In today’s fast-paced financial landscape, where interest rates fluctuate and market volatility is ever-present, many investors seek safer alternatives to parking their money. If you’re looking for a low-risk investment with relatively stable returns, money market funds (MMFs) might be the right option for you. These funds offer a safe, liquid, and low-risk way to grow your savings. In this article, we’ll dive into what money market funds are, how they work, their benefits, and why they can be a smart investment choice for many individuals.

What are Money Market Funds?

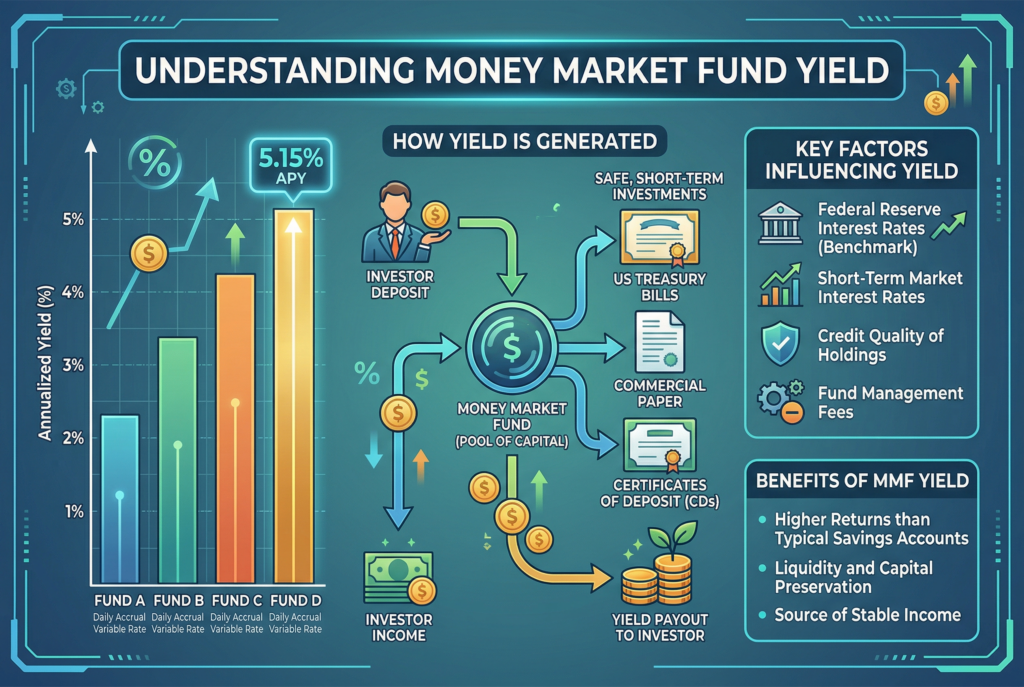

A money market fund (MMF) is a type of mutual fund that invests in short-term, high-quality debt instruments like government securities, certificates of deposit (CDs), commercial paper, and repurchase agreements. MMFs aim to offer liquidity, principal preservation, and low risk, all while providing a higher return than traditional savings accounts.

MMFs typically maintain a $1 per share net asset value (NAV), meaning they strive to keep their share price stable. However, while they’re generally considered low-risk, the returns can vary depending on the performance of the underlying debt securities and prevailing interest rates.

How Money Market Funds Work

Money market funds pool capital from multiple investors and invest in short-term, low-risk debt securities. The fund aims to generate interest income for investors, with the returns distributed regularly, often monthly. The fund’s goal is to keep the NAV stable, usually around $1 per share, making MMFs a safe and easily redeemable investment vehicle.

Unlike a savings account, MMFs aren’t FDIC-insured but are regulated by the Securities and Exchange Commission (SEC). Although these funds generally provide more liquidity than other investments, some money market funds may charge a fee if there’s a high level of withdrawals, especially during times of market turbulence.

The Key Benefits of Money Market Funds

Low Risk and Stability

The primary appeal of MMFs is their low-risk nature. By investing in short-term, high-quality debt instruments, such as Treasury bills and highly rated corporate bonds, MMFs offer investors safety with a minimal chance of principal loss. These funds are designed to provide steady returns with relatively low volatility, which is particularly appealing in uncertain economic times.

Additionally, since MMFs invest in short-term securities (usually with maturities of less than one year), they’re less susceptible to the interest rate fluctuations and economic shifts that affect longer-term investments, like stocks or bonds.

Liquidity and Easy Access

Another major advantage of money market funds is their liquidity. MMFs allow investors to easily buy or redeem shares. This makes them an excellent option for those who need access to cash quickly. Unlike some other investment vehicles, which may require waiting for long periods to liquidate, MMFs allow you to move your money as needed, usually within a few business days. This flexibility makes MMFs an ideal place to park funds for short-term goals or as a temporary safe haven for cash, without having to worry about a lack of access.

Better Yields than Savings Accounts

One of the primary reasons investors turn to money market funds is the higher yields they typically offer compared to traditional savings accounts or money market deposit accounts (MMDAs). MMFs invest in a variety of short-term debt instruments that usually provide better returns than standard bank accounts.

For instance, while traditional savings accounts often offer interest rates of 0.1% or lower, money market funds tend to yield higher returns, especially when interest rates are rising. Given their relatively low risk and easy access to funds, they can be a great choice for emergency savings or cash that needs to stay liquid.

