Buying a home is one of the biggest financial decisions you’ll ever make. For many, a 30-year fixed mortgage is the most popular choice. It offers long-term stability and affordable monthly payments, making it a preferred option for many homebuyers. But while this type of mortgage offers many benefits, it also has its drawbacks. To help you decide if it’s the right fit for you, this article will dive into the pros and cons, costs, and who this mortgage works best for.

What is a 30-Year Fixed Mortgage?

A 30-year fixed mortgage is a type of home loan where the interest rate remains the same throughout the entire 30-year term. This provides homeowners with consistent, predictable payments each month. The loan is paid off over 30 years, and the monthly payments are spread out over this period, which can make your payments more affordable compared to shorter-term loans like a 15-year mortgage.

For example, on a $300,000 mortgage loan at 4% interest, your monthly payments will be lower than a 15-year loan, but you’ll pay more in interest over the long term. The stability of a 30-year mortgage makes it ideal for those seeking long-term affordability, but it’s important to understand both the benefits and the challenges.

Pros of a 30-Year Fixed Mortgage

Lower Monthly Payments

One of the main advantages of a 30-year fixed mortgage is the lower monthly payments. Because the loan is stretched out over a longer period, you’ll pay less each month compared to a shorter-term loan. This can make homeownership more affordable and free up funds for other important expenses, such as savings or daily living costs.

For example, on a $300,000 loan, you’ll typically pay significantly less each month with a 30-year mortgage than you would with a 15-year mortgage. This can be a game-changer for those living on a tight budget or those who want to invest in other financial opportunities while maintaining affordable monthly payments.

Long-Term Stability

A fixed-rate mortgage provides long-term stability. Once your mortgage is set, you don’t need to worry about fluctuating interest rates causing your payments to increase. This makes it easier to plan and manage your finances, especially for those who are risk-averse or want a predictable financial future.

Stability is especially valuable in today’s economic climate, where interest rates can rise unexpectedly. With a fixed-rate mortgage, you’re protected from such fluctuations, giving you peace of mind knowing exactly how much you need to pay each month.

Predictable Budgeting

The predictability of monthly payments is a huge advantage of the 30-year fixed mortgage. Since your payments won’t change, it makes budgeting much easier. You can confidently plan your finances for the long term without worrying about unexpected increases in your mortgage payment.

