: How It Works, Key Benefits, and Smart Ways to Use It")

A Tax-Free Savings Account (TFSA) is a popular savings and investing account designed to help people grow money without paying tax on investment gains or qualified withdrawals. While the TFSA is a Canadian account rather than a U.S. retirement plan, it still gets a lot of attention from U.S.-based readers researching tax-advantaged saving options. Understanding how it works can help clarify where it fits, who benefits most, and why it’s often compared with accounts like a Roth IRA or high-yield savings account.

What Is a Tax-Free Savings Account?

A TFSA is a registered account that allows eligible individuals to contribute money, invest it, and withdraw funds later without paying tax on the growth inside the account. That means interest, dividends, and capital gains earned within the TFSA can build over time without creating the same tax burden you’d typically face in a taxable investment account.

Despite the name, a TFSA isn’t limited to cash savings. It can usually hold a range of investments, depending on the financial institution and account setup. That may include cash, mutual funds, exchange-traded funds, stocks, bonds, and other qualified investments.

This is one reason the TFSA can be more flexible than many people first assume. It isn’t just a place to park emergency cash. It can also be used as a long-term investing vehicle, depending on the account holder’s goals and timeline.

For U.S. readers, the biggest point to understand is that the TFSA isn’t a U.S. account type. It belongs to the Canadian financial system. Even so, people often look it up because the concept of tax-free growth is similar to ideas seen in some U.S. accounts.

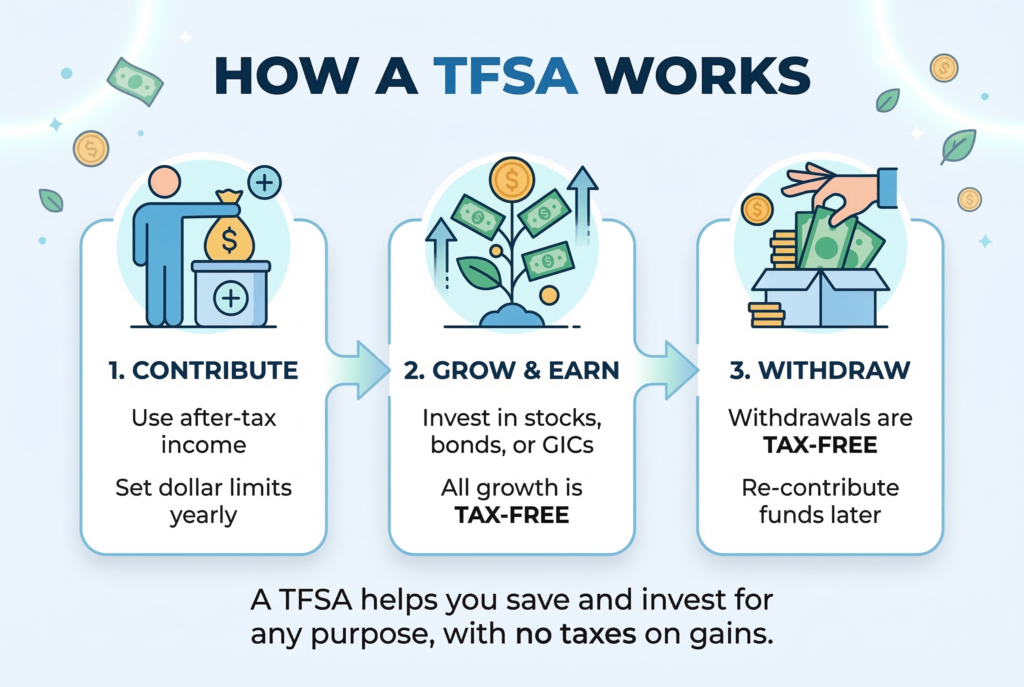

How a TFSA Works

A TFSA works by allowing contributions up to a set annual limit, with unused contribution room generally carrying forward. Once money is contributed, the account holder can keep it in cash or invest it based on the options available in the account.

The main appeal is simple: any growth that happens inside the account is generally tax-free, and withdrawals are also typically tax-free. That treatment makes the TFSA attractive for both shorter-term and longer-term financial goals.

Another important feature is flexibility. Unlike some retirement-focused accounts, a TFSA doesn’t usually require the money to stay locked in until retirement. Funds can often be withdrawn when needed, which makes the account useful for goals such as emergency savings, a future home purchase, travel, education, or general investing.

