: How They Work, Tax Benefits, and Smart Ways to Save for School")

An Education Savings Account (ESA) usually refers to a Coverdell ESA, a tax-advantaged account designed to help families save for a child’s education expenses. It can be a useful option for people who want tax-free growth and flexible use of funds for both K-12 and higher education costs, but it comes with tighter contribution limits and income rules than many families expect.

What Is an Education Savings Account?

A Coverdell ESA is a trust or custodial account created in the United States for the sole purpose of paying a designated beneficiary’s qualified education expenses. The beneficiary generally must be under age 18 when the account is opened, unless they’re a special needs beneficiary. Unlike some college-focused savings tools, a Coverdell ESA can be used for both qualified higher education expenses and qualified elementary or secondary education expenses.

That flexibility is one reason some families still look at ESAs even though 529 plans are more widely used. A 529 plan is another tax-advantaged education savings vehicle, but it operates under different rules and is generally sponsored by states, state agencies, or educational institutions.

How a Coverdell ESA Works

A Coverdell ESA works a lot like an investment account for education. You contribute cash, the money can be invested, and any earnings grow tax free as long as withdrawals are used for qualified education expenses. Contributions aren’t tax deductible, so the tax benefit comes on the growth and the tax-free qualified distributions rather than on the way in.

There’s no limit on the number of Coverdell ESAs a beneficiary can have, but the total annual contribution across all accounts for that beneficiary can’t exceed $2,000. Contributions also must be made by the due date of the contributor’s tax return, not including extensions. This structure makes the ESA most useful as a targeted savings tool rather than a full college-funding solution by itself. The contribution cap is relatively small, so many households that use an ESA treat it as one piece of a broader education savings plan.

Who Can Contribute and What the Income Limits Are

Individuals can contribute to a Coverdell ESA if their modified adjusted gross income falls below the allowed limits. For 2025, the IRS says the $2,000 contribution limit begins phasing out between $95,000 and $110,000 for single filers and between $190,000 and $220,000 for joint filers. At or above the top of those ranges, an individual can’t contribute. Organizations such as corporations and trusts can contribute regardless of adjusted gross income.

Another important rule is age. In general, contributions can’t be made after the beneficiary reaches age 18 unless the beneficiary is a special needs beneficiary.

These rules matter because they can affect whether an ESA is practical for your household. Families with higher income may need to rely more heavily on other education savings options, while families with younger children may benefit more from the time available for tax-free growth.

The Main Tax Benefits of an ESA

The biggest advantage of a Coverdell ESA is tax treatment. Qualified distributions are tax free to the extent they don’t exceed the beneficiary’s qualified education expenses. That means investment gains can be withdrawn without federal tax when the money is used properly. If a distribution is larger than qualified expenses, part of the earnings may become taxable to the beneficiary.

Another key benefit is expense flexibility. IRS guidance says qualified expenses can include not only higher education costs but also qualified elementary and secondary education expenses. That broader range is one of the most appealing features of the account for families who expect private school, tutoring, curriculum, or certain school-related technology costs before college.

That said, tax coordination matters. Families should be careful not to use the same expenses for multiple tax benefits in ways the IRS doesn’t allow. When education credits, 529 plan withdrawals, and ESA withdrawals all overlap, recordkeeping becomes especially important.

What Expenses an ESA Can Cover

One of the strongest selling points of a Coverdell ESA is that qualified expenses go beyond college tuition. IRS Publication 970 explains that qualified elementary and secondary education expenses can include costs tied to enrollment or attendance at an eligible elementary or secondary school, and it also includes certain computer-related expenses and internet access used by the beneficiary and family during the beneficiary’s elementary or secondary school years.

For higher education, tax-free withdrawals can generally be used for qualified post-secondary education expenses, subject to IRS rules on what counts and how those costs coordinate with other education tax benefits.

That flexibility can make an ESA attractive for families who know education costs will start before college. In practice, it can work well for households with a clear K-12 funding plan, not just a college plan.

Drawbacks Families Should Understand

The main drawback is the low annual contribution limit. $2,000 per year usually isn’t enough on its own to cover the long-term cost of private school or college, especially if you’re starting late.

Another limitation is the income phaseout, which can restrict who’s allowed to contribute directly. There’s also an age deadline on the back end. In general, remaining assets must be distributed within 30 days after the beneficiary reaches age 30, unless the beneficiary is a special needs beneficiary.

