Understanding your tax liability is essential for managing your finances effectively and ensuring you pay the correct amount, not too much and not too little. In this article, we’ll explain what tax liability is, how to calculate it, and the strategies you can use to minimize the taxes you owe. Whether you’re an individual or a business owner, the right approach can help reduce your overall tax burden.

What is Tax Liability?

Tax liability is the total amount of tax you owe to the government based on your taxable income, including all applicable taxes such as income tax, capital gains tax, and self-employment tax. It’s calculated based on various factors such as income level, filing status, and eligible deductions and credits.

Your tax liability can vary significantly depending on how much you earn, your filing status (single or married), and any tax-saving strategies you use. For example, you may qualify for tax credits or deductions that can lower the amount you owe.

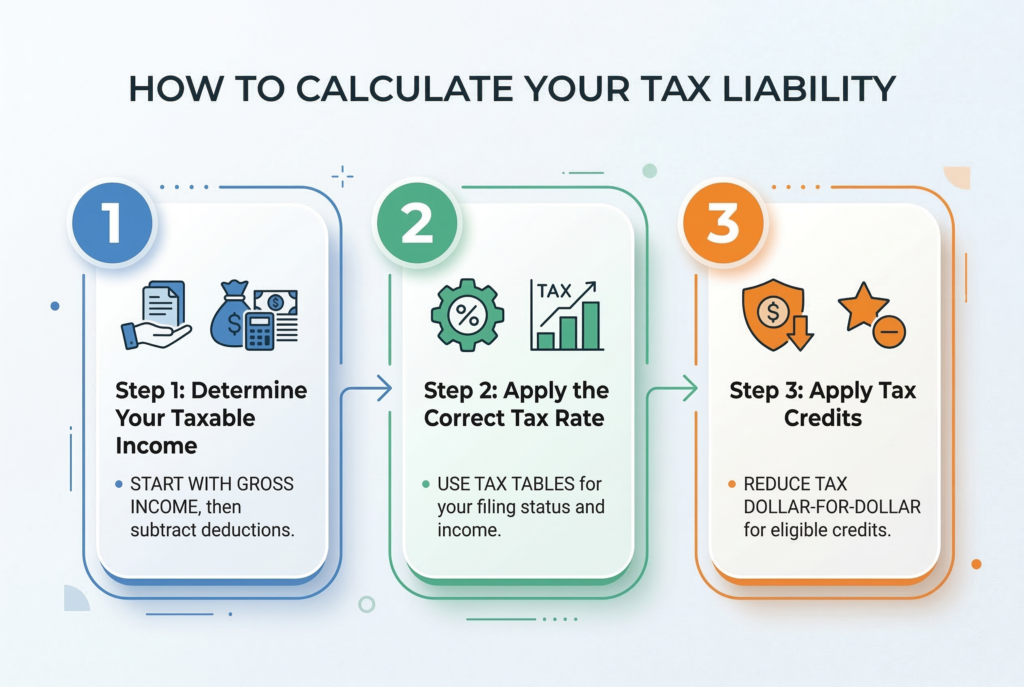

How to Calculate Your Tax Liability

Step 1: Determine Your Taxable Income

Taxable income is the amount of your income that is subject to tax. To calculate it, start with your gross income and subtract eligible deductions. Common deductions include:

- Standard deduction: A set amount that reduces your taxable income.

- Itemized deductions: Deductions for things like mortgage interest, state taxes, or medical expenses.

- Contributions to retirement accounts like IRAs or 401(k)s, which can reduce taxable income.

Example: If your gross income is $60,000 and you take the standard deduction of $12,000, your taxable income would be $48,000.

Step 2: Apply the Correct Tax Rate

Once your taxable income is determined, you apply the appropriate tax rate, which can vary depending on your income level and filing status. The U.S. tax system is progressive, meaning that higher levels of income are taxed at higher rates. For example, if your taxable income falls into the 12% tax bracket, that portion of your income will be taxed at 12%, and income above that will be taxed at a higher rate.

Step 3: Apply Tax Credits

Tax credits directly reduce the amount of tax you owe. Common tax credits include:

- Child Tax Credit: If you have qualifying children, you may reduce your tax liability by up to $2,000 per child.

- Earned Income Tax Credit (EITC): A credit for low to moderate-income working individuals and families.

- Education credits: If you are paying for education, there are credits like the American Opportunity Credit.

Unlike deductions, which reduce taxable income, tax credits reduce the actual amount of tax you owe, making them more valuable.

Types of Taxes Contributing to Your Tax Liability

Income Tax

The most common type of tax liability is income tax, which is based on your wages, salary, or other income sources. It is calculated according to tax brackets, with higher incomes taxed at higher rates.

