Student loans are often an unavoidable aspect of financing higher education, and understanding how they work is essential for managing the long-term impact on your financial health. With rising tuition fees and living costs, it’s crucial to know how to navigate student loans, from borrowing to repayment, and even the potential for forgiveness. This guide delves into the complexities of student loans, offering detailed information to help you make informed decisions.

What Are Student Loans?

A student loan is borrowed money that you use to pay for your higher education expenses, such as tuition, fees, books, and living costs. These loans are offered by both the federal government and private institutions like banks and credit unions. They’re generally repaid after graduation, although some loans, particularly private ones, may require you to make payments while you’re still in school. The government offers lower interest rates and more flexible repayment options, making federal loans a popular choice for students.

Types of Student Loans

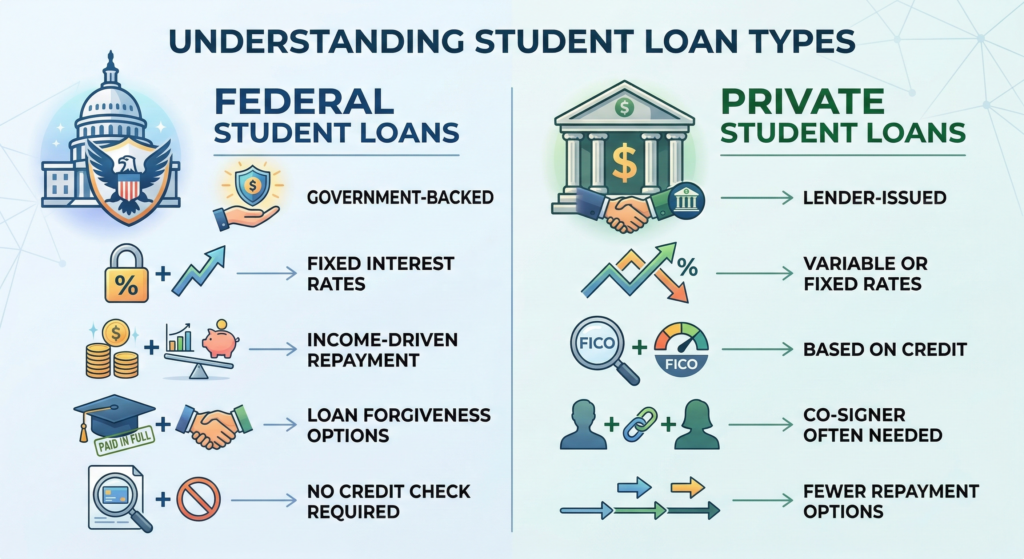

Federal Loans

Federal loans, as discussed earlier, offer lower interest rates and more flexible repayment options. They’re also eligible for certain programs like loan forgiveness and income-driven repayment plans. Federal loans are classified into different categories, including subsidized and unsubsidized loans, as well as PLUS loans for parents and graduate students.

Private Loans

Issued by banks, credit unions, or online lenders, private loans tend to have higher interest rates than federal loans and depend on your credit score. A co-signer may be required for students with little or no credit history. Unlike federal loans, private loans do not come with government protections like income-driven repayment options or forgiveness programs.

How Do Student Loans Work?

Student loans work by providing you with funds to cover educational expenses, which you must pay back with interest. The repayment process typically begins after you graduate or drop below half-time enrollment, but here’s what you need to know about the process:

Disbursement

Once you’re approved for a loan, the lender sends the money directly to your school. This payment is used to cover tuition, fees, and other educational costs. Any remaining funds are typically given to you to cover living expenses, such as rent and food.

Interest Rates

Interest is the cost of borrowing money. Federal student loan interest rates are fixed by the government, and they tend to be lower than private loan rates. Rates for federal loans vary depending on the type of loan (subsidized vs. unsubsidized) and the disbursement year. Private loans can have either fixed or variable interest rates, which may depend on your credit score and the lender’s policies.

Example: If you borrow $10,000 at a 5% interest rate for 10 years, you’ll repay more than $15,000 by the time you finish the loan, as the interest adds up over time. Understanding how interest accrues is crucial to estimating the total cost of your loan.

Student Loan Repayment: What You Need to Know

Repayment of student loans generally begins six months after graduation or when you drop below half-time enrollment, though some private loans may require payments while you’re still in school. There are different repayment options available for federal loans, each with its advantages and disadvantages.

The Standard Repayment Plan requires fixed monthly payments over 10 years, which is the fastest way to pay off your loan but may come with higher monthly payments. On the other hand, the Graduated Repayment Plan starts with lower payments that increase over time, which can be beneficial for those expecting their income to grow.

For those struggling with high monthly payments, Income-Driven Repayment Plans (IDR) offer more flexibility. These plans base monthly payments on your income and family size, making them more affordable for individuals with fluctuating or lower earnings. There are several types of IDR plans, including Income-Based Repayment (IBR) and Pay As You Earn (PAYE), each with its own criteria for eligibility and terms.

Another option is Extended Repayment, which allows you to stretch out your loan payments over a longer period (up to 25 years), lowering your monthly payments but increasing the total amount of interest you will pay over time. Additionally, there are options like Deferment and Forbearance, which temporarily suspend payments if you’re facing financial hardship, but these options may lead to accruing more interest, especially on unsubsidized loans.

Student Loan Forgiveness Programs

One of the most attractive aspects of federal student loans is the potential for loan forgiveness. This means that after a certain number of qualifying payments, any remaining loan balance could be forgiven. The most popular forgiveness programs are:

- Public Service Loan Forgiveness (PSLF): If you work in a government or nonprofit organization, you could qualify for forgiveness after making 120 qualifying monthly payments under an income-driven repayment plan. This is ideal for individuals working in public service roles such as teachers, social workers, or government employees.

- Teacher Loan Forgiveness: Teachers who work in low-income schools for five years may qualify for up to $17,500 in forgiveness.

- Income-Driven Repayment (IDR) Forgiveness: After 20-25 years of qualifying payments under an income-driven plan, the remaining balance of the loan can be forgiven.

It’s important to note that only federal student loans are eligible for forgiveness, and private loans don’t qualify for these programs.

What Happens If You Default on Your Student Loans?

Defaulting on your student loans can have serious consequences, including wage garnishment, tax refund seizure, and a significant drop in your credit score. Default occurs after you miss several months of payments, and it makes it much harder to qualify for future credit. To avoid default, it’s essential to stay in contact with your loan servicer and explore options like deferment, forbearance, or changing your repayment plan if necessary.

Dealing with Financial Hardship

Managing student debt can be stressful, especially for recent graduates facing uncertain job markets or high living costs. If you’re struggling to make payments, don’t hesitate to reach out to your loan servicer. Many servicers offer resources and guidance to help you get back on track, and seeking assistance early can prevent the long-term consequences of default.

Current Trends in Student Loans

In recent years, student loan forgiveness programs have gained significant attention, especially in the context of public service workers and changes to the federal student loan landscape. The Biden administration has pushed for more manageable repayment options and has aimed to offer broader forgiveness programs, such as the SAVE plan, which makes repayment more affordable for low-income borrowers. Additionally, income-driven repayment plans are becoming increasingly popular as they offer more flexibility for students and graduates with variable earnings.

The growing availability of refinancing also plays a role in managing student debt. For borrowers with good credit scores, refinancing can reduce interest rates and lower monthly payments. However, it’s essential to understand that refinancing federal loans with private lenders may cause you to lose access to federal protections, such as income-driven repayment plans and loan forgiveness.

Conclusion

Student loans are a critical tool for funding education, but managing them requires careful planning and understanding of repayment options. By familiarizing yourself with the different types of loans, repayment strategies, and potential forgiveness programs, you can make better decisions that support your long-term financial well-being. If you’re feeling overwhelmed, know that there are resources available to help you manage your debt effectively and navigate the repayment process.