Diversification and Flexibility

Money market funds offer diversification by investing in a variety of short-term debt instruments, which helps spread risk. Unlike holding a single certificate of deposit or Treasury bond, investing in an MMF allows you to gain exposure to a range of securities, which can offer a more stable return. Additionally, MMFs are flexible and can be included in different investment accounts, including IRAs or 401(k)s, providing more options for tax-efficient investing.

Risks to Consider with Money Market Funds

Credit Risk

Although MMFs primarily invest in low-risk, short-term debt securities, there is still a chance that an issuer of a bond or other debt security could default. This is known as credit risk. MMFs aim to minimize this risk by investing in high-quality assets, but investors should understand that there is always some level of risk associated with these investments.

Inflation Risk

MMFs often offer modest returns, especially in low-interest-rate environments. While they’re a safer alternative to stocks, inflation can erode the purchasing power of the returns earned from MMFs. If inflation rises faster than the yield offered by your MMF, the real return could be negative, meaning you could lose purchasing power over time.

Interest Rate Risk

Although MMFs typically invest in short-term debt instruments that are less sensitive to interest rate fluctuations, rising interest rates can still affect the performance of MMFs. When interest rates rise, the price of existing bonds falls, which can impact the performance of MMFs. However, because MMFs focus on short-term investments, they typically adjust quickly to changes in interest rates.

No FDIC Insurance

Unlike money market deposit accounts (MMDAs), money market funds are not FDIC-insured. Instead, they’re regulated by the Securities and Exchange Commission (SEC) and are covered by SIPC insurance, which protects investors in case of fraud or mismanagement, but doesn’t cover losses due to market fluctuations.

Types of Money Market Funds

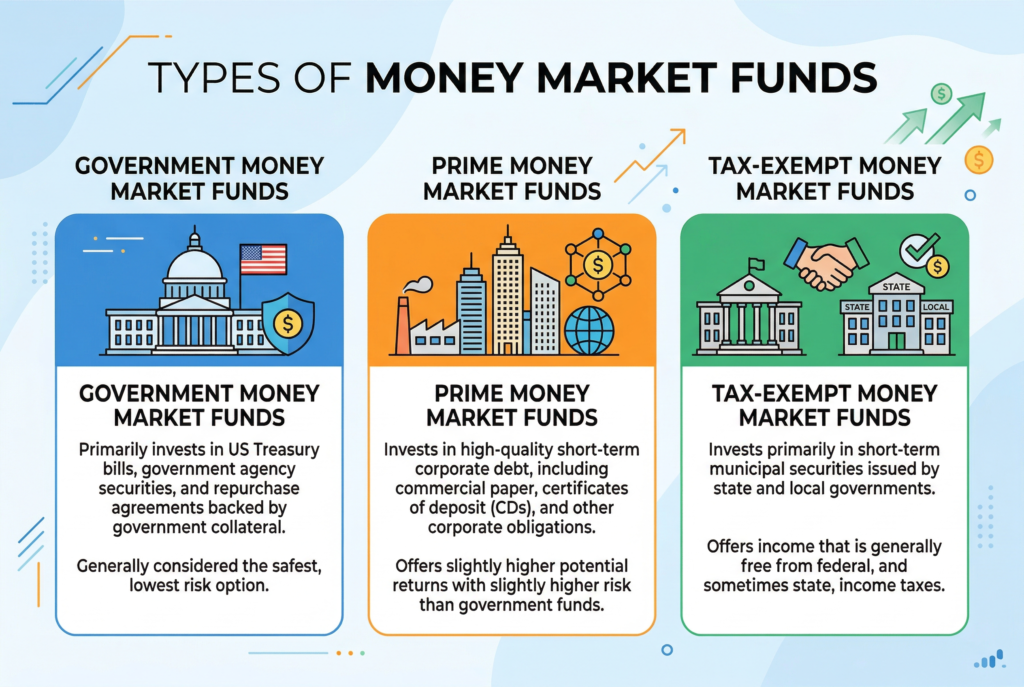

Government Money Market Funds

These funds invest primarily in U.S. government securities, such as Treasury bills and repurchase agreements. These funds are the safest option, offering minimal risk since the U.S. government backs the debt securities.

Prime Money Market Funds

Prime MMFs invest in a broader range of short-term debt instruments, including corporate bonds and commercial paper. While these funds offer higher returns than government MMFs, they come with slightly more risk due to their exposure to corporate debt.

Tax-Exempt Money Market Funds

Tax-exempt MMFs invest in municipal bonds, offering tax-free income to investors. These funds are a good option for individuals in higher tax brackets looking for a safe, tax-efficient way to park their money. However, they tend to offer lower yields than taxable MMFs.

When to Use Money Market Funds

Money market funds are best used for short-term savings goals where you need liquidity and capital preservation. They’re ideal for:

- Emergency funds

- Short-term savings goals, like a vacation or car purchase

- Holding cash temporarily while deciding on longer-term investments

MMFs also serve as a safe haven during periods of market volatility, where investors seek a low-risk place to park cash without locking it up for extended periods.

Conclusion: A Safe and Smart Investment Choice

Money market funds offer a low-risk, liquid, and relatively high-yielding investment option for those looking to preserve their capital while earning better returns than traditional savings accounts. They’re ideal for investors seeking short-term safety, easy access to funds, and diversification within a broader investment strategy.

However, like all investments, MMFs come with some risks, such as credit and inflation risk. Understanding these risks and balancing them with your financial goals will help you determine if MMFs are the right choice for your portfolio. By using MMFs strategically, you can enhance liquidity, earn stable returns, and protect your wealth in today’s dynamic financial environment.

Related Articles

Money Market Accounts Explained: Key Features, Current Rates, Pros and Cons for Savers