Filing taxes can be a stressful process for many, especially for first-time filers or those unsure about where to start. But understanding tax returns and the process behind them can help you feel more confident and even allow you to maximize your refund. In this article, we’ll break down everything you need to know about tax returns, from what they’re, how to file them, and key steps to take to ensure you’re getting the most back.

What Is a Tax Return?

A tax return is a form submitted to the government to report your income, expenses, and other financial details to determine the amount of taxes you owe or the refund you’re entitled to. Essentially, it’s how you settle your annual financial obligations with the government. Tax returns also play a crucial role in applying for loans, rental agreements, or financial aid, as they show your financial standing over the past year.

Key Elements of a Tax Return

- Income: All sources of income, such as wages, salaries, and interest, need to be reported.

- Deductions: These reduce your taxable income and can include expenses like student loan interest, medical costs, and charitable donations.

- Tax credits: These directly reduce the amount of taxes you owe and can be applied for things like education expenses or adopting a child.

- Refund: If you’ve overpaid taxes throughout the year (through deductions from your paycheck, for example), you may receive a refund.

Why Are Tax Returns Important?

First and foremost, tax compliance is the key reason for filing your tax return. It’s your responsibility to ensure that you comply with tax laws, and failing to file or pay taxes on time can result in penalties or even legal action. Filing also opens the possibility for refund opportunities. If too much tax was withheld from your paycheck throughout the year, filing a tax return allows you to get that money back. Additionally, filing helps with tax planning. When you file, it gives you the chance to plan for things like retirement savings or investment opportunities to reduce your tax liability next year.

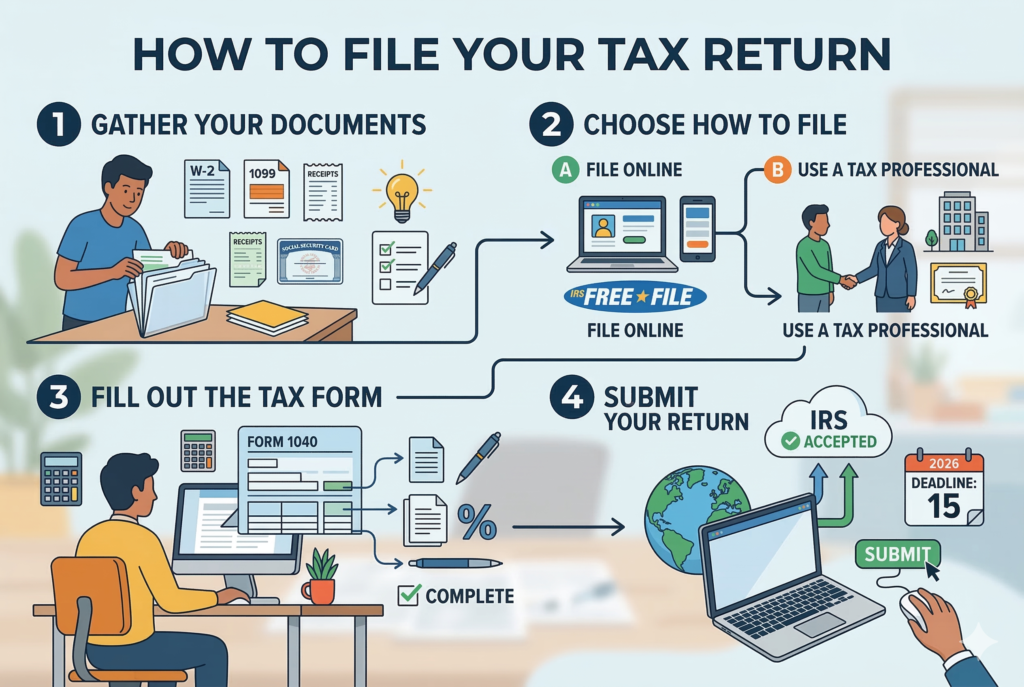

How to File Your Tax Return

Step 1: Gather Your Documents

Before starting the filing process, make sure you have all necessary documents, such as:

- W-2 forms (for salaried employees)

- 1099 forms (for independent contractors or freelancers)

- Bank statements and interest certificates

- Receipts for deductible expenses (for example, medical bills, or educational costs)

- Social Security Number (SSN) or Taxpayer Identification Number (TIN)

Step 2: Choose How to File

You can file online (e-filing), which is the quickest and easiest way to submit your return. Using platforms like the IRS Free File system or paid tax software like TurboTax can walk you through the process step by step. Alternatively, you can file manually by completing the appropriate forms and mailing them to the IRS, although this method is slower and can lead to processing delays. If your taxes are more complicated, such as being self-employed or having multiple income streams, it may be worth seeking help from a tax professional.

Step 3: Fill Out the Tax Form

Depending on your situation, you’ll use different forms. The most common is the 1040, which is for individual income tax returns. If you’re self-employed, you’ll need additional forms (like the Schedule C for reporting business income). Make sure to accurately report your income, deductions, and credits.

Step 4: Submit Your Return

Once you’ve completed your forms, submit them to the IRS. If you’re e-filing, the software will walk you through submission. If you’re mailing it in, make sure to use certified mail or another trackable service to ensure it arrives safely.

