When applying for a mortgage, understanding the Loan-to-Value (LTV) ratio is critical for securing favorable loan terms. Your LTV ratio is one of the primary factors that lenders use to assess the risk of lending to you, and it plays a major role in the interest rates and fees you may pay over the life of your loan. Whether you’re a first-time homebuyer, refinancing, or simply exploring loan options, understanding LTV is key to making informed decisions.

In this article, we’ll explain exactly what LTV is, how to calculate it, why it matters, and practical steps you can take to improve your LTV ratio and secure the best loan terms.

What is Loan-to-Value (LTV) Ratio?

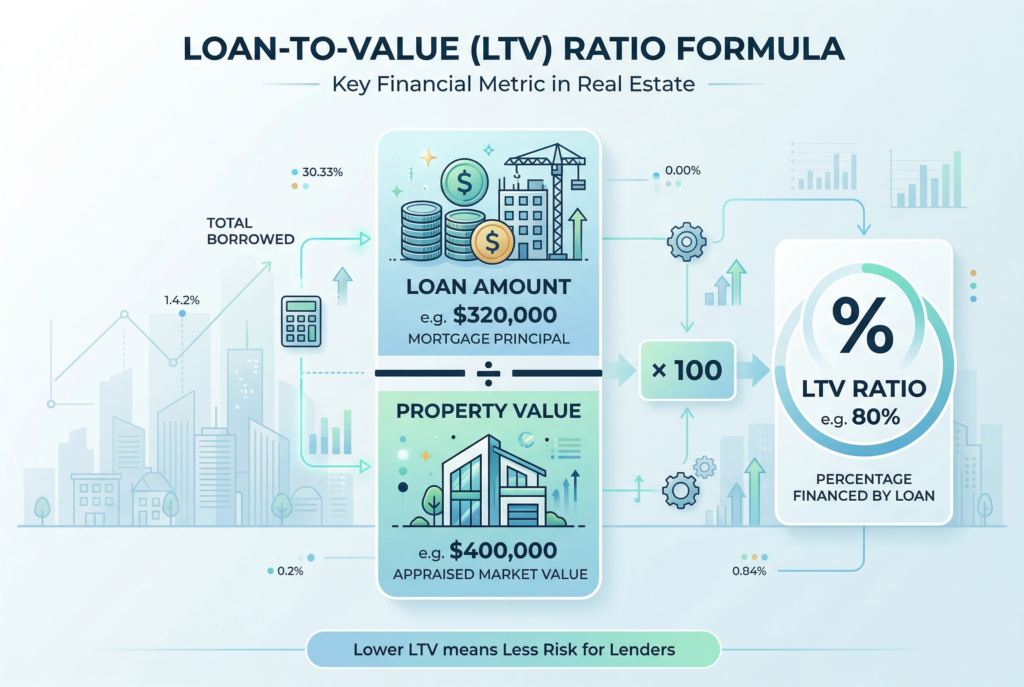

The Loan-to-Value (LTV) ratio is the percentage of the property’s value that you’re borrowing. It’s calculated by dividing the loan amount by the appraised value or purchase price of the property (whichever is lower), and multiplying by 100. Essentially, the LTV ratio measures the risk for lenders; the higher the LTV, the riskier the loan is for them.

For example, if you’re purchasing a home valued at $300,000 and you take out a mortgage for $240,000, your LTV ratio would be 80%. The remaining 20% is covered by your down payment.