In many cases, withdrawn amounts can also create new contribution room in a future year, which adds to the account’s usefulness. That feature makes the TFSA appealing for people who want tax-free growth without the same withdrawal restrictions that apply to certain retirement accounts.

Why the TFSA Gets Attention From U.S. Readers

A lot of U.S.-based readers come across the Tax-Free Savings Account and assume it’s a direct equivalent to an American savings or retirement product. It isn’t. Still, the TFSA attracts interest because the tax treatment sounds very appealing and because the name is easy to misunderstand.

For someone in the United States, the closest comparisons often depend on the purpose of the money. A Roth IRA also offers tax-free qualified withdrawals, but it has retirement-focused rules and eligibility requirements. A Health Savings Account, or HSA, can offer major tax advantages too, but only for people with eligible health plans and qualified medical spending. A standard savings account in the U.S. offers liquidity, but interest is usually taxable.

The TFSA stands out because it combines tax-free growth with broad flexibility. That combination is what makes it so widely discussed.

Key Benefits of a TFSA

The TFSA has several strengths that explain why it’s considered such a valuable financial tool.

Tax-Free Investment Growth

The most obvious benefit is tax-free growth. Interest, dividends, and capital gains earned inside the account generally don’t create the same tax drag you’d face in a regular taxable account. Over time, this can make a meaningful difference, especially for long-term investors.

Tax-Free Withdrawals

Another major advantage is that withdrawals are usually tax-free. This gives account holders flexibility to use the money when needed without worrying about triggering additional tax on the gains.

Flexibility for Multiple Goals

A TFSA can often be used for more than one purpose. Some people use it for emergency savings. Others use it for medium-term goals or long-term investing. Because the account isn’t strictly limited to retirement use, it can fit into many kinds of financial planning.

Wide Range of Investment Options

Depending on the provider, a TFSA can hold more than cash. That means savers may be able to invest for stronger long-term growth instead of relying only on low-yield deposit products.

Useful Contribution Room Structure

The ability to build contribution room over time adds value, especially for people who can’t contribute the maximum every year. This feature can make the account easier to use across different life stages and income levels.

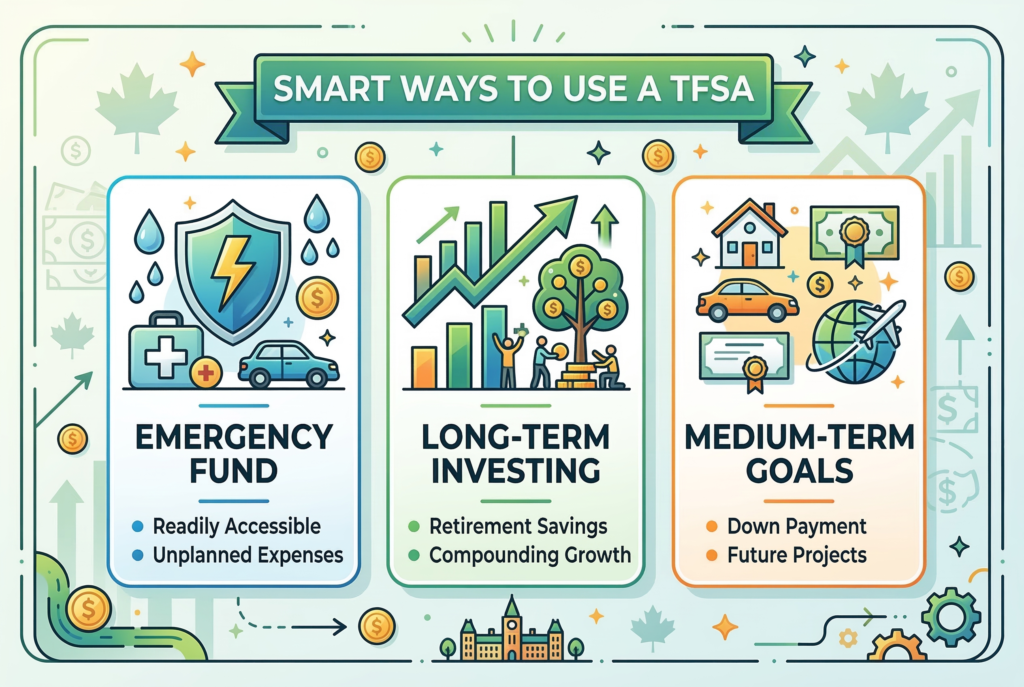

Smart Ways to Use a TFSA

The best way to use a TFSA depends on your financial goals, time horizon, and need for liquidity. Because the account is flexible, there isn’t just one correct strategy.