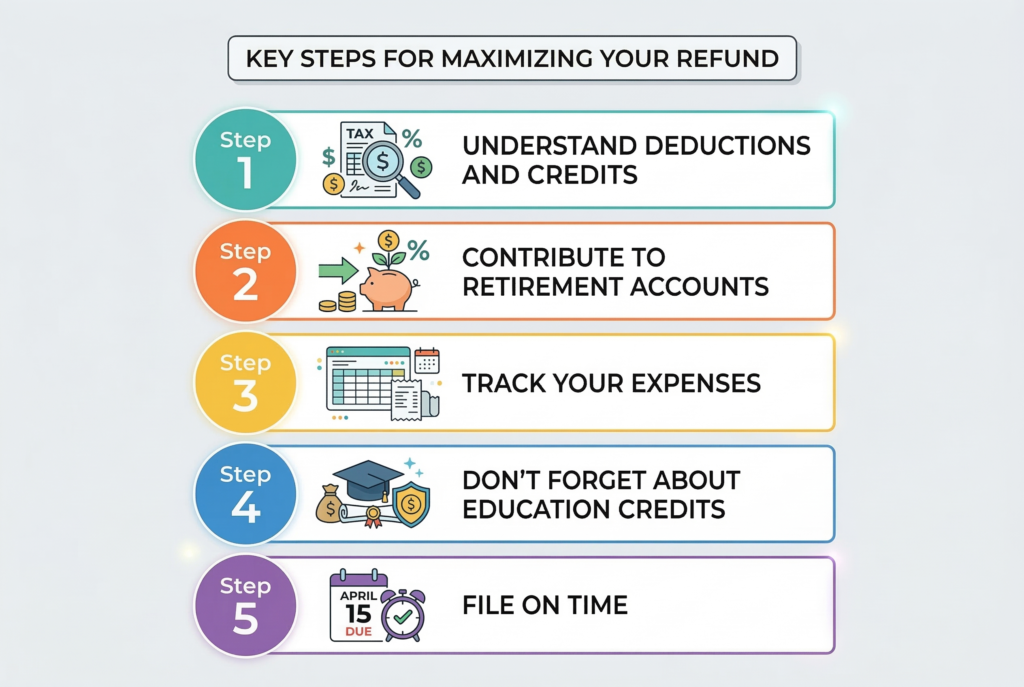

Key Steps for Maximizing Your Refund

Step 1. Understand Deductions and Credits

Deductions reduce your taxable income, while credits reduce your tax bill directly. Common deductions include the standard deduction or itemized deductions, such as mortgage interest, medical costs, or charitable donations. Tax credits include the Earned Income Tax Credit (EITC) and the Child Tax Credit for eligible parents. Contributing to retirement accounts like a 401(k) or an IRA can also lower your taxable income and potentially increase your refund.

Step 2. Contribute to Retirement Accounts

Contributing to retirement accounts like a 401(k) or IRA can lower your taxable income and potentially increase your refund. These contributions are deducted from your income before taxes are calculated, reducing the amount of tax you owe.

Step 3. Track Your Expenses

For self-employed individuals, freelancers, or small business owners, make sure to track all business-related expenses. Business deductions can include office supplies, mileage, and even the cost of a home office, helping to reduce your taxable income.

Step 4. Don’t Forget About Education Credits

If you or your dependents are in school, you might be eligible for tax credits such as the American Opportunity Credit or the Lifetime Learning Credit, which can reduce your tax liability significantly.

Step 5. File on Time

The sooner you file, the sooner you’ll receive your refund. Missing the deadline can lead to penalties and delays, so make sure to file by the due date, which is typically April 15th.

Avoid Common Mistakes

Many taxpayers make mistakes that can result in smaller refunds or penalties. To avoid these issues, it’s important to double-check your Social Security Number (SSN). A simple typo can cause delays and prevent your return from being processed on time. Additionally, if you’re expecting a direct deposit refund, make sure to verify your bank account details. Incorrect information can lead to delays or even your refund being sent to the wrong account. Lastly, it’s crucial to ensure all required documents are included when you file. Missing forms or documents can result in your return being delayed or rejected, so take extra care to gather everything needed before submitting your tax return.

Conclusion: Stay Ahead with Tax Filing

Filing a tax return doesn’t have to be a daunting task. With a little planning, the right resources, and attention to detail, you can navigate the process with confidence and ensure you’re getting the maximum refund. Stay organized, utilize available deductions and credits, and file on time to keep your finances in check and avoid penalties. Whether you’re a first-time filer or a seasoned pro, taking the time to understand the process will not only ensure compliance but also open the door to potential savings.

Related Articles

- Income Tax Calculation Explained: Simple Steps to Estimate What You Owe in the U.S.

- Unexpected Tax Bills: Why They Happen and How to Prevent Them

- Tax Brackets Explained: How the Income Tax System Really Works

- States With No Income Tax: Where You’ll Pay Less and How These States Offset Revenue

- 10 Common Tax Mistakes That Cost People Thousands Without Them Noticing

- How to Build a Tax Smart Financial Lifestyle for Long Term Financial Security