For many veterans, active-duty service members, and surviving spouses, buying a home can feel daunting. Traditional mortgages often require large down payments and private mortgage insurance, adding to the financial burden. Fortunately, VA loans exist to provide veterans with easier access to homeownership, lower costs, and a path to long-term financial stability. Understanding how VA loans work, who qualifies, and how to maximize their benefits is essential for making smart decisions.

What Is a VA Loan?

A VA loan is a mortgage program guaranteed by the U.S. Department of Veterans Affairs. Unlike conventional loans, VA loans often require no down payment, no private mortgage insurance (PMI), and offer competitive interest rates. The guarantee from the VA reduces the risk for lenders, allowing eligible borrowers to secure financing under favorable terms.

VA loans can be used to purchase a primary residence, refinance an existing mortgage, or in some cases, to renovate a home. They’re specifically designed for veterans, active-duty service members, and certain surviving spouses. The primary goal of the VA loan program is to make homeownership accessible and affordable for those who have served.

Who Qualifies for a VA Loan?

Eligibility for a VA loan is based on military service, length of service, and character of discharge. Key groups include:

- Veterans who served a minimum period of active duty, depending on the era of service.

- Active-duty service members who meet specific tenure requirements.

- Surviving spouses of service members who died in the line of duty or due to a service-related condition.

- Certain members of the National Guard and Reserves who meet length-of-service requirements.

To apply, borrowers must obtain a Certificate of Eligibility (COE) from the VA, which verifies their entitlement to a VA-backed loan. Many lenders can request the COE on your behalf, making the process smoother.

Key Benefits of VA Loans

VA loans offer several advantages that set them apart from conventional financing options. First and foremost, no down payment means you can purchase a home without needing to save tens of thousands of dollars upfront. In addition, VA loans don’t require private mortgage insurance (PMI), a cost that often adds hundreds of dollars per month for conventional loans with less than 20% down.

Interest rates on VA loans are typically lower than conventional or FHA loans, making monthly payments more manageable. VA loans also have flexible credit requirements, which can benefit service members who might not have an extensive credit history. Additionally, the VA allows a funding fee, which helps sustain the program but can often be rolled into the loan, reducing the immediate cash needed at closing.

Finally, VA loans provide protections that aren’t always available in other mortgages. For example, if financial hardship arises, the VA can assist borrowers in avoiding foreclosure, offering counseling and negotiation support with lenders.

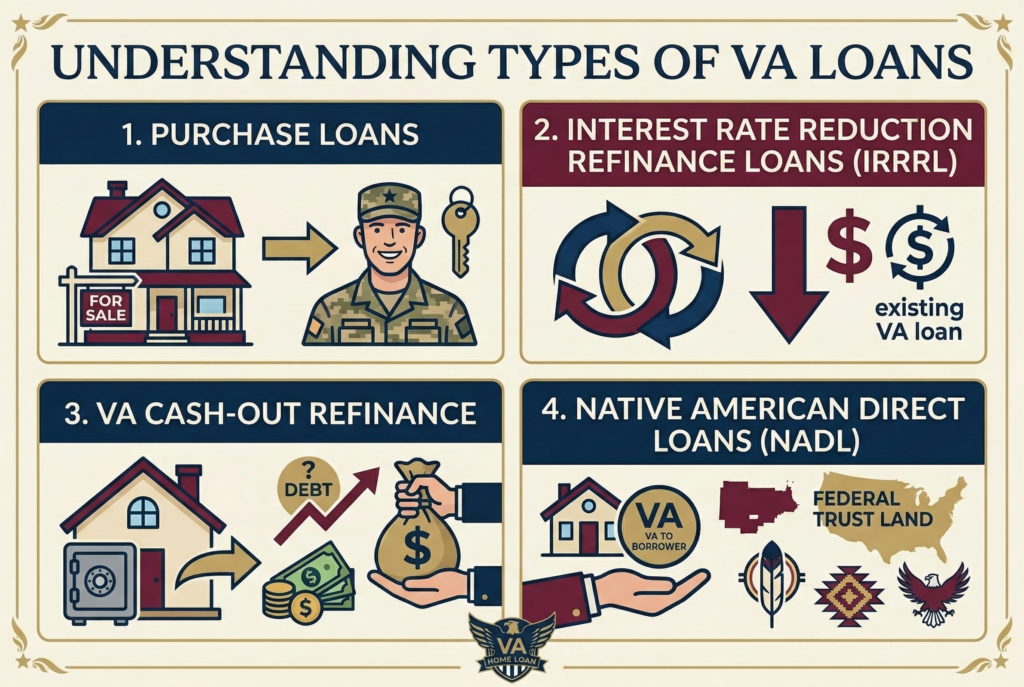

Types of VA Loans

1. Purchase Loans

These allow eligible veterans and service members to buy a home with no down payment, low interest rates, and no private mortgage insurance. This type is ideal for first-time homebuyers or those looking to buy a new property without needing to save thousands upfront.

2. Interest Rate Reduction Refinance Loans (IRRRL)

For those who already have a VA-backed mortgage, the Interest Rate Reduction Refinance Loan (IRRRL), also called a VA Streamline Refinance, can help you lower your interest rate or switch from an adjustable-rate mortgage to a fixed-rate loan. This type of refinance often requires minimal documentation, making it a quick and convenient option for reducing monthly payments.

3. VA Cash-Out Refinance

If you have built equity in your home, a VA cash-out refinance allows you to tap into that equity for major expenses, such as home renovations, debt consolidation, or emergency funds. Unlike conventional cash-out loans, VA rules often permit a higher loan-to-value ratio, which can provide more flexibility in accessing funds.

