When considering a loan, whether for buying a home, a car, or funding a business venture, understanding loan terms is crucial. Your loan term, which refers to the length of time over which you’ll repay the loan, has a significant impact on your monthly payments, the total interest paid over the life of the loan, and your overall financial flexibility. In this article, we’ll break down what loan terms are, explore different types of loan terms, and provide helpful tips on how to choose the best term for your needs.

What Is a Loan Term?

A loan term is the period during which you agree to repay a loan, including both principal and interest. Loan terms vary depending on the type of loan, lender, and your financial situation. The loan term is typically expressed in years or months and affects both your monthly payment and the total cost of the loan.

For example, when you take out a mortgage, you might choose a 30-year loan term, which means you have 30 years to pay off the loan. On the other hand, a 15-year mortgage gives you a shorter repayment period, meaning higher monthly payments but less interest paid overall.

Choosing the right loan term is essential for aligning your loan with your financial goals and capabilities. Whether you’re focused on lower monthly payments or paying off the loan faster, understanding the impact of different loan terms will help you make an informed decision.

Types of Loan Terms

Short-Term Loans

Short-term loans are loans that typically have terms ranging from 1 to 5 years. These loans are designed to be repaid quickly, and they generally come with higher monthly payments compared to long-term loans. While the monthly payments may be higher, short-term loans have the advantage of paying off quicker, which means you’ll pay less interest overall.

Short-term loans are ideal for individuals who can afford higher monthly payments and want to avoid being tied down by long-term debt. Common examples of short-term loans include personal loans, auto loans, and business loans used for specific purchases or to cover immediate expenses.

Medium-Term Loans

Medium-term loans typically range from 5 to 10 years. These loans offer a balance between manageable monthly payments and the desire to pay off the loan sooner than a traditional long-term loan. With a medium-term loan, you’re still able to enjoy lower monthly payments than a short-term loan while reducing the overall interest cost compared to a long-term loan.

Medium-term loans are often used for major purchases like home renovations, business expansion, or debt consolidation. They offer a good option for individuals or businesses who want to balance monthly affordability with a faster repayment schedule.

Long-Term Loans

Long-term loans typically have terms of 15 to 30 years. These loans are commonly used for major financial commitments, such as buying a home or financing a long-term project. The primary advantage of long-term loans is their ability to offer the lowest monthly payments, making them more affordable on a month-to-month basis.

However, the downside of long-term loans is the higher total interest paid over the life of the loan. Because the loan term is extended, the lender collects more interest, even if the interest rate is relatively low. Long-term loans are ideal for individuals who need the lowest monthly payment possible but are willing to pay more in interest over time. Mortgages are the most common type of long-term loan.

Key Factors That Affect Your Loan Term

When selecting the right loan term for your situation, there are several factors to consider. These factors will influence both the loan type you choose and the terms associated with it.

Interest Rates

Interest rates are one of the most important factors that will impact your loan term decision. In general, shorter loan terms come with lower interest rates, which means you’ll pay less interest over the life of the loan. Longer loan terms, on the other hand, may have slightly higher interest rates.

For example, if you’re choosing between a 15-year mortgage and a 30-year mortgage, the 15-year option will typically offer a lower interest rate, which can save you a significant amount of money in the long run, even though your monthly payments will be higher.

Monthly Payments

The loan term you choose will directly affect your monthly payments. Shorter loan terms have higher monthly payments but allow you to pay off the loan faster, whereas longer loan terms have lower monthly payments, but the loan takes longer to pay off and results in more interest being paid over time.

When deciding on your loan term, it’s crucial to consider your monthly budget. Can you comfortably afford higher monthly payments for a shorter term, or would you prefer the flexibility of lower payments over a longer period?

Loan Purpose

Your loan purpose also plays a significant role in determining the right loan term. For example, if you’re purchasing a home, a 30-year mortgage is common because it provides lower monthly payments, allowing homeowners to afford a larger home. However, if you’re taking out a loan for a small business or personal project, you may opt for a shorter-term loan that aligns with the immediate nature of the purchase or investment.