Why LTV Matters for You

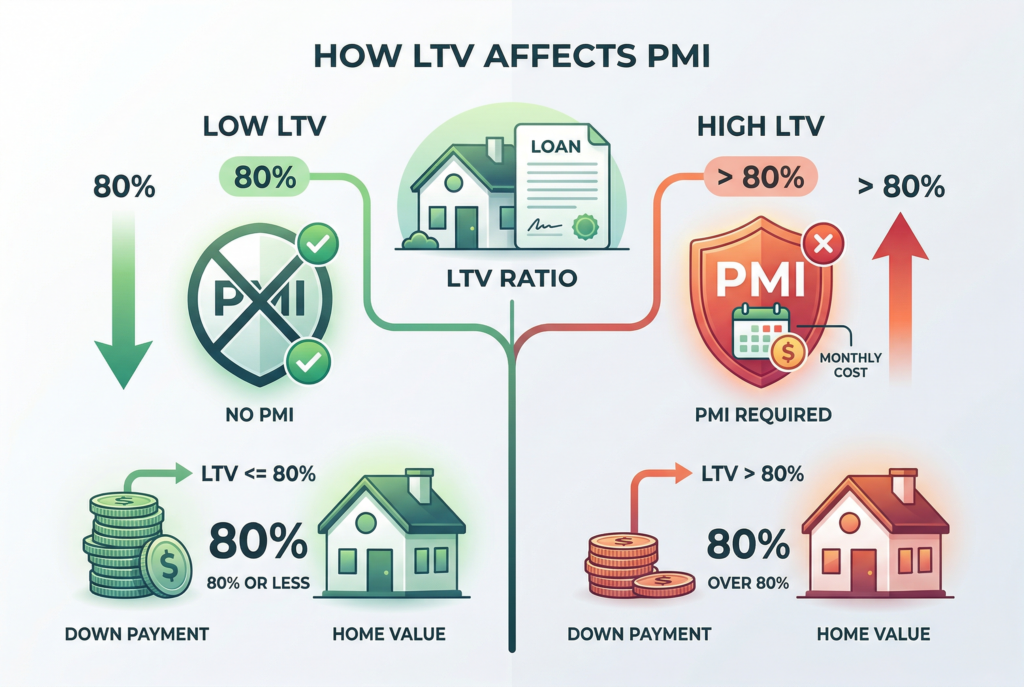

LTV is an important factor in mortgage approvals because it helps lenders assess how much of the property’s value you’re borrowing. A higher LTV ratio means a higher risk for the lender, and they might require you to purchase Private Mortgage Insurance (PMI) to offset that risk. Here’s how LTV affects your loan terms:

1. Mortgage Insurance (PMI)

One of the most significant consequences of a high LTV ratio is the need for Private Mortgage Insurance (PMI). If your LTV ratio exceeds 80%, most lenders will require you to pay PMI. This insurance protects the lender if you default on the loan. PMI can significantly increase your monthly payments, and it can cost anywhere from 0.3% to 1.5% of the original loan amount per year.

If you manage to keep your LTV below 80%, you can avoid PMI and keep your mortgage payments lower.

2. Interest Rates

Lenders typically offer lower interest rates to borrowers with a low LTV ratio because it reduces their risk. If you put down a larger down payment and have a lower LTV, you’re seen as less of a financial risk, which could result in better loan terms. On the other hand, high LTV ratios are often associated with higher interest rates, as lenders are taking on more risk by lending a larger percentage of the property’s value.

3. Loan Approval

Lenders use the LTV ratio to decide whether to approve a loan application. If your LTV is too high, they may reject your application or require a larger down payment. Most conventional loans require an LTV ratio of 80% or lower. However, some government-backed loans, like those from the FHA, may accept higher LTV ratios.

How to Calculate LTV Ratio

Calculating your LTV ratio is a straightforward process, but it’s essential to get the right numbers in order to understand the financial implications. Here’s the formula:

LTV Ratio = (Loan Amount ÷ Property Value) × 100

Example: Calculating LTV

Let’s say you want to purchase a property worth $250,000, and you plan to make a $50,000 down payment. Here’s how to calculate your LTV:

- Loan Amount: $250,000 (purchase price) – $50,000 (down payment) = $200,000 (loan amount)

- LTV Calculation: (Loan Amount / Property Value) × 100 = ($200,000 / $250,000) × 100 = 80%

So, in this case, your LTV ratio is 80%. This means you’re borrowing 80% of the property’s value and putting down the remaining 20%.

What’s the Ideal LTV Ratio?

While 80% LTV is often considered the sweet spot, the ideal LTV depends on several factors:

- Conventional loans: With a conventional loan, a LTV ratio of 80% or lower is ideal to avoid PMI and secure favorable interest rates. Some lenders may offer loans with higher LTV ratios, but they may come with additional costs, such as PMI and higher rates.

- FHA loans: For FHA loans, the maximum LTV ratio can be as high as 96.5%, meaning you can potentially buy a home with just a 3.5% down payment. However, you’ll likely pay mortgage insurance premiums (MIP) on top of the loan.

