To understand how leasing a car works, forget ownership for a moment. A lease allows you to drive a vehicle for a fixed number of years while paying primarily for its depreciation, not its full purchase price. Lease payments are based largely on the car’s expected depreciation during the lease term, which is why they are often lower than loan payments.

Leasing means you’re paying to use the car for a set period, not to own it. You typically drive it for 24 to 36 months, then return it, buy it, or lease another one. While the lower monthly payment can be appealing, it’s important to understand the full agreement, including mileage limits, fees, insurance requirements, and potential charges at the end of the lease.

How Does Leasing a Car Work?

A car lease follows a fairly simple process. First, you choose a vehicle and negotiate its price, just as you would if you were buying. The leasing company then estimates what the car will be worth at the end of the lease, called its residual value.

Next, you sign a lease agreement that sets the lease term, annual mileage limit, monthly payment, and any fees. Most leases last 24 to 36 months.

During the lease, you make monthly payments and keep the vehicle in good condition while staying within the agreed mileage limit. Because the leasing company owns the car, you’ll usually need to meet its insurance requirements and follow the maintenance schedule.

When the lease ends, you typically have three choices:

- Return the vehicle and walk away (after any end-of-lease inspection and fees).

- Buy the car for the price listed in your lease agreement.

- Lease or finance another vehicle.

How Much Does It Cost to Lease a Car?

The real answer to how much does it cost to lease a car has two parts: what you pay upfront and what you pay every month.

Most drivers pay drive off costs when they sign. These may include the first month’s payment, registration fees, taxes, dealer fees, and an acquisition fee. The acquisition fee is the charge from the leasing company to set up the contract, and it often runs around $500 to $1,000. Some leases also ask for a down payment, though putting a large down payment on a lease can be risky. If the car is totaled early, you may not recover that cash the way you expect.

Then comes the monthly payment. A lease payment is shaped by three main numbers: capitalized cost, residual value, and money factor.

- Capitalized cost is the negotiated price of the car. Treat it like the selling price. Don’t assume it’s fixed just because you’re leasing. If the dealer inflates the capitalized cost, your monthly payment rises.

- Residual value is the estimated value of the car at the end of the lease. If a $40,000 car is expected to be worth $25,000 after three years, the expected depreciation is $15,000. That depreciation becomes the core of what you pay.

- Money factor is the lease version of interest. Dealers may quote it as a small decimal, which makes it feel harmless. To estimate the APR, multiply the money factor by 2,400. A money factor of 0.0025 is roughly 6% APR.

Why Lease Payments Look So Low

Lease ads often focus on the monthly payment because that is the emotional hook. A shopper may see $399 per month and feel like they found a bargain. But that number may assume a large down payment, strict mileage limits, excellent credit, and extra fees due at signing. This is where many shoppers get trapped. They compare a lease payment with a loan payment without comparing the total cost. A loan payment may be higher, but after the loan is paid off, the car is yours. A lease payment may be lower, but after years of payments, you usually return the car with no equity. That doesn’t make leasing wrong. It just means the monthly payment isn’t the whole story.