Capital Gains Tax

If you sell an asset (such as property or stocks) for a profit, that profit is taxed as capital gains. Capital gains are taxed at different rates depending on how long you’ve held the asset. Long-term capital gains (on assets held for more than one year) are generally taxed at a lower rate than short-term capital gains.

Self-Employment Tax

If you are self-employed or own a business, you’re required to pay self-employment tax, which covers Social Security and Medicare contributions. This tax is calculated on your net earnings from self-employment.

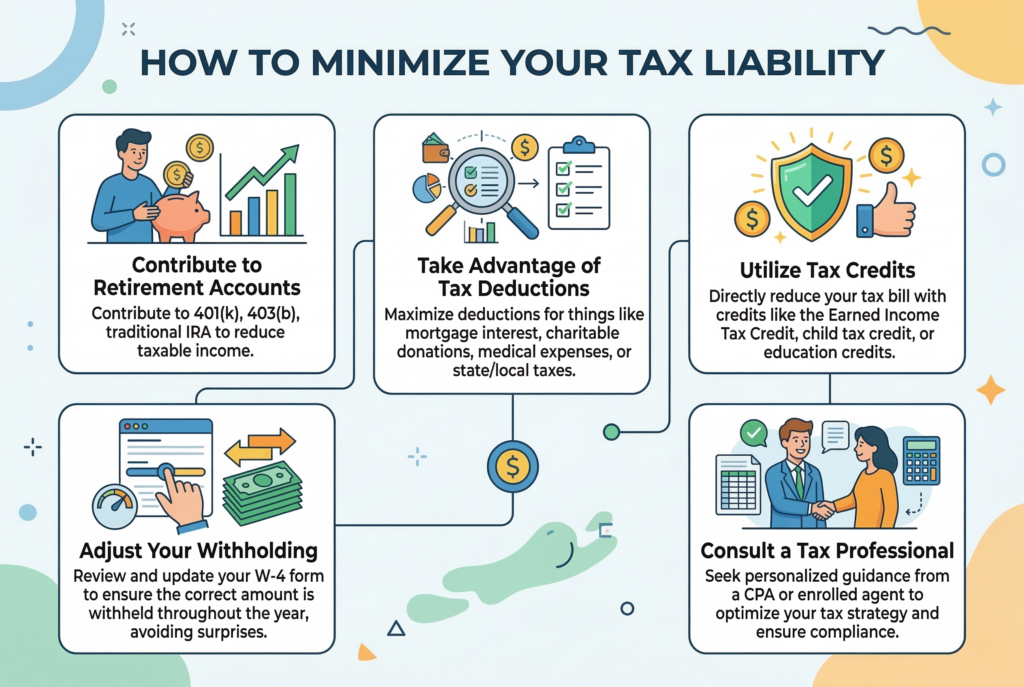

How to Minimize Your Tax Liability

Contribute to Retirement Accounts

Contributions to retirement accounts like IRAs and 401(k)s can reduce your taxable income, thus lowering your tax liability. These contributions are often tax-deferred, meaning you won’t pay taxes on the money until you withdraw it in retirement.

Example: If you contribute $5,000 to your 401(k), your taxable income decreases by that amount, potentially reducing the amount of tax you owe.

Take Advantage of Tax Deductions

Deductions lower your taxable income, which in turn reduces your tax liability. In addition to the standard deduction, you can also deduct things like mortgage interest, state and local taxes, and charitable donations. If your total deductions exceed the standard deduction, it’s worth itemizing your deductions.

Utilize Tax Credits

As mentioned, tax credits directly reduce your tax bill, so make sure to claim all the credits you qualify for. Some credits, like the Child Tax Credit, can reduce your liability by thousands of dollars.

Adjust Your Withholding

If you’re having too much tax withheld from your paycheck, you could be giving the government an interest-free loan. By adjusting your withholding through your W-4 form, you can keep more of your money throughout the year, rather than waiting for a refund.

Consult a Tax Professional

For complex tax situations, such as owning a business or having multiple sources of income, consulting a tax professional can be invaluable. They can help identify deductions, credits, and tax-saving strategies you may have missed.

Example of Calculating Tax Liability

Let’s say you’re a single filer with a taxable income of $50,000 in 2026. Based on current IRS tax brackets, here’s how your tax liability would be calculated:

- The first $11,000 is taxed at 10%.

- The next $33,000 is taxed at 12%.

- The remaining $6,000 is taxed at 22%.

After applying the tax rates, you’ll have your total tax liability, and you can subtract any eligible tax credits to lower your final amount.

Conclusion

Tax liability is an unavoidable part of managing your finances, but with the right strategies, you can reduce the amount you owe. By understanding your taxable income, utilizing deductions and credits, and contributing to retirement accounts, you can lower your tax burden and keep more of your hard-earned money. If your tax situation is complex, it’s always a good idea to consult a tax professional to ensure you’re maximizing your tax-saving opportunities.