- VA loans: VA loans for veterans and active military members offer 100% financing, meaning no down payment and an LTV of 100%. These loans are often the best option for eligible individuals because they come with low rates and no PMI requirements.

- USDA loans: Similar to VA loans, USDA loans are also available for rural homebuyers with 100% financing. This means no down payment and an LTV of 100%.

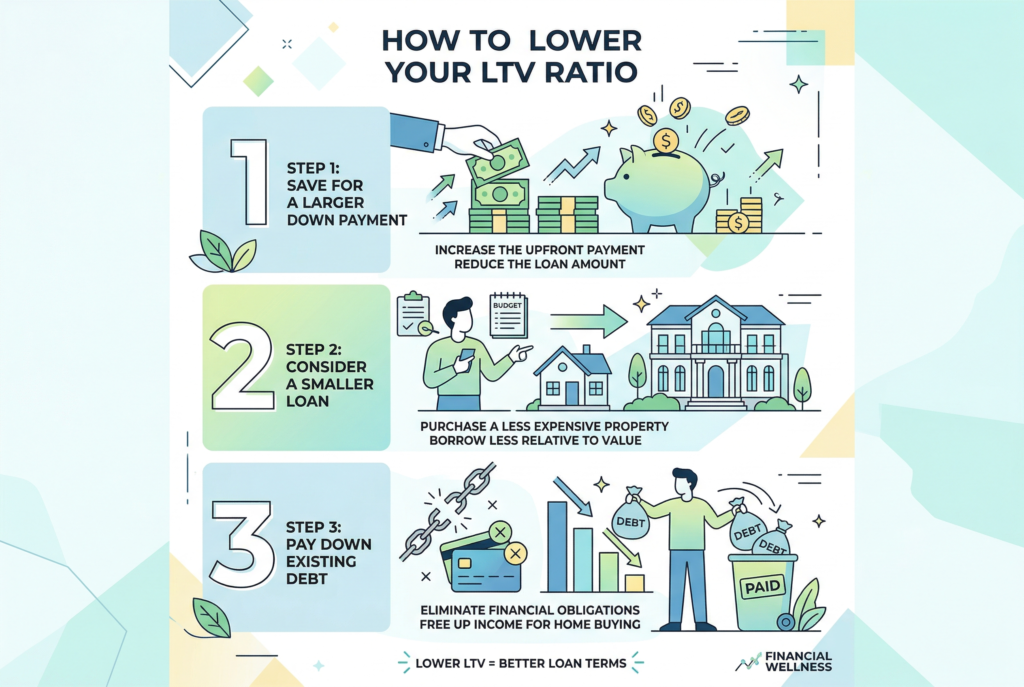

How to Lower Your LTV Ratio

Step 1: Save for a Larger Down Payment

The easiest way to lower your LTV ratio is to increase your down payment. If your current LTV is 90%, increasing your down payment by 5% or 10% will significantly reduce your LTV and may help you qualify for better loan terms.

Step 2: Consider a Smaller Loan

Another way to reduce your LTV ratio is by purchasing a less expensive home. A smaller loan will naturally result in a lower LTV, making it easier to secure better financing options and interest rates.

Step 3: Pay Down Existing Debt

If you already own a property and are refinancing, paying down your existing mortgage or other debts can lower your LTV ratio. This strategy can be especially helpful if your home has appreciated in value since you originally purchased it.

Conclusion: Understanding and Managing Your LTV Ratio

The Loan-to-Value (LTV) ratio is a key factor in securing the right mortgage terms. By understanding how LTV works, how to calculate it, and the impact it has on your loan terms, you can make more informed decisions about your home purchase and financing options. Lowering your LTV ratio by increasing your down payment or refinancing can help you secure better rates, avoid PMI, and reduce the total cost of your mortgage.

Always keep in mind that lenders prefer borrowers with lower LTV ratios, as it reduces the risk to them. By aiming for an LTV of 80% or lower, you’ll not only save money but also improve your chances of approval. If you’re ready to buy a home or refinance, taking steps to manage your LTV ratio is essential to getting the best deal on your mortgage.