4. Native American Direct Loans (NADL)

Native American Direct Loans (NADL) serve eligible Native American veterans purchasing a home on trust land, offering similar benefits to standard VA loans. There are also specialized programs for certain military spouses or surviving spouses, which ensure continued access to VA loan benefits even if the service member has passed away

By exploring each type carefully, borrowers can align their loan choice with their financial goals, whether it’s buying a home, lowering interest costs, or leveraging equity safely.

Costs to Consider

While VA loans reduce many upfront costs, they aren’t completely free. The VA funding fee ranges from 1.25% to 3.3% of the loan amount depending on the type of service and whether it’s a first-time use. This fee supports the VA loan program and can often be rolled into the loan rather than paid upfront. Veterans with service-related disabilities are exempt from the funding fee.

Other costs include standard closing costs, which can cover title insurance, appraisal fees, and loan processing. The VA caps certain fees to protect borrowers, but costs can still vary by lender. Shopping around and comparing lenders is essential to ensure you get the best deal.

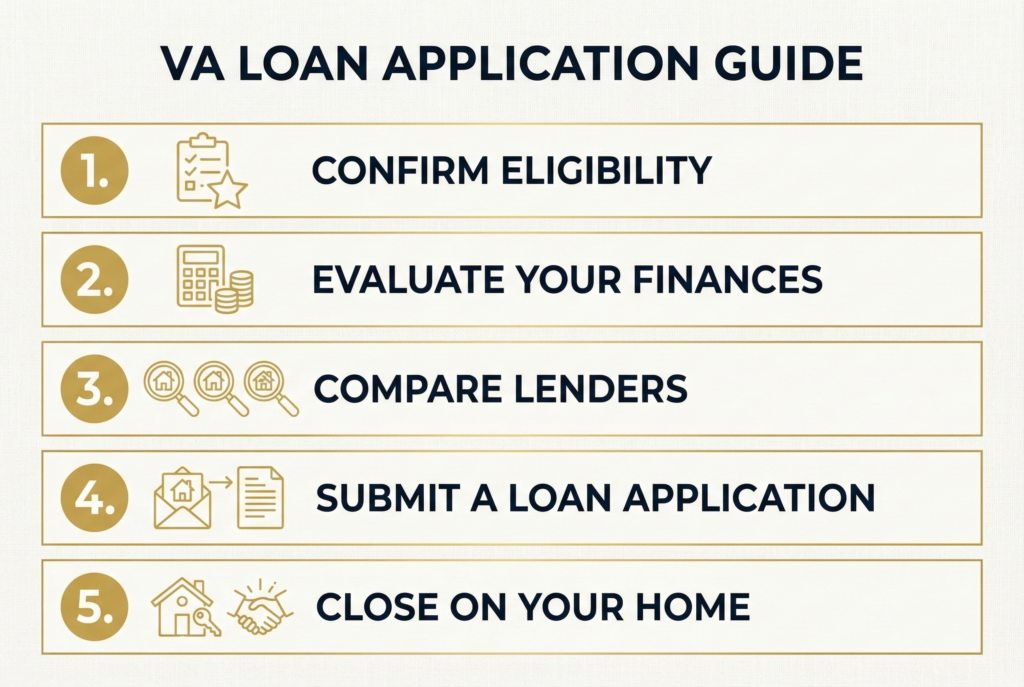

Step-by-Step Guide to Applying for a VA Loan

Step 1: Confirm Eligibility

Obtain your Certificate of Eligibility (COE) to prove your entitlement to a VA-backed loan. This step ensures you meet military service requirements.

Step 2: Evaluate Your Finances

Check your credit score, review your monthly income and expenses, and determine how much home you can afford. Unlike conventional loans, VA loans are forgiving on shorter credit histories but still require reasonable financial stability.

Step 3: Compare Lenders

Different lenders may offer varying interest rates, fees, and customer service. Comparing multiple lenders helps you secure the best rate and avoid unnecessary costs.

Step 4: Submit a Loan Application

Provide income documents, COE, and information about the property you intend to buy. Lenders will assess your financial standing and calculate your VA loan eligibility.

Step 5: Close on Your Home

After approval, review the Closing Disclosure, verify costs, and sign documents. Once complete, you can move into your new home with the peace of mind that comes from VA-backed protections.

Tips to Maximize Your VA Loan Benefits

Even with a VA loan, careful planning can enhance your financial outcomes. Avoid borrowing the maximum allowable loan if it stretches your budget; instead, aim for a comfortable monthly payment. Use the VA cash-out option only for strategic needs like high-interest debt payoff or essential home improvements. Regularly review interest rates and consider IRRRL if a lower rate could save thousands over time.

Finally, stay informed about VA rules and updates, as benefits and fees can change, impacting your borrowing strategy. Working with a lender experienced in VA loans ensures you fully leverage the program.

Conclusion

VA loans offer unmatched benefits for eligible veterans, active-duty service members, and surviving spouses. From no down payment to competitive interest rates and flexible credit requirements, they provide a practical path to homeownership and financial stability. By understanding eligibility, costs, and loan types, and by following a structured application process, borrowers can confidently secure financing while minimizing risk.

Whether you’re buying your first home, refinancing an existing mortgage, or accessing equity, mastering the VA loan process can save you thousands and support long-term wealth building. Start with your COE, evaluate your finances, and partner with a VA-savvy lender to make the most of this valuable benefit.