One smart use is as an emergency fund. If the money stays in a lower-risk option, the TFSA can provide accessible savings while still allowing any interest or earnings to grow tax-free. This may appeal to people who want more efficiency than a taxable savings account can offer.

Another strong use is for long-term investing. Since gains inside the account can grow tax-free, many people prefer to hold growth-oriented investments in the TFSA if they have a long timeline and won’t need the money soon. This can make the account particularly valuable for younger investors or anyone focused on long-term compounding.

A TFSA can also work well for medium-term goals, such as saving for a future home-related expense, education costs, or a major purchase. In that case, the investment mix should usually match the timeline. Money needed soon may belong in safer holdings, while money with a longer timeline may be invested more aggressively. The key is to align the account’s investments with the purpose of the money. A tax-free account still needs a sound strategy behind it.

TFSA vs. Taxable Accounts

Compared with a regular taxable account, the TFSA has a clear advantage in how investment earnings are treated. In a taxable account, interest, dividends, and capital gains may increase your annual tax bill. In a TFSA, those earnings typically grow without that ongoing tax cost.

That difference matters because taxes can reduce net returns over time. When an account allows money to compound without annual tax drag, the long-term outcome may be stronger, especially for investors who use the account consistently.

Still, a taxable account may offer more unrestricted contribution potential and can still be useful once tax-advantaged space is fully used. The better choice depends on account availability, eligibility, and the saver’s broader financial plan.

What U.S. Readers Should Keep in Mind

For readers in the United States, the biggest takeaway is that a TFSA isn’t a domestic account option in the way a Roth IRA, 401(k), or HSA is. That makes context especially important.

If you’re researching saving strategies in the U.S., the TFSA may be useful mainly as a point of comparison. Its structure highlights the value of tax-free growth and flexible withdrawals, but American savers usually need to look at U.S.-based account types when deciding where to save and invest.

That’s why searchers should be careful not to assume a TFSA works the same as a standard savings account or retirement plan available through a U.S. bank or employer. The name sounds simple, but the account belongs to a different tax system.

Common Misunderstandings About TFSAs

One common misunderstanding is that a TFSA is only for cash savings. In reality, it can often be used for a much broader investment strategy. Another misconception is that “tax-free” means there are no rules or limits. In practice, contribution rules still matter, and account holders need to pay attention to how the account is used.

A third misunderstanding, especially among readers in the United States, is the assumption that the TFSA functions like a typical savings account found in many countries. However, this is not the case. It’s a specific account type with a distinct role in Canadian personal finance. Understanding these differences is important because tax-advantaged accounts work best when they’re used intentionally and within the correct system.

When a TFSA Can Be Especially Valuable

A TFSA can be especially useful for people who want both flexibility and tax-free growth. It may be attractive for savers who don’t want every dollar tied up in retirement-only accounts, or for investors who want a tax-efficient space for goals outside traditional retirement planning.

It can also be valuable for people who expect to need access to funds without sacrificing the benefit of tax-free investment growth. That makes it different from accounts that offer tax advantages but impose tighter withdrawal restrictions. In that sense, the TFSA is often appreciated not just for what it saves in taxes, but for how adaptable it can be in real-world financial planning.

Conclusion

A Tax-Free Savings Account (TFSA) is a flexible, tax-advantaged account that allows eligible users to grow savings and investments without paying tax on the earnings or withdrawals. Its main strengths include tax-free growth, tax-free withdrawals, and the ability to support both short-term and long-term goals. Those features make it one of the more versatile savings and investing tools in the system where it applies.

For readers in the United States, the TFSA is best understood as a useful comparison point rather than a standard local account option. It highlights why tax-efficient saving matters and why flexible account design can be so powerful. Whether you’re researching global personal finance concepts or comparing savings strategies, understanding how the TFSA works can give you a clearer view of what makes tax-advantaged accounts so valuable.