Certain rollovers and family-member beneficiary changes are allowed, but the age rules still make planning important. This is why ESAs often work best for families who want flexibility and tax benefits but also understand the account’s narrow limits. It’s a helpful tool, but it isn’t always the simplest or biggest one.

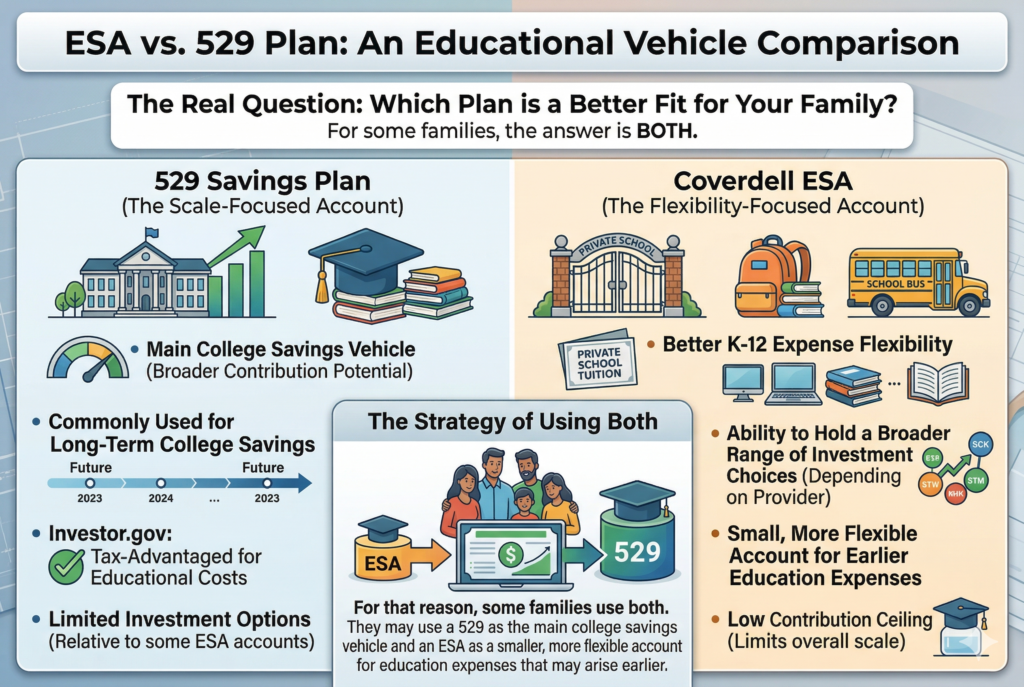

ESA vs 529 Plan: Which Is Better?

For many families, the real question isn’t whether an ESA is good. It’s whether it’s better than a 529 plan. A 529 plan is also tax advantaged, and Investor.gov notes that it’s designed to encourage saving for certain educational costs. It generally offers broader contribution potential and is more commonly used for long-term college savings.

A Coverdell ESA stands out more on flexibility for certain K-12 expenses and on the ability to hold a broader range of investment choices depending on the provider. But the 529 usually wins on scale because the contribution ceiling for an ESA is so low. For that reason, some families use both. They may use a 529 as the main college savings vehicle and an ESA as a smaller, more flexible account for education expenses that may arise earlier.

Smart Ways to Save for School With an ESA

The smartest way to use a Coverdell ESA is to match it to a specific goal. If you know your child may attend private elementary or secondary school, the ESA’s K-12 flexibility may be especially valuable. If your goal is college only, the ESA can still help, but the low annual cap means you’ll probably want another savings vehicle alongside it.

It also helps to start early. Because contributions are capped at $2,000 per year, time matters. The earlier you begin, the more years of tax-free growth you give the account. Another smart move is keeping good records. Since tax-free treatment depends on qualified expenses, you’ll want documentation showing what withdrawals paid for and when. The IRS notes that account holders should receive Form 1099-Q for distributions, which helps with tax reporting.

Finally, think in terms of coordination. An ESA works best when it fits into your broader education plan, alongside emergency savings, retirement contributions, and possibly a 529 plan. School savings should support your overall finances, not compete with core priorities.

Conclusion

A Coverdell ESA can be a valuable education savings tool for families who want tax-free growth and the ability to use funds for both K-12 and higher education expenses. Its biggest strengths are flexibility and tax-free qualified withdrawals, while its biggest weaknesses are the $2,000 annual contribution cap, income phaseouts, and age-based distribution rules. For the right household, it can be a smart way to save for school, especially when paired with a larger education funding strategy.