Cons of a 30-Year Fixed Mortgage

Higher Overall Interest Payments

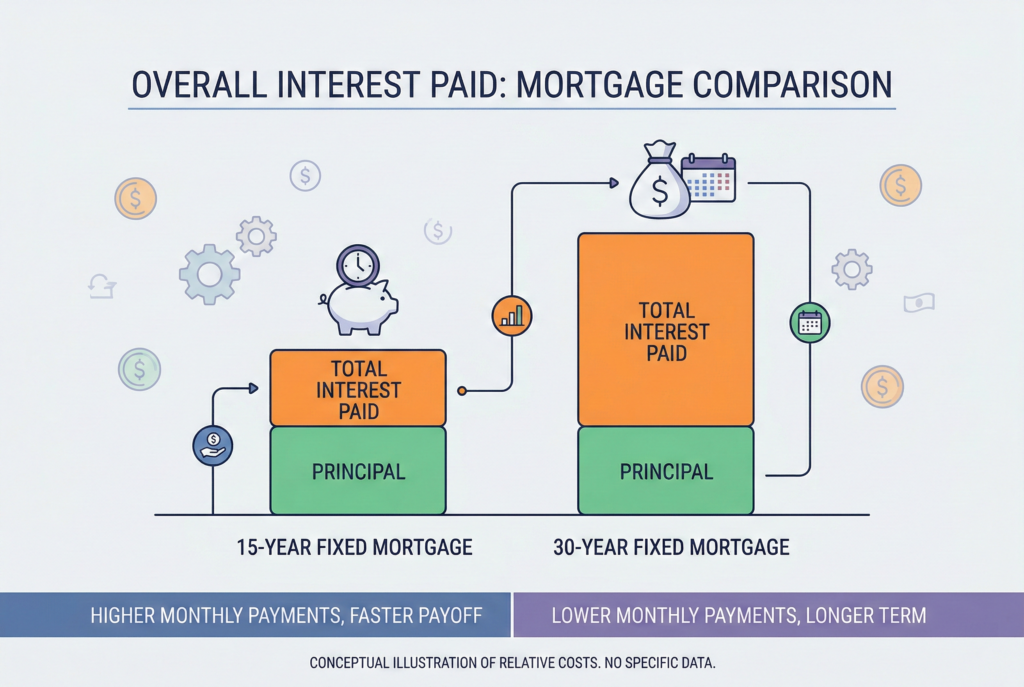

Although your monthly payments are lower, the total interest you pay over the life of the loan is higher. This is because you’re paying off the loan over a longer period of time. As a result, you’ll end up paying more in interest compared to shorter-term loans.

For example, with a $300,000 loan at 4% interest, over 30 years, you may pay more than double the amount in interest than if you had taken a 15-year loan. This means you’ll pay more for the home in the long run.

Slower Equity Growth

In the early years of a 30-year fixed mortgage, most of your payments go toward paying interest rather than the loan’s principal. This means that you’re building equity in your home at a slower pace compared to a shorter-term loan. For those who want to build equity quickly, this could be a disadvantage. If you plan to sell your home within the first few years, you may find that you don’t have much equity built up to cover the selling costs.

Longer Commitment

A 30-year mortgage is a long-term financial commitment. While it’s great for those seeking affordability in the short term, it can feel like a heavy burden if your financial situation changes over the years. Life events, such as job changes or family relocations, may alter your ability to keep up with such a long-term commitment.

How the 30-Year Fixed Mortgage Works

A 30-year fixed mortgage works by offering you a set interest rate for the entire 30-year period. You’ll make monthly payments that cover both the principal (the amount you borrowed) and the interest (the cost of borrowing money).

In the early years of the mortgage, most of your payments will go toward the interest. Over time, as the principal decreases, a larger portion of your monthly payment will go toward reducing the principal. This gradual shift helps you pay off the loan over time, but it also means you’ll pay more in interest during the first part of the loan.

Interest and Principal Breakdown

For example, in the first few years of a 30-year mortgage, you may only pay down a small portion of the principal, while the majority of your payment is applied to the interest. Over time, as your loan balance decreases, more of your payment will go toward paying off the principal, helping you build equity in the home.

When a 30-Year Fixed Mortgage Might Not Be Right for You

A 30-year fixed mortgage isn’t always the best choice for everyone. If you’re considering a mortgage, it’s important to evaluate whether this option fits your personal financial goals. Here are some situations where you might want to consider other mortgage options:

1. You Want to Pay Off Your Loan Faster

If your goal is to pay off your loan quickly and save on interest, you might prefer a 15-year mortgage. This will give you the ability to pay off your home sooner and with significantly less interest over the term of the loan.

2. You Plan to Move Soon

If you don’t plan to stay in your home for the full 30 years, the 30-year mortgage might not be the best choice. Since most of your early payments go toward interest, you may not have much equity to cover the cost of selling your home.

3. You Have a Higher Income and Can Afford Larger Payments

If you have a higher income and can afford to make larger monthly payments, you might benefit from a shorter-term loan, such as a 15-year mortgage. This option offers lower interest payments and helps you build equity faster.

Alternatives to the 30-Year Fixed Mortgage

1. 15-Year Fixed Mortgage

A 15-year mortgage offers higher monthly payments, but it allows you to pay off your home faster and save on interest. This is a good option for those who want to pay off their mortgage more quickly and build equity faster.

2. Adjustable-Rate Mortgages (ARMs)

An ARM offers a lower interest rate at the beginning of the loan, but the rate can change over time. This option may be a good choice for those who plan to move or refinance within a few years, as it offers lower rates initially.

3. Government-Backed Loans

FHA, VA, and USDA loans are government-backed options that offer lower down payments and more flexible qualifications. These are ideal for first-time homebuyers or those with less-than-perfect credit.

Conclusion

A 30-year fixed mortgage is an excellent option for many homebuyers because it offers lower monthly payments and long-term financial stability. However, it’s important to weigh the pros and cons, including the higher overall interest costs and slower equity growth.

By understanding how the 30-year mortgage works and considering your long-term financial goals, you can make an informed decision about whether this is the right option for you. Make sure to shop around, compare interest rates, and understand your financial priorities to find the mortgage that best suits your needs.