep your investments. Short-term goals typically fall within 1 to 5 years, medium-term goals fall within 5 to 10 years, and long-term goals extend beyond 10 years.

- Reassess over time: Your time horizon may change as your goals evolve. Life changes, such as a new job, marriage, or a child’s education needs, can shift your priorities and timeline. It’s important to reassess your time horizon periodically.

Understanding your time horizon will help you determine your risk tolerance and asset allocation, which are crucial elements for developing a strong investment strategy.

Common Mistakes with Investment Time Horizons

Investing Too Conservatively for Long-Term Goals

If you invest too conservatively for long-term goals like retirement, you might miss out on higher returns that could help you achieve your goals. While safety is important, it’s also important to have a portion of your portfolio in higher-growth assets.

Investing Too Aggressively for Short-Term Goals

On the flip side, taking on too much risk for short-term goals can expose you to significant losses when the market fluctuates. If you’re saving for a down payment in a couple of years, investing in volatile assets like stocks may not be the best approach.

Failing to Reassess Your Time Horizon

Your time horizon may change over time as your goals and circumstances evolve. Failing to reassess your time horizon periodically could result in mismatched investment choices.

Why Time Horizon Matters for Investment Success

Your investment time horizon plays a crucial role in shaping your investment strategy. It impacts:

- Risk tolerance: The longer your time horizon, the more risk you can afford to take on, as you have time to recover from any market downturns.

- Asset allocation: The time horizon helps determine the mix of stocks, bonds, and other assets in your portfolio. Short-term goals usually call for safer, more liquid investments, while long-term goals allow for more growth-oriented investments.

- Investment choices: Your time horizon also affects whether you choose stocks, mutual funds, bonds, or other assets. Longer-term investors tend to focus more on stocks and equity investments, while those with shorter-term goals may prioritize fixed-income investments like bonds.

By aligning your investment strategy with your time horizon, you’ll be better positioned to achieve your financial goals without taking on more risk than you can handle.

Conclusion: Align Your Strategy with Your Time Horizon

Understanding and managing your investment time horizon is key to making smart financial decisions that will help you achieve your goals. Whether you’re saving for short-term objectives like a vacation or long-term goals like retirement, the length of your time horizon directly impacts your risk tolerance, asset allocation, and investment choices. By tailoring your strategy to your time horizon, you can build a portfolio that works for you, whether you need flexibility, growth, or stability.

Take the time to assess your financial goals, define your time horizon, and adjust your investment strategy accordingly. This proactive approach will give you the confidence and direction needed to achieve financial success over the long term.