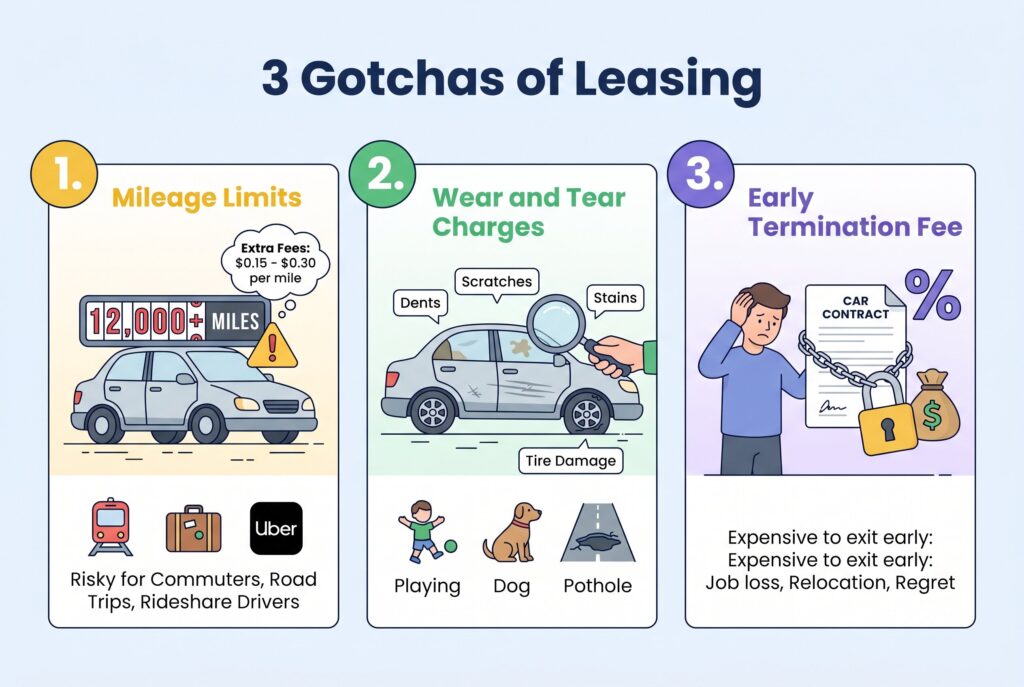

The 3 Gotchas of Leasing

1. Mileage Limits

Most leases come with mileage limits, often 10,000 to 12,000 miles per year. Some allow 15,000 miles, but the payment may be higher. If you go over the limit, you may pay around $0.15 to $0.30 per mile. Driving 5,000 miles over your limit could cost $750 to $1,500 at lease end. This is why leasing can be dangerous for commuters, road trip families, rideshare drivers, and anyone whose job location may change. If your life isn’t predictable, the mileage limit can become expensive fast.

2. Wear and Tear Charges

When you return the car, the leasing company inspects it. Small dents, wheel scratches, stained seats, cracked glass, tire damage, and interior wear may lead to extra charges. The phrase “normal wear” sounds generous, but the final judgment belongs to the leasing company. If you have children, pets, tight parking, rough roads, or winter weather, be realistic. A lease expects the vehicle to come back clean, marketable, and within contract standards.

3. Early Termination Fee

An early termination fee can be brutal. If you need to exit the lease early because of job loss, relocation, family changes, or regret, you may owe remaining payments and additional charges. A lease is flexible only when you stay inside the rules. Outside the rules, it can become rigid and expensive.

Is Leasing a Car a Good Idea?

Is leasing a car a good idea? Yes, for the right driver. Leasing can make sense if you drive low miles, want a new car every few years, prefer warranty coverage, and don’t care about ownership. It can also work well for someone who wants predictable transportation without worrying about long term repairs.

Leasing may also be useful for some EV shoppers. Electric vehicle technology changes quickly, and battery concerns can make long term ownership feel uncertain. A short lease lets you drive newer technology without committing to the car for eight or ten years. But leasing is a poor fit if you drive a lot, want to customize the car, dislike strict contracts, or care about building equity. It’s also risky if you focus only on the monthly payment and ignore the full lease terms.

Lease Negotiation: What to Ask the Dealer

Never walk into a dealership and ask, “What can I get for $400 a month?” That gives the dealer too much control. They can stretch terms, adjust fees, or hide costs to hit your payment target. Instead, ask for the full quote in writing. Request the capitalized cost, residual value, money factor, acquisition fee, drive off cost, mileage allowance, disposition fee, and purchase option price. Compare several dealers using the same vehicle, same mileage allowance, and same term. Negotiate the car price first, just as if you were buying. A lower capitalized cost can reduce your monthly lease payment without tricks.

Conclusion

What does it mean to lease a car? It means you’re paying for temporary use, not ownership. That can be smart if your driving life fits the contract, but expensive if it doesn’t.

The best lease shoppers don’t chase the lowest advertised payment. They decode the numbers, compare quotes, understand mileage limits, and read every fee before signing. If you want freedom, ownership, and long term value, financing or buying used may be stronger. If you want a new car, low predictable miles, and warranty coverage, leasing can work, but only when you control the deal instead of letting the payment control you.