Future Financial Goals

Your long-term financial goals are essential when considering your loan term. If you plan to refinance in the future or want to own your home outright sooner, a shorter-term loan may be more suitable. Conversely, if you’re planning to make larger investments or need time to build more savings, a longer loan term with manageable payments may make more sense.

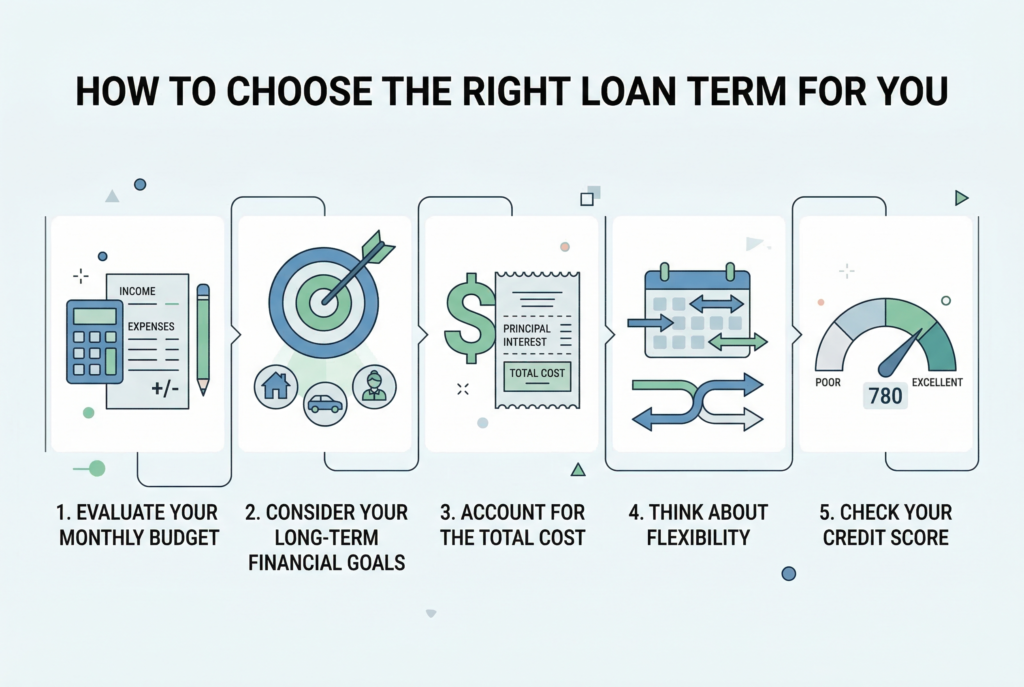

How to Choose the Right Loan Term for You

Evaluate Your Monthly Budget

Review your monthly income and expenses to determine how much you can comfortably allocate to your loan payment. If you can afford higher monthly payments, a shorter loan term might work for you.

Consider Your Long-Term Financial Goals

Think about your future financial plans. Do you want to pay off debt quickly, or are you looking for a long-term solution with lower payments?

Account for the Total Cost

Don’t just look at monthly payments. Consider the total amount you’ll pay over the life of the loan, including interest. Shorter loan terms might have higher payments but will cost you less in interest in the long run.

Think About Flexibility

If you need flexibility in your payments, a longer loan term may be a better option. However, if you’re looking to pay off your debt sooner and build equity faster, a shorter loan term might be worth the higher payments.

Check Your Credit Score

Your credit score will affect the interest rates you qualify for. A higher credit score can help you secure better loan terms with lower interest rates.

Conclusion: Choose the Loan Term That Works for You

Understanding loan terms is crucial when making a large financial commitment, whether you’re buying a home, investing in your business, or financing another significant purchase. By considering factors like interest rates, monthly payments, your loan purpose, and long-term goals, you can make an informed decision about the best loan term for your situation.

Take the time to assess your finances, compare loan options, and consult with a financial advisor if needed. With the right loan term, you’ll be on the path to managing your debt wisely, saving money, and achieving your financial goals.

Related Articles

Explore Different Types of Loans and Learn Which Option Best Fits Your Financial Needs