If you’re looking for a low-risk, high-yield investment option, CD ladders (Certificate of Deposit ladders) might be an excellent choice. This strategy helps you take advantage of higher interest rates associated with long-term CDs, while still maintaining some flexibility and liquidity with short-term CDs. In this article, we’ll break down what CD ladders are, how they work, the benefits they offer, and practical steps to build one that fits your financial needs.

What is a CD Ladder?

A CD ladder is a strategy where you divide your investment across multiple Certificates of Deposit (CDs) with varying maturity dates. By using this approach, you can earn higher interest rates on long-term CDs while still ensuring regular access to your money as each CD matures. Instead of locking up all your money in one long-term CD, a ladder allows you to balance the need for higher returns with the flexibility of accessing portions of your funds at regular intervals.

For example, if you have $30,000 to invest, you might choose to place:

- $5,000 in a 1-year CD

- $5,000 in a 2-year CD

- $5,000 in a 3-year CD

- $5,000 in a 4-year CD

- The remaining $10,000 in a 5-year CD

Each time a CD matures, you can either withdraw the funds or reinvest them into a new 5-year CD, taking advantage of the best available rates.

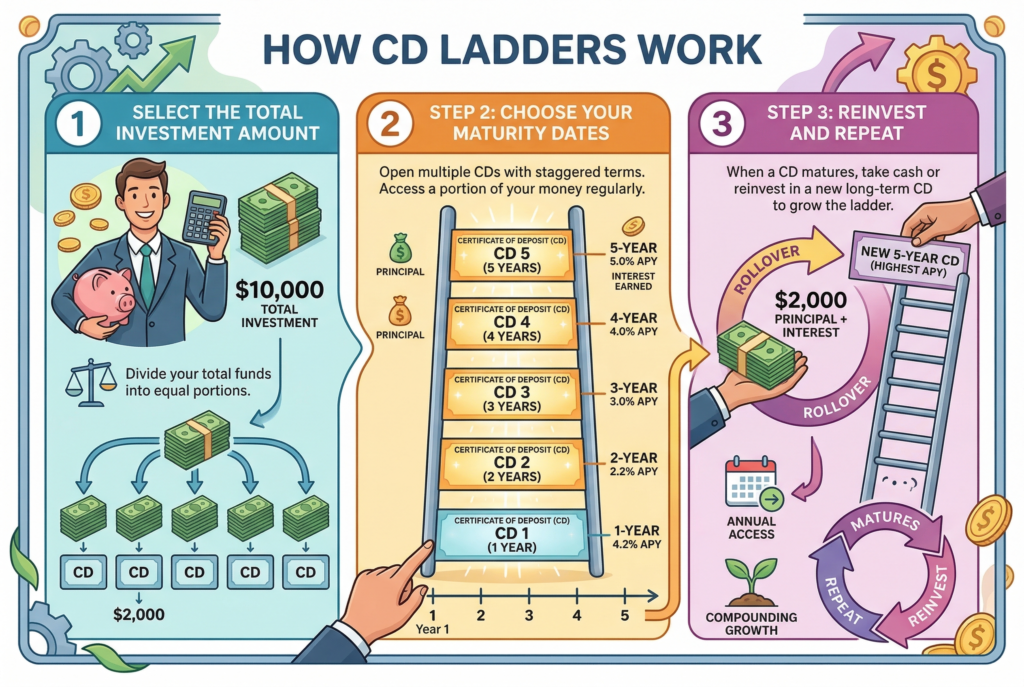

How CD Ladders Work

Step 1: Select the Total Investment Amount

Determine how much money you want to invest in a CD ladder. This can vary based on your goals, such as saving for a major purchase, building a retirement fund, or just growing your savings in a low-risk environment.

Step 2: Choose Your Maturity Dates

Next, decide on the maturity dates for your CDs. Typically, you’ll want to spread your investment across different term lengths, such as 1-year, 2-year, or 3-year, so you can take advantage of higher interest rates offered by longer-term CDs while having access to your money at regular intervals.

For instance, you could invest a portion of your funds in short-term CDs (for example, 1-year CDs) and the rest in long-term CDs (for example, 3 or 5 years). As each CD matures, you can reinvest the principal and interest into a new long-term CD, effectively maintaining a ladder.

Step 3: Reinvest and Repeat

When one of your CDs matures, you’ll have the option to reinvest the principal and the interest into a new CD with a longer maturity date. This allows you to maintain the ladder and potentially benefit from the best available rates in the market.

The process of reinvesting keeps your savings working hard for you, while also ensuring you maintain a predictable return on your investment.

Key Benefits of CD Ladders

Predictable Returns

One of the biggest advantages of CD ladders is the predictability of returns. Since CDs are FDIC-insured and offer fixed interest rates, you know exactly how much you will earn over the life of each CD. This can help provide a sense of security for those looking to avoid the volatility of the stock market.

Liquidity

Unlike traditional long-term CDs, which lock up your funds for several years, a CD ladder ensures that you have access to a portion of your funds at regular intervals. This means you can withdraw or reinvest funds as needed, without having to break a CD early and incur penalties.

Flexibility

By building a CD ladder, you can choose different maturities based on your specific financial needs. You can decide whether you need more flexibility with short-term CDs or whether you want to maximize your return with long-term CDs. This flexibility allows you to adjust your strategy based on changes in your financial situation.

Higher Interest Rates

Typically, the longer the term of the CD, the higher the interest rate you’ll earn. A CD ladder allows you to lock in these higher interest rates on a portion of your funds, while still keeping access to other funds through shorter-term CDs.

Safety and Low Risk

Since CDs are FDIC-insured up to $250,000 per depositor, per institution, CD laddering offers a safe, low-risk investment strategy. This makes it an attractive option for conservative investors who want predictable returns without the risk of market fluctuations.

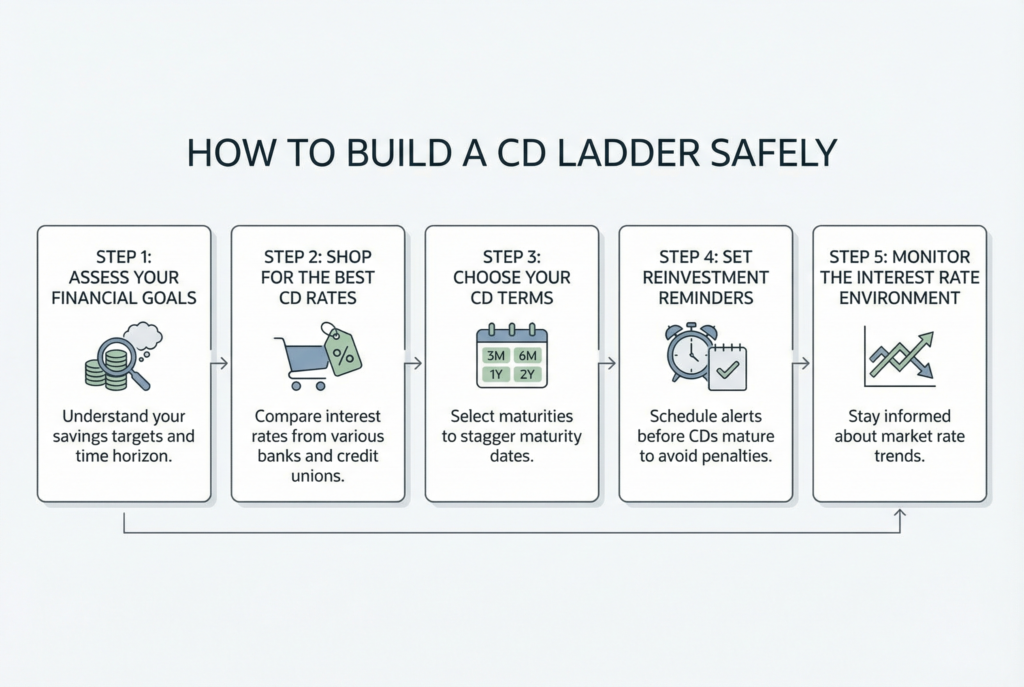

How to Build a CD Ladder Safely

Step 1: Assess Your Financial Goals

Before you start investing in CDs, it’s important to assess your financial goals. Are you saving for a down payment on a house, planning for retirement, or building an emergency fund? Your goals will help you determine how much to invest, the length of time you’ll want to commit, and how liquid you need your investments to be.

Step 2: Shop for the Best CD Rates

Interest rates can vary significantly depending on the financial institution, so it’s important to shop around for the best rates. Look for banks or credit unions that offer competitive CD rates and ensure that they are FDIC-insured. Online banks often offer better rates than traditional brick-and-mortar banks, so don’t hesitate to explore all options.

Step 3: Choose Your CD Terms

Select the terms for your CDs based on your liquidity needs. For example, if you need access to cash every year, you might choose a mix of 1-year, 2-year, and 3-year CDs. The goal is to balance having access to some of your funds while still benefiting from higher rates offered by longer-term CDs.

Step 4: Set Reinvestment Reminders

To maintain your CD ladder, it’s important to keep track of when your CDs mature. You’ll want to reinvest the proceeds into a new CD to maintain the ladder and continue earning the best available rates. Set a calendar reminder to ensure you stay on top of this.

Step 5: Monitor the Interest Rate Environment

Interest rates can fluctuate, so it’s essential to keep an eye on the current rate environment. If interest rates are expected to rise, you might want to adjust your CD ladder strategy accordingly by locking in longer-term CDs at current rates before they increase.

When CD Ladders Don’t Make Sense

While CD ladders offer many advantages, they might not be the best option for everyone. Consider the following:

- Low interest rates: If the interest rates are low, you may find that a CD ladder doesn’t offer the best return. In such cases, exploring alternative low-risk investments, such as high-yield savings accounts, may be a better option.

- Inflation concerns: If inflation is high, the real returns from CDs may be eroded over time. In such situations, it’s important to assess whether the predictable returns from a CD ladder outweigh the potential loss of purchasing power.

Conclusion: Maximize Your Savings with a CD Ladder

Building a CD ladder can be a smart and effective way to earn predictable returns while maintaining some liquidity. This strategy allows you to balance the safety and security of FDIC-insured CDs with the opportunity to earn higher interest rates. By following the steps outlined in this article, you can build a CD ladder that fits your financial goals, maximizes your returns, and provides flexibility as your funds mature.

While CD ladders may not offer the highest returns compared to riskier investments like stocks, they’re a low-risk, secure option for investors seeking stability and predictability in their savings strategy. Start building your CD ladder today, and enjoy the peace of mind that comes with having a structured, low